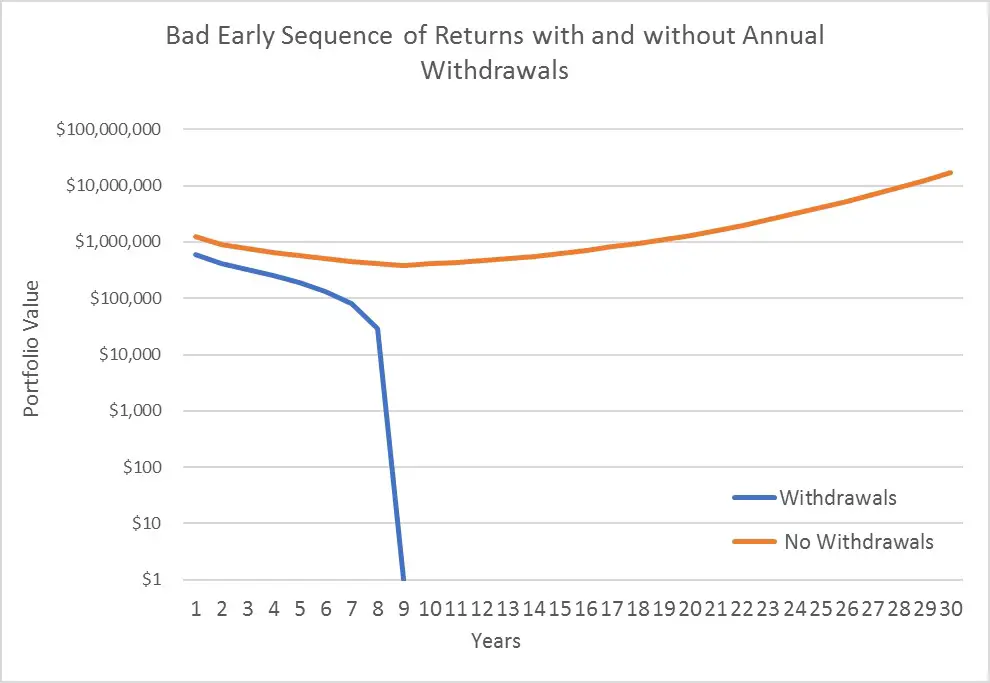

I’ve posted before about sequence-of-return risk, or “sequence risk” for short. Sequence risk is when several years of bad returns early in retirement cause a portfolio to run out of money too soon. This risk applies specifically to retirement because retirees withdraw money from their portfolios regularly to fund living expenses. This graph shows the huge impact that an early sequence of bad returns can have on portfolio value when annual inflation-adjusted withdrawals are made (blue line).

In contrast, when there are no withdrawals (orange line) the long-term impacts of a bad early sequence of returns can be relatively minimal due to math that’s explained more here.

To minimize sequence risk in my own retirement, I devised a rather elaborate “bucket investing” plan, where I withdraw from cash and bonds¹ early in retirement, giving stocks in my portfolio more time to grow and recover from any early declines.

But even back when I was devising my plan I knew it was potentially inconsistent with some research by Javier Estrada of the IESE Business School in Barcelona, Spain. Estrada used 110 years of returns data from 19 countries and showed that a 100% stock portfolio has often performed as good or better than bucket-type approaches. While that sounds promising for an all-stock retirement portfolio, I still thought it was prudent to guard against sequence risk in my own retirement.

So, I was intrigued when I saw a new research paper by Estrada that casts more light on sequence risk. If you choose only one investing research article to read this year, Estrada’s paper on sequence risk is my top pick, particularly if you’re an investor nearing or in retirement. Estrada explains his research in a way that is refreshingly understandable for the layperson. But even so, I thought it would be worth summarizing some key points from his new paper and presenting a few of my related observations as a mindful investor.

What is Risk?

The standard measure of “risk” is the product of:

- The probability or likelihood of a negative event occurring and

- The magnitude of the negative event when it occurs.

In the world of risk assessment, a 90% chance of stubbing my toe in one sport, and a 1% chance of breaking my leg in another sport pose similar levels of risk. One has a high probability of a minor negative event and the other has a low probability of a pretty serious negative event. In this case, both sports seem pretty safe, but if one sport instead had a 90% chance of a broken leg, that would be too risky for me.

So, to determine the seriousness of sequence risk, we need to look at both its likelihood of occurring (probability) and how bad the outcome is when it occurs (magnitude).

How Likely Is Sequence Risk?

The blue line on the top graph looks super scary, but how likely is that sort of outcome? Amazingly, back when I was devising my retirement plan, I couldn’t find a straightforward answer to that question. For this reason, I performed my own calculations, which suggested my specific investing and withdrawal plan was unlikely to fail.

Helpfully, Estrada estimates the probabilities of portfolio failure due to sequence risk in several ways that are more widely applicable. I won’t describe his methods in detail, but in general, Estrada uses S&P 500 annual return data going back to 1900 to estimate the probabilities that a bad sequence of early returns would cause an all-stock portfolio to fail (defined as running out of money in less than 30 years).

Here are the key results based on all 91 overlapping 30-year periods since 1900:

- A 4% (inflation-adjusted) annual withdrawal rate would have failed only four times, a failure rate of 4.4%.

- With a reduced withdrawal rate of 3.5%, there were zero failures.

These findings are generally consistent with past “safe withdrawal rate” studies. But Estrada goes further and finds:

- Among the four failed sequences of returns, there is only a 1% to 9% chance that they would cause portfolio failure again if the offending sequence occurred in a different order.

This means that the four historical failures were not caused by the general prevalence of poor returns in these periods, but instead by a relatively peculiar sequence of bad returns.

To examine how likely these peculiar sequences might be in the future, Estrada conducted a Monte Carlo simulation where historical return sequences were shuffled 10,000 times. This simulation showed that:

- Peculiarly bad sequences are expected to cause portfolio failure about 10% of the time at an approximate withdrawal rate of 3.5%.

This is the clearest probability forecast for sequence risk that I’ve ever seen.

How Bad is Sequence Risk?

The 10% probability of sequence risk defines failure as when the portfolio completely runs out of money before 30 years. When it comes to retirement planning, that’s pretty much the worst possible outcome. But clearly, other possible negative outcomes aren’t so disastrous. In my view, running out of money is probably the least likely of undesirable outcomes.

Why? Well, think about what would happen after a few years of watching your portfolio value plummet. Would you just blithely continue spending at the same rate until every last penny was used up and you were out on the street? Perhaps some people would. But most reasonably aware people would decide to hit the spending brakes before careening off the retirement road.

Estrada helps with this question too. He points out that all these failure probabilities are really about the interplay of both sequences and withdrawal rates. This means that portfolio failure is not a foregone conclusion, even in the face of a peculiarly bad sequence, assuming the investor is willing to take action. Estrada devises a fairly simple procedure for determining when and how much withdrawal rates should be reduced as early bad sequences start to play out. His procedure ensures that the portfolio is unlikely to fail and can be applied in real-time.

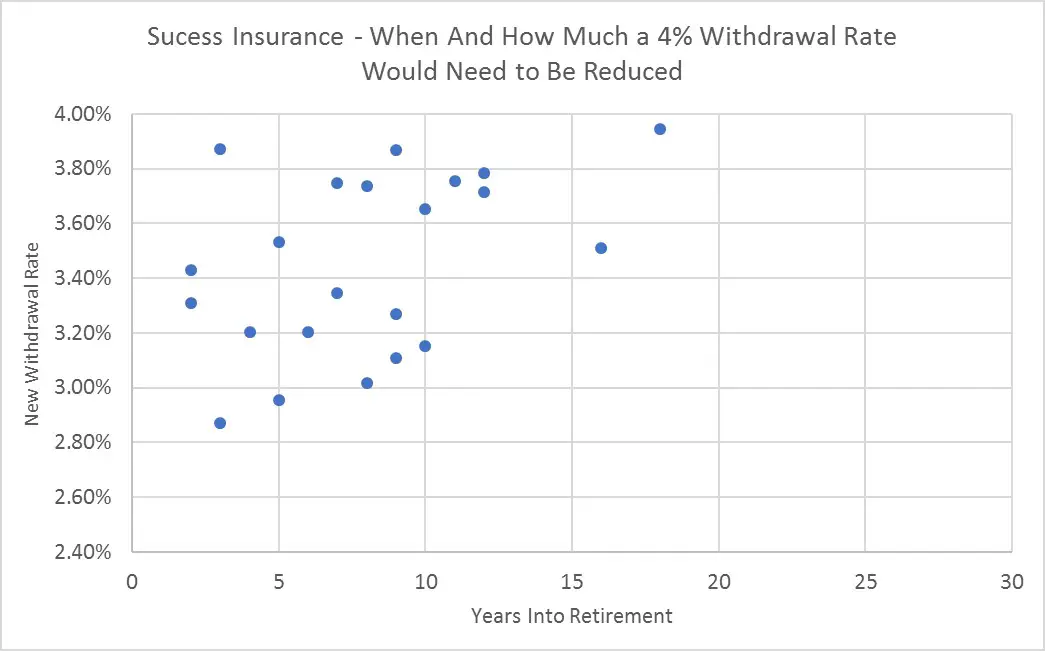

Estrada applied his flexible withdrawal rate procedure to the historical 91 overlapping 30-year periods. He found that withdrawal rate reductions that maximize portfolio success would have only been necessary in 22 cases or 24% of the periods. When and how much the withdrawal rates had to be reduced in these 22 cases is shown in this graph, which I generated using one of Estrada’s tables.

As opposed to simply measuring portfolio failure, this graph gives us a much more nuanced measure of the negative outcomes likely from sequence risk.

Importantly, the results are clumped in the upper left corner of the graph, which indicates that in most cases, only a relatively modest withdrawal rate reduction would be needed and usually pretty early in retirement. In other words, none of these cases results in the theoretical worst-case portfolio failure that is usually the unrealistic focus of sequence risk studies. In fact, none of these cases even involves steep spending cuts very late into retirement.

To better grasp the meaning of this flexible withdrawal procedure, let’s assume a retiree started with a $60,000 initial withdrawal on a $1.5 million portfolio and was forced to reduce from 4% inflation-adjusted annual withdrawals to 3% at various points in the first 10 years. (I assumed an inflation rate of 3% here.) Under these assumptions, the equivalent dollar values for planned versus new, reduced withdrawals are shown in this table.

| Retirement Year | Planned Withdrawal at 4% | New Withdrawal at 3% |

| 3 | $63,654 | $47,740 |

| 6 | $69,556 | $52,167 |

| 10 | $78,286 | $58,715 |

While these new withdrawal rates would require some pretty painful spending adjustments, they seem unlikely to destroy the retiree’s accustomed quality of life. And let’s not forget that in 22 of 24 cases, the recommended withdrawal reductions are less severe than the 3% level assumed in the table.

Estrada also points out that the same math applies to very good sequences too, which are just as likely to occur as very bad sequences. For example, he found that 10% of the time the safe withdrawal rate was more than 12%!

This means that Estrada’s recommended withdrawal rate reductions are not necessarily permanent. In many cases, stock returns could subsequently improve sufficiently that the withdrawal rate could be readjusted upward again, perhaps even to levels above the original 4% rate. So, none of these example reductions necessarily result in a life sentence of a bleak retirement.

Putting Sequence Risk In Perspective

We can sum up that, if history is any guide:

- There is a 10% chance of complete portfolio failure at a 3.5% withdrawal rate, but only if we completely ignore our investments during retirement.

- And if we monitor our investments, there is a 24% chance that relatively modest, and possibly temporary, withdrawal reductions might be necessary.²

Unless you pay zero attention, the complete failure of an all-stock portfolio turns out to be a negligible risk.

I thought of Estrada’s findings when I recently read about a local man who was arrested for investment adviser fraud. This licensed adviser allegedly stole several hundred thousand dollars from at least five local retirees. My town has a population of only 50,000, and amazingly, this isn’t the only local incident of investment fraud that I’ve heard about since I moved here.

According to several studies, it turns out that somewhere between 7% and 10% of older investors will be the victims of investment fraud over the course of their lifetimes! Perhaps this doesn’t surprise you. But before finding these fraud rates, I thought of adviser fraud as a freak accident limited to the rare Bernie Madoff style con-artist and a few super-rich investors.

Fraud risk may be widely misperceived because the adviser industry understandably seeks to downplay fraud risks in media interactions and client communications. But to me, a 10% chance of having a big chunk of my portfolio stolen, seems much more egregious than the moderate risks associated with a bad sequence of returns. And yet, compared to sequence risk, no one seems to talk about fraud very much.

Conclusions

If Estrada’s new study had been available a few years ago when I was crafting my own retirement plan, I likely would have just selected a 100% stock portfolio and a reasonably cautious withdrawal rate. I would have dispensed with the bucket approach entirely.

But hindsight is always 20/20. I’ll stick to my bucket investing plan because, in my view, a plan you don’t follow is actually worse than no plan at all. If I revised my plan every year or two based on the latest research, my retirement would meander like the town drunk lurching from one potential watering hole to the next.

And when my short-term bucket is used up in a few years, I will have a 100% stock portfolio for the rest of my retirement. So, Estrada’s study gives me a new confidence that the rest of my retirement will likely be a financial success.

Originally published by Mindfully Investing, 12/7/20

1 – My analysis of bucket investing includes bonds as a theoretical exercise. But because of the current super-low bond yields and corresponding low expected future bond returns, my short-term bucket contains cash only at this time.

2 – Early retirees should take note that these findings are all based on a 30-year retirement. If you plan to be retired for 40 or 50 years, then your risks will likely be somewhat higher and safe withdrawal rates somewhat lower than these conclusions. But I wouldn’t, therefore, conclude that sequence risk is huge for the early retiree. The flexible withdrawal strategy proposed by Estrada is feasible for any retirement timespan. Or put another way, if you’re willing to live frugally enough, Estrada’s risk estimates are entirely realistic for the early retiree.