Being on the path to recovery for 2021 means accounting for risks and pushing through tricky areas. In the global market outlook from T. Rowe Price, “Managing to the Other Side,” CIOs David Giroux, Equity and Multi-Asset, Justin Thomson, International Equity, and Mark Vaselkiv, Fixed Income, explored the ways to look at 2021 and seek fixed income yield with acceptable risk in today’s market. There’s also the consideration of politics through its relation with the pandemic and how to find the right way to take on key issues.

In 2020, the pandemic led to lower sovereign yields, even while central bank liquidity infusions allowed for stabilized global credit markets. These duel trends produced strongly positive returns across most fixed income sectors.

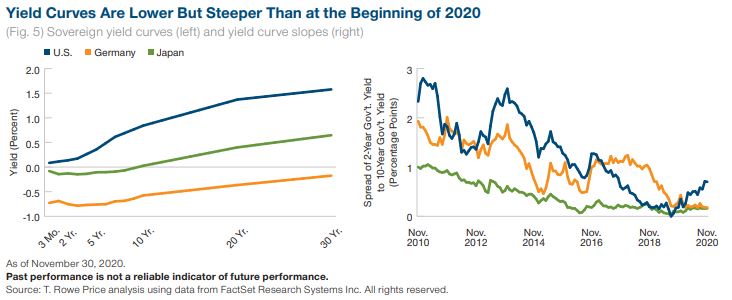

For 2021, however, “investors face a more challenging environment,” Vaselkiv stated. “With short‑term yields at

ultralow or negative levels and the U.S. yield curve steepening as economic growth and inflation expectations

revive interest rates, the risk could become a critical issue, he cautions.”

With investment-grade and high yield credit spreads closer to their historical norms, credit markets also no longer appear as attractive as they did after central banks launched their rescue operations in 2020. Yes, the pandemic’s effects still linger, but active sector and security selection are likely to play more critical roles in seeking yield and managing risk in 2021.

“For credit investors, the flood of new U.S. dollar‑denominated corporate issuance seen in 2020—an estimated $2 trillion in investment‑grade and more than $500 billion in high yield debt— offers both potential opportunities and additional risks,” Vaselkiv said.

In an environment where short‑term rates are at, or close to zero, but prospects for a post‑pandemic recovery appear to be brightening, duration could become a top issue for many fixed-income investors in 2021. With that in mind, Vaselkiv warned, “extended durations for high‑quality sovereigns and investment‑grade corporates mean that even modest upticks in interest rates and inflation could produce significant capital losses on those assets.”

One can also consider potential opportunities in floating rate bank loans and emerging market debt. Bank loans sit higher in the borrower’s capital structure than high yield bonds, which has historically resulted in higher recoveries in default situations. The floating rate feature of bank loans also gives them an extremely low duration profile, but with much higher yields.

“Fixed income assets outside the U.S. also could hold opportunities for global bond investors in 2021,” according to Vaselkiv. “A weaker U.S. dollar,” he added, “could enhance that appeal by potentially boosting returns on nondollar assets for dollar‑based investors and potentially improving the creditworthiness of U.S. dollar bond issuers.”

A Pandemic In A Time Of Politics

The social and economic upheaval caused by the pandemic could worsen political divisions. The tensions between the U.S. and China are another potential flashpoint. In the U.S., the Biden administration is widely expected to seek additional fiscal stimulus to bolster the economy. The administration will have to decide whether and how to challenge Beijing on trade, IP rights, human rights, and other issues.

Given that a hardline trade policy toward China has broad bipartisan support in Washington, Thomson says he doesn’t expect the new administration to roll back the tariffs on Chinese goods imposed by President Trump. However, the intensity of the trade conflict might be reduced. Control of IP, on the other hand, is likely to remain a key battleground.

IP conflict could pose a potential economic risk. It also could create new opportunities for investors, as China seeks to develop its own supply chains, including an onshore semiconductor industry. Meanwhile, Beijing’s campaign to bring Hong Kong under tighter control appears to have achieved its objective.

Shifting thoughts to Brexit, Thomson believes there’s a workable set of post-Brexit arrangements that can be achieved. This could have positive implications for the British pound versus the U.S. dollar, potentially boosting returns on sterling-denominated assets for non-British investors.

Lastly, if new vaccines and continued fiscal and monetary stimulus support a return to more normal economic conditions in 2021, a key question will be how quickly global labor markets improve as a result.

Looking at all of the expectations for 2021, in both equity and credit markets, T. Rowe Price investment leaders state, “the uneven impact of the pandemic and the recovery on countries, industries, and individual companies is likely to make strong fundamental analysis and skilled active security selection a critical component of investment success.”

For more on active strategies, visit our Active ETFs Channel.