T. Rowe Price multi-asset division Capital Markets Strategist Tim Murray wrote the following white paper on asset allocation.

Many investors were bracing for a recession in 2022 as they muddled through an array of challenges, including runaway inflation, an extremely hawkish Federal Reserve, geopolitical turmoil, and rapidly deteriorating economic data.

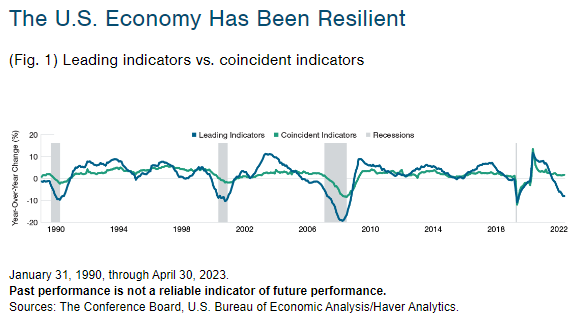

Despite these headwinds, the U.S. economy has remained surprisingly resilient, and the widely anticipated recession has not yet come to pass. The breakdown in the normal relationship between the year-over-year changes in the Conference Board’s Leading Economic Index and its Coincident Economic Index captures this unusual dynamic.

Looking Ahead

The leading index is designed to gauge how the economy might behave in the next three to four months. Typically, when this forward-looking indicator deteriorates, the coincident index, which reflects current economic conditions, follows the same trajectory within a few months. This time has been different. While the leading index has been falling sharply since July 2022, the coincident index has remained stubbornly positive.

Key factors that have supported the economy remain in play. U.S. consumers still have excess savings to spend. They have also benefited from falling inflation—especially in energy costs—and low unemployment. Manufacturing activity also appears to be stabilizing, as bloated inventories have declined to normal levels. Further, despite elevated mortgage rates, housing construction is picking up in response to low supply.

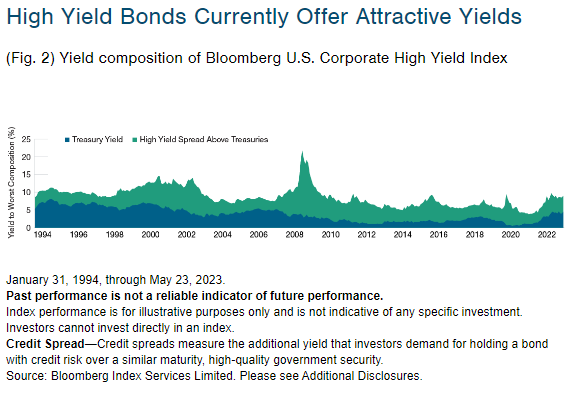

Still, caution is warranted. The lagged effects of higher interest rates and tighter bank credit conditions could weigh meaningfully on economic activity. In this uncertain environment, the healthy yield offered by high yield bonds could provide a buffer for investors.

High yield bonds tend to be sensitive to economic events. However, they currently offer attractive yields, and active security selection could help to identify issuers with elevated interest coverage ratios and low leverage ratios that might suffer less in a recessionary scenario. As a result, our Asset Allocation Committee is overweight to high yield bonds. We believe the asset class offers an attractive risk/reward trade-off in the current environment.

For more news, information, and analysis, visit the Active ETF Channel.

Additional Disclosures

Bloomberg® and Bloomberg U.S. Corporate High Yield Index are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by T. Rowe Price. Bloomberg is not affiliated with T. Rowe Price, and Bloomberg does not approve, endorse, review, or recommend T. Rowe Price. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to T. Rowe Price.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of May 2023 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy. Actual future outcomes may differ materially from any estimates or forward-looking statements provided.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. Fixed‑income securities are subject to credit risk, liquidity risk, call risk, and interest-rate risk. As interest rates rise, bond prices generally fall. Investments in high-yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2023 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

202306-2987497