Diversification is finally paying off. After more than a decade of U.S. dominance, international equity ETFs are enjoying monster inflows, outpacing their domestic counterparts for the first time since early 2023. This structural shift is being fueled by a potent mix of shifting earnings momentum abroad and a cyclically weakening dollar.

Many investors are unwittingly making a dual bet: one on foreign corporate earnings, and another on the greenback itself. While the allure of lower P/E ratios in Europe and Asia is drawing capital across the ocean, a cloudier outlook for the dollar — and often does — eviscerate those valuation gains in an unhedged portfolio.

Embedded Currency Exposure

Historically, the dollar has reigned supreme as the world’s ultimate “safe haven” currency, strengthening during periods of global conflict or macro uncertainty as investors sought shelter. However, that traditional dynamic is beginning to crack under the weight of rising national debt levels and persistent fiscal deficits. As these pressures mount, some investor concerns over the gradual debasement of the dollar have cast a shadow over its long-term stability as the undisputed global reserve currency. Recognizing these structural vulnerabilities, both institutional investors and global central banks are now slowly starting to diversify their currency exposure.

These brewing fiscal concerns didn’t just stay in the headlines – they translated directly into market performance, as evidenced by the currency whiplash in 2025. The MSCI EAFE Index delivered a robust 24% return in local terms, but a sliding dollar swelled that figure to 31% for U.S. investors. That 7% “currency gift” was a reminder of how quickly the turn of the dollar can provide a tailwind — and how abruptly it can pivot. Historically, an unhedged international ETF does come with higher volatility compared to its hedged counterpart.

International Bond ETFs

In the equity space, unhedged exposure remains the default among most broad international funds. But in fixed income, hedging is the standard for reducing volatility, making most international debt ETFs pure bets on rates and unhedged bond ETFs a much more specialized, speculative choice. The typical total international bond heavyweights, such as the Vanguard Total International Bond Index Fund ETF (BNDX) and the iShares Core International Aggregate Bond ETF (IAGG), are dollar-hedged by design to maintain the low-volatility profile typical of fixed income. Without that hedge, currency attribution could easily dominate interest rate attribution – meaning, a “conservative” international bond fund could well end up behaving more like a volatile currency trade than a stable income producer.

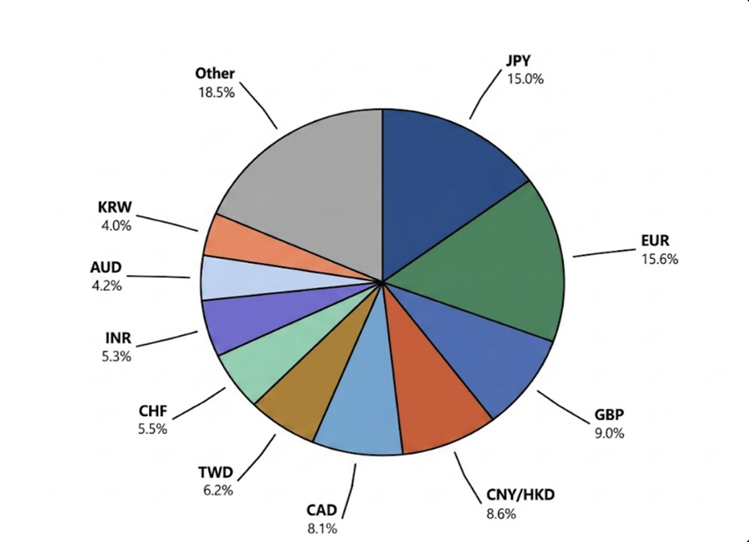

Biggest Players: The FX Footprint

A quick glance at the breakdown of foreign currency exposures reveals that some of the largest, most liquid international equity ETFs are decently diversified on the forex front. The single largest international ETF, the Vanguard Total International Stock Index Fund ETF (VXUS), comprises both developed and emerging markets. The euro, yen and pound make up the lion’s share of exposure. If these three currencies strengthen against the dollar, VXUS gets a performance “gift” regardless of how the underlying stocks move. Unlike many developed-market-only ETFs (like VEA), VXUS includes a significant chunk of emerging markets. This adds exposure to currencies that can be more volatile but often provide higher growth potential.

As of April 2026, VXUS holds more than 8,000 stocks across 47 countries.

Vanguard Total International Stock Index Fund ETF (VXUS)

Foreign Currency Exposure Breakdown (Approx.)

Case for Hedging: Bullish on the Country, Not the Currency

However, there are cases, particularly when placing single-country bets, where investors may have conviction on the regional market but want to strip out the currency risk. This typically calls for a strategy aimed at hedging out currency risk and gaining pureplay stock exposure. For instance, the yen has been wobbly but Japanese equity returns have been strong. In local currency terms, the Nikkei rose 26% in 2025. But in dollar terms, it rose 33% because the yen also strengthened.

Case in point: The WisdomTree Japan Hedged Equity (DXJ) is up 15% year-to-date, while the unhedged iShares MSCI Japan ETF (EWJ) has risen only 9% from currency drag. Despite holding virtually the same blue-chip constituents, the two funds are telling different stories. Both are benefiting from Prime Minister Sanae Takaichi’s focus on AI and defense, but only the hedged investor is isolating the equity risk and capturing the “pure” version of that growth, insulated from the yen’s persistent interference.

Bottom Line: Mind the Gap

Currency exposure is no longer a passive byproduct — it’s an active decision that can shape returns. Unhedged strategies can boost performance when the dollar weakens, but they can also add volatility that can overwhelm an equity thesis. The choice should reflect conviction. In today’s volatile macro environment, managing this tradeoff can make the difference between capturing alpha and giving it back.

For more news, information, and analysis, visit VettaFi | ETF Trends.