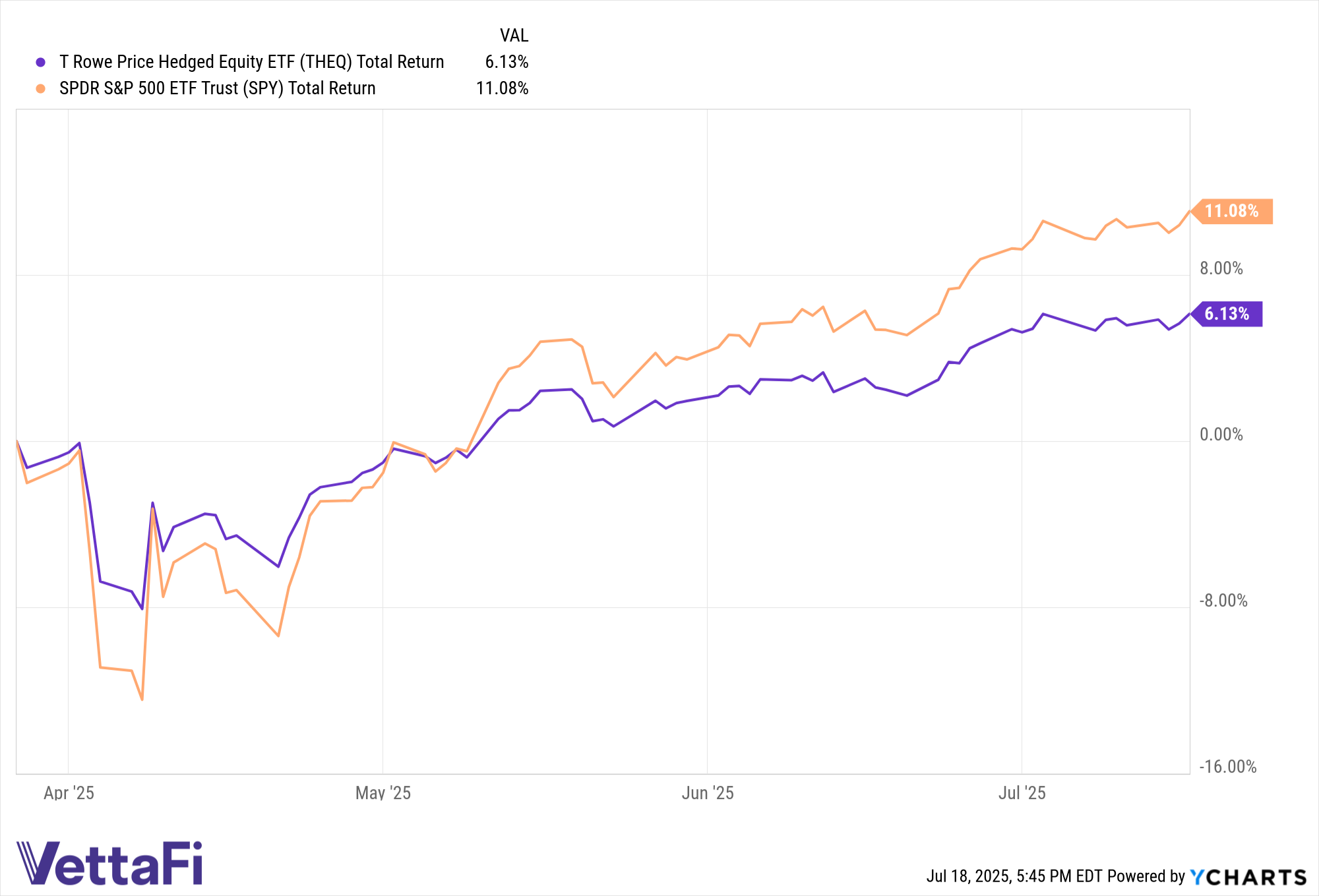

Second quarter earnings season kicked off with an impressive showing from banks, coupled with a mostly in-line inflation print for June. However, stress fractures could be spreading across tariff-sensitive goods sectors, while U.S. tariff rates remain unpredictable and volatile. In this year’s mixed and muddled market environment, dynamic risk management strategies like the T. Rowe Hedged Equity ETF (THEQ) appear well positioned.

Consumer sentiment regarding inflation improved in July, though it remains significantly below 2024 numbers according to University of Michigan survey data. With second quarter earnings season underway, investors will be closely watching for company predictions of tariff impacts in the second half. Meanwhile, the current administration is in tense trade negotiations with the EU, threatening 15–20% tariffs on the bloc, reported the FT.

Ongoing changes to tariff rates, the inflationary impacts of tariffs within the U.S., and geopolitical risks all create the potential for heightened volatility in the second half. Investors looking to hedge their equity exposures with a dynamic strategy would do well to consider THEQ.

Sean McWilliams, portfolio manager of the T. Rowe Hedged Equity ETF (THEQ), will be a part of the upcoming Alternatives Symposium hosted on the VettaFi platform on July 31, 2025. You can pre-register here.

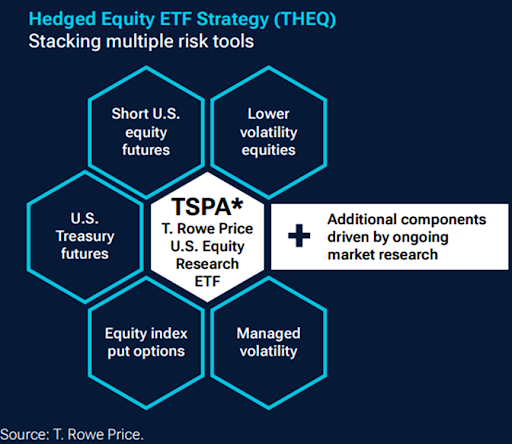

Under the Hood of THEQ’s Layered Risk Management Strategy

At its core, THEQ invests in the T. Rowe Price U.S. Equity Research ETF (TSPA). TSPA maintains the style and risk profile of the S&P 500, but with the addition of active management benefits. THEQ combines TSPA exposure with low volatility equities identified by the T. Rowe Price Integrated Equity team. The fund then overlays the equity exposure with a multi-pronged risk management strategy that responds to changing market dynamics.

The fund uses equity index futures to manage volatility in different risk environments. This includes decreasing equity exposures through the futures when equity risk is elevated, and increasing it when risk is diminished. The overall outcome seeks to provide reduced portfolio volatility for investors.

THEQ also uses U.S. treasury interest rate futures for diversified performance. These exposures prove beneficial during periods of strong market drawdowns driven by economic decline. This interest rate exposure is also dynamic, changing to accommodate shifts in longer versus shorter rate attractiveness as well as rate and equity correlations.

The final component of THEQ’s risk management strategy entails buying equity index put options. The fund managers select put options that offer protection in the event of rapid market decline while also preserving long-term return potential as much as possible. Options positions account for the rest of the risk mitigation strategies employed within the fund.

THEQ’s actively managed strategy also keeps it dynamic in changing market environments. The PMs can adjust the risk overlay to respond to emerging risks, offering flexibility in uncertain times. THEQ carries a competitive expense ratio of 0.46%.

For more news, information, and strategy, visit the Active ETF Channel.