Summary

- The Alerian MLP Infrastructure Index (AMZI) underlies the Alerian MLP ETF (AMLP), which is celebrating its 15-year anniversary. AMZI is a composite of energy infrastructure MLPs with a quality focus.

- Over the last 15 years, MLPs have provided income (average yield of 7.40%), real asset exposure, and diversification benefits.

- The outlook for MLPs remains constructive driven by expectations for continued distribution growth and the tailwinds associated with free cash flow generation.

With the Alerian MLP ETF (AMLP) celebrating its fifteenth anniversary this week, this note takes a closer look at AMLP’s underlying index, the Alerian MLP Infrastructure Index (AMZI). Continue reading for a brief overview of AMZI, the portfolio benefits of MLPs backed by 15-year data points, and the outlook for the MLP space.

Overview of the AMZI Index

AMZI is a composite of energy infrastructure MLPs, and it launched in November 2009. AMZI has historically had a quality emphasis, given its focus on energy infrastructure MLPs and requirement that constituents pay a distribution. The methodology also includes a liquidity criterion. Constituents must earn the majority of their cash flows from midstream activities. Current AMZI constituents are primarily involved in pipeline transportation of hydrocarbons, gathering and processing, marketing and distribution, liquefaction, and compression.

The index is rebalanced quarterly in March, June, September, and December, according to its methodology. Constituents are weighted based on float-adjusted market capitalization with a 12% cap for individual constituents. Performance data and other index statistics are updated in AMZI’s monthly fact sheet.

15-year snapshot of MLP portfolio benefits.

While the MLP space has changed in many ways over the last 15 years, the core investment case remains largely unchanged. MLPs offer compelling income, real asset exposure (MLPs tend to outperform when inflation is elevated), and typically have a lower correlation with other asset classes. The infographic below highlights some of these qualities.

For income investors, it bears mentioning that AMZI’s yield is currently above its 15-year average of 7.40%. Additionally, AMZI’s negligible correlation with bonds over the last 15 years reinforces MLPs’ diversification benefits in an income portfolio. MLPs also have a noticeably lower correlation with bonds and the S&P 500 than REITs. The FTSE NAREIT Real Estate 50 Index (FNR5) has a 15-year correlation of 0.5 with bonds and 0.7 with the S&P 500.

Of course, one cannot directly invest in AMZI. The ETF wrapper offers the convenience of exposure to a portfolio of MLPs with Form 1099 tax reporting and no concern of unrelated business taxable income for tax-advantaged accounts (read more).

MLP outlook remains constructive.

While trying to predict the next 15 years is a fool’s errand, the outlook for the MLP space remains constructive. The positive outlook is in part underwritten by expectations for continued distribution growth. The majority of AMZI constituents have grown their distributions within the last year (read more). It has been more than four years since a name in AMZI cut its regular distribution.

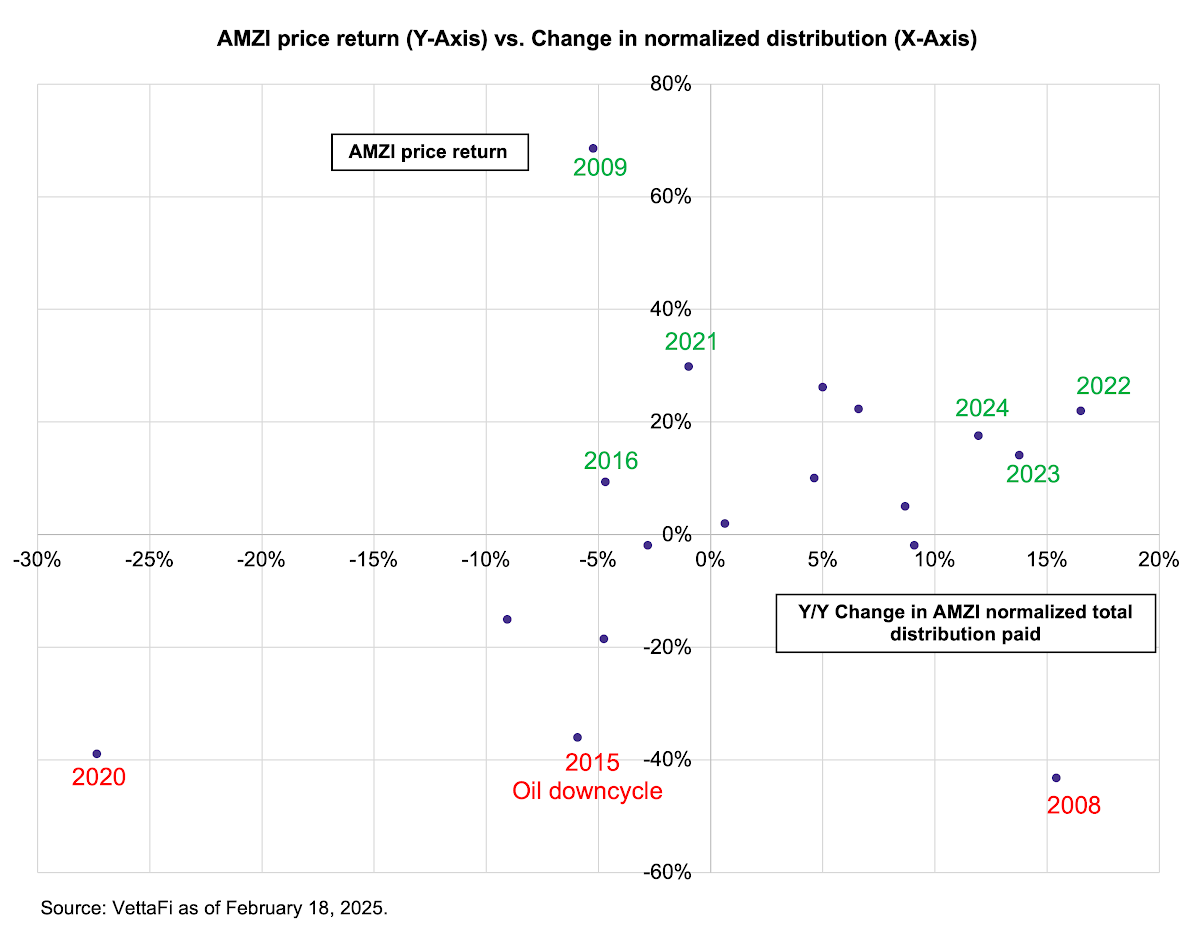

The chart below plots AMZI’s annual price return (vertical axis) against the change in normalized distribution (horizontal axis) going back to 2007. When distributions are growing, performance tends to be positive (top right quadrant). The only exception was 2008, when distributions increased but performance was negative.

Beyond growing distributions, there are other tailwinds for MLPs today. Relative to 15 years ago or even pre-pandemic, MLPs enjoy more financial flexibility from free cash flow generation and reduced leverage. Instead of issuing units to fund capital projects, which was commonplace in 2010, select MLPs are repurchasing their equity. By weighting, over 70% of AMZI has a buyback authorization in place (read more).

Midstream MLPs are expected to continue generating free cash flow. While there are growth opportunities primarily related to natural gas and natural gas liquids, the really hefty capital spending of the 2010s is expected to remain in the rearview. Moderate EBITDA growth is generally expected, and inorganic growth likely continues to play a role for MLPs as well (recent examples).

Despite strong performance over the last five years, MLP valuations have not become stretched. As of August 20, AMZI was trading at a weighted average forward EV/EBITDA multiple of 8.8x based on 2026 consensus estimates. This is comfortably below its 10-year average forward multiple of 9.7x.

Conclusion

Relative to 15 years ago, energy infrastructure MLPs are generally making money in the same way and providing the same portfolio benefits — income, real asset exposure, and diversification benefits. However, MLPs are in a healthier financial position today thanks to free cash flow and stronger balance sheets. The outlook for the space remains constructive given expectations for ongoing free cash flow generation and distribution growth.

Register today for our 60-minute webcast, “Checking MLP/Midstream Fundamentals as 2026 Approaches” on Wednesday, September 3, at 2 p.m. ET. CE credit will be available.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

Related Research:

Energy Infrastructure’s Fit & Function in Portfolios

Midstream/MLP Buybacks Jumped in 2Q25

2Q25 MLP/Midstream Dividend Recap: MLPs Deliver Growth

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLPand MLPB, for which it receives an index licensing fee. However, AMLP and MLPB are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing or trading of AMLP and MLPB.

For more news information and analysis, visit the Energy Infrastructure Content Hub.