Corporations aren’t the only major source that can drive capital expenditures (CapEx) spending on artificial intelligence infrastructure.

Recent insights from Alger highlighted how spending from foreign governments could serve as a key accelerator for AI CapEx spending. Namely, the insights post focused on how governmental programs around the world are amplifying efforts to develop “sovereign AI.” In layman’s terms, sovereign AI refers to a country’s ability to curate its own AI infrastructure, data centers, and locally-trained models.

We believe the justification behind doing so certainly makes a good deal of sense at face value. In an era where data security and protection of intellectual property is crucial, the best defense for a country may be to rely on its own network. Currently, U.S.- and China-based platforms dominate the competition. However, the Alger post notes that South Korea, Saudi Arabia, and the EU have made significant investments as well.

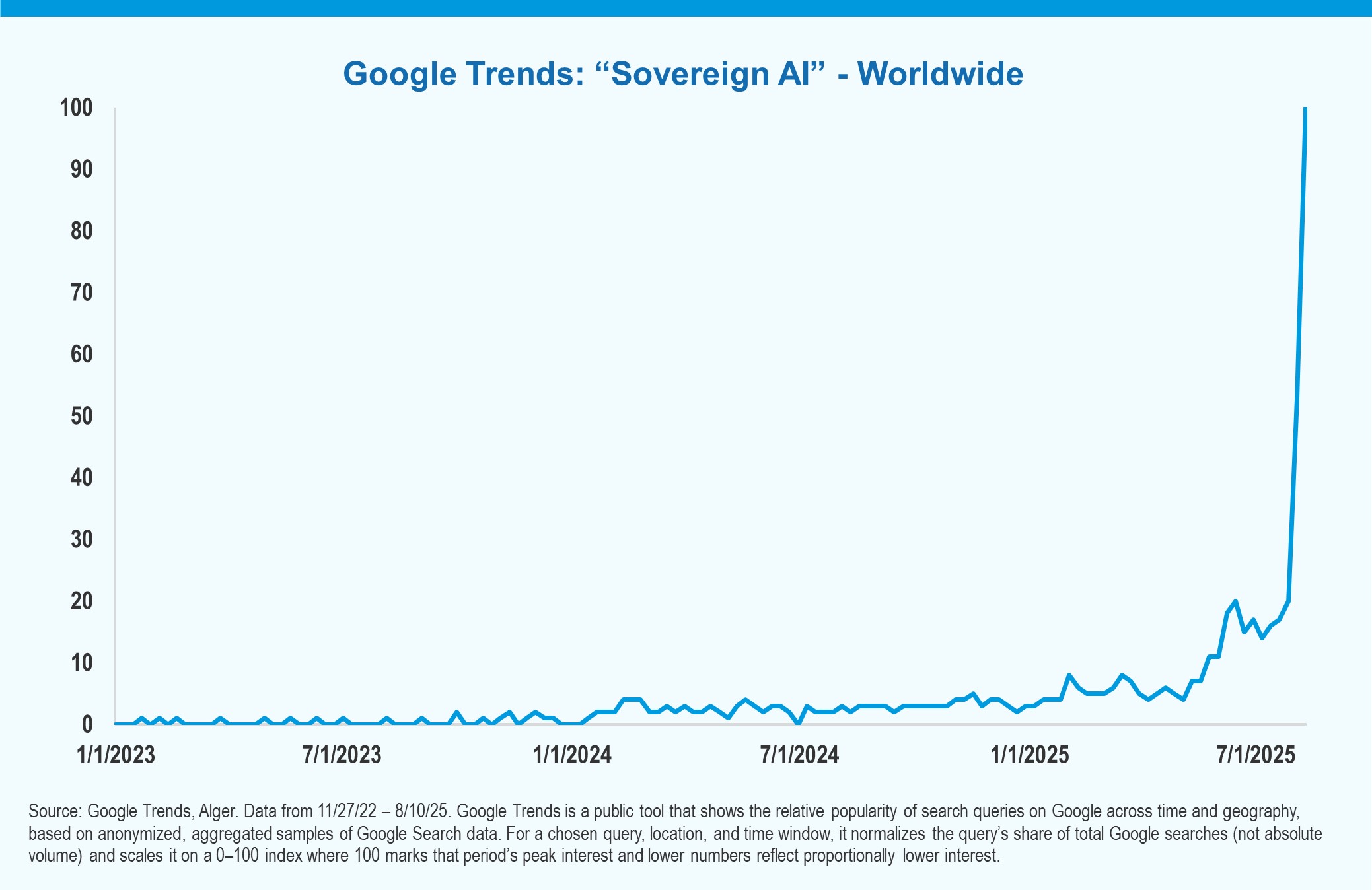

The chart above takes a look at worldwide search interest in sovereign AI. As countries around the world have rolled out new plans to build out their own AI infrastructure, interest has spiked in learning more about sovereign AI and its importance going forward.

Sovereign AI could represent a crucial step forward for driving further AI CapEx spending. Not only could sovereign AI help promote national security, thorough AI infrastructure could also help countries and their individual companies remain competitive as the AI space continues to innovate. While much of the sovereign AI spending may be focused on international companies, many U.S. providers can stand to benefit as well.

ALAI Taps into Growing AI Adoption

In our view, advisors and investors looking to capitalize on growing AI CapEx spending may want to turn to the Alger AI Enablers & Adopters ETF (ALAI). The actively managed fund focuses on investing in companies engaged in furthering AI innovation and adoption.

This fund selects companies to invest in through its proprietary investment research process. That process is designed to find stocks that are seeing Positive Dynamic Change. The term refers to companies that are either witnessing High Unit Volume Growth or Positive Lifecycle Change.

High Unit Volume Growth companies are those with strong business models that are experiencing growing revenues, significant market growth and rising demand. Meanwhile, Positive Lifecycle Change companies are those that are well-positioned to benefit from new management teams, innovations, or even government regulations. When combined, this strategy can seek out companies that are both seeing broad demand and also poised to benefit from favorable conditions in the long-term.

For more news, information, and strategy, visit the Artificial Intelligence Content Hub.

Disclosure Information

Click here for more information on the Alger AI Enablers & Adopters ETF.

The views expressed are the views of Fred Alger Management, LLC (“FAM”) and its affiliates as of October 2025. These views are subject to change at any time and may not represent the views of all portfolio management teams. These views should not be interpreted as a guarantee of the future performance of the markets, any security or any funds managed by FAM. These views are not meant to provide investment advice and should not be considered a recommendation to purchase or sell securities. Holdings and sector allocations are subject to change. Past performance is not indicative of future performance.

Risk Disclosures: Investing in the stock market involves risks, including the potential loss of principal. Growth stocks may be more volatile than other stocks as their prices tend to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Companies involved in, or exposed to, AI-related businesses may have limited product lines, markets, financial resources or personnel as they face intense competition and potentially rapid product obsolescence, and many depend significantly on retaining and growing their consumer base. These companies may be substantially exposed to the market and business risks of other industries or sectors, and may be adversely affected by negative developments impacting those companies, industries or sectors, as well as by loss or impairment of intellectual property rights or misappropriation of their technology. Companies that utilize AI could face reputational harm, competitive harm, and legal liability, and/or an adverse effect on business operations as content, analyses, or recommendations that AI applications produce may be deficient, inaccurate, biased, misleading or incomplete, may lead to errors, and may be used in negligent or criminal ways. AI technology could face increasing regulatory scrutiny in the future, which may limit the development of this technology and impede the future growth. AI companies, especially smaller companies, tend to be more volatile than companies that do not rely heavily on technology. A significant portion of assets will be concentrated in securities in related industries, and may be similarly affected by adverse developments and price movements in such industries. A significant portion of assets may be invested in securities of companies in related sectors, and may be similarly affected by economic, political, or market events and conditions and may be more vulnerable to unfavorable sector developments. Investing in companies of small and medium capitalizations involves the risk that such issuers may have limited product lines or financial resources, lack management depth, or have limited liquidity. The Fund is classified as a “non-diversified fund” under federal securities laws because it can invest in fewer individual companies than a diversified fund. Private placements are offerings of a company’s securities not registered with the SEC and not offered to the public, for which limited information may be available. Such investments are generally considered to be illiquid. Foreign securities involve special risks including currency fluctuations, inefficient trading, political and economic instability, and increased volatility. ADRs and GDRs may be subject to international trade, currency, political, regulatory and diplomatic risks. Active trading may increase transaction costs, brokerage commissions, and taxes, which can lower the return on investment. At times, cash may be a larger position in the portfolio and may underperform relative to equity securities.

ETF shares are based on market price rather than net asset value (“NAV”), as a result, shares may trade at a price greater than NAV (a premium) or less than NAV (a discount). The Fund may also incur brokerage commissions, as well as the cost of the bid/ask spread, when purchase or selling ETF shares. The Fund faces numerous market trading risks, including the potential lack of an active market for Fund shares, losses from trading in secondary markets, periods of high volatility and disruption in the creation and/or redemption process of the Fund. Any of these factors, among others, may lead to the Fund’s shares trading at a premium or discount to NAV. Thus, you may pay more (or less) than NAV when you buy shares of the Fund in the secondary market, and you may receive less (or more) than NAV when you sell those shares in the secondary market. The Manager cannot predict whether shares will trade above (premium), below (discount) or at NAV. The Fund may effect its creations and redemptions for cash, rather than for in-kind securities. Therefore, it may be required to sell portfolio securities and subsequently recognize gains on such sales that the Fund might not have recognized if it were to distribute portfolio securities in-kind. As such, investments in Fund shares may be less tax-efficient than an investment in an ETF that distributes portfolio securities entirely in-kind. Brokerage fees and taxes will be higher than if the Fund sold and redeemed shares in-kind. Certain shareholders, including other funds advised by the Manager or an affiliate of the Manager, may from time to time own a substantial amount of the shares of the Fund. Redemptions by large shareholders could have a significant negative impact on the Fund.

Alger pays compensation to VettaFi to sell various strategies to prospective investors.

The following positions represent firm wide assets under management as of July 31, 2025: Alphabet Inc., 2.27%.

Before investing, carefully consider a Fund’s investment objective, risks, charges, and expenses. For a prospectus and summary prospectus containing this and other information or for a Fund’s most recent month-end performance data, visit www.alger.com, call (800) 992-3863 (for a mutual fund) or (800) 223-3810 (for an ETF), or consult your financial advisor. Read the prospectus and summary prospectus carefully before investing. Distributor: Fred Alger & Company, LLC. All underlying series of The Alger ETF Trust listed on NYSE Arca, Inc. NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.