At the end of September, the Board of Governors of the Federal Reserve System pegged unfunded pension liabilities of US state and local governments at more than $4 trillion, a significant increase on the previous figure of $2 trillion.

The new number is the reflection of an accounting change in the way that the Fed considers expectations of future salary growth.

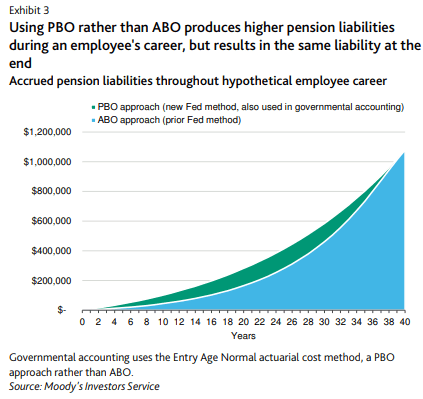

Under the previous model, the Fed relied on an “accrued benefit obligation,” or “ABO,” approach to measuring liabilities. This method used salary growth once it had already occurred, rather than projected salary growth. As pension benefit formulas are typically based on higher average salaries, which tend to occur towards the end of an employees career, ABO accounting can give somewhat of a misleading estimate of future pension obligations.

Instead, the Fed has now adopted a “projected benefit obligation,” or “PBO,” approach. This method of accounting recognizes assumed future salary growth, which gives a more accurate reflection of the ultimate pension liability that will arise for each employee.

Accounting change

The most significant difference between ABO and PBO accounting is that the former tends to understate the ultimate pension obligations for each employee throughout their career while PBO accounting gives a smoother, more realistic and less volatile prediction, as the chart from credit rating agency Moody’s below shows.