Investors looking for economically resilient themes amid tariffs and other global economic uncertainties might want to consider exposure to the music industry. TD Cowen recently highlighted music as “an oasis of stability,” especially with digital goods “unaffected by tariffs.”

The firm views music as a defensive sector because companies like Universal Music Group, Warner Music Group, and Spotify generate revenues from subscription streaming. Given the automated and low-cost nature of these charges, numbers shouldn’t fall off too much in the face of a recession, should it occur.

Music Reasonably Cheap and Portable

Compared to other entertainment options, music has a high value to price proposition.

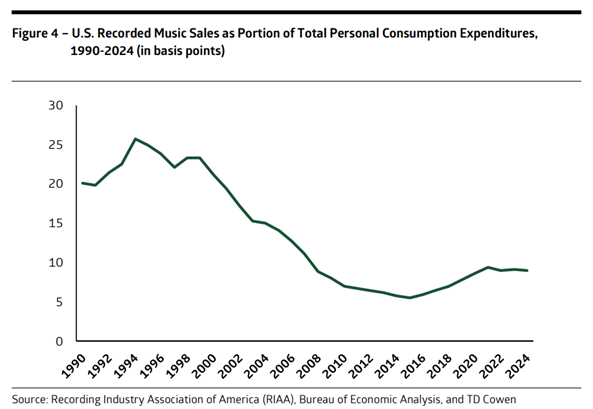

“Consumer spending on recorded music relative to overall personal consumption expenditures remains at less than half the level reached during the peaks in the 1990s before the industry was disrupted by digital distribution,” TD Cowen shared in the note, supported by the accompanying chart below.

Not only is music cheap, but it is benefiting from a vastly improved digital consumer experience via streaming services. Users can listen to “virtually all music ever created” on their phones, according to TD Cowen.

Emotional Connection to Music Makes it More Recession-Proof.

Consumers have strong feelings concerning the music they enjoy that can intensify when their stress levels are heightened. Historically, music has been resilient during recessions, and compared to other forms of discretionary spending, music-related spending appears less at risk.

Broad consumer spending on music streaming was up 12% in 2024 from the prior year, according to TD Cowen estimates. The firm projects music streaming will “sustain high single digits/low double-digit rates with +10% YoY expected in 2025 and +9% YoY in 2026.”

In a recent Barron’s article, BofA Securities analyst Peter Henderson agrees that music could be “relatively recession resilient” if consumers continue to make attending music-related events a priority as the economic environment worsens. This is partly due to the “scarcity value with specific dates and limited shows in a particular area,” he argues, noting that it incentivizes them to buy tickets when they are available.

He also points out that live music doesn’t necessarily require attendees to travel long ways or spend a huge amount beyond the cost of tickets. As such, it can weather recessions well. Tickets are relatively inexpensive compared to other forms of entertainment.

Goldman Sachs analyst Stephen Laszczyk also noted that during recessionary periods, spending on live music increased by 7.3% on average. Meanwhile, overall consumer spending was only up 3.2% during the same periods. Laszczyk says his firm finds the live music space less cyclical than other entertainment mediums.

Streaming Booming

Spotify was solely responsible for payments of $10 billion to the music industry in 2024. That is more than any single company has paid previously. The company also just signed a licensing deal with Universal Music Group.

With streaming service subscriptions climbing globally, the music industry is taking in 10 times as much in payouts as it was 10 years ago. Streaming sales represented $28 billion in revenue for the industry last year.

Investment Potential

How have all these positive trends manifested at the stock level and in the performance of the only pure-play ETF remaining in the category?

KPOP Pops, but ETF No More

South Korean K-pop companies such as SM Entertainment (+58.6%), YG Plus (+48.8%), and YG Entertainment (+42.0%, Cube (24.3%), and Hybe (+23.3%) are all up considerably so far this year. K-pop stocks have “popped” based on investor confidence that tariffs will not be levied on the sector.

This is partly due to the expected cancellation of a ban focused on Korean culture in China and the return of many popular groups that will be releasing new music and touring after a long drought of activity. However, the JAKOTA K-Pop and Korean Entertainment ETF (KPOP), which focused on this area, is no longer. The fund was liquidated on April 4 of this year.

Streaming is Screaming

In the US, the streaming service Spotify is a top-performing stock this year, up 38.8%. Chinese music streaming services are “screaming” as well, with Netease Cloud Music gaining 46.2% this year and Tencent Music up 19.2% during the same period.

Live Music Performance a Mixed Bag

European live concert promoter CTS Eventim AG has been a big beneficiary of positive economic trends in Europe, with the stock rising 38.4% YTD. US live music names have been more of a mixed bag, with Live Nation up 2.5%, outpacing the overall market. Meanwhile, Vivid Seats is down 41.5% after the ticket marketplace reported mixed results and weaker guidance amid rising industry competition for resale tickets. One positive catalyst is that ticket resale company StubHub will go public with the pending listing date. This summer’s live concert activity could spur interest, with pop star Lady Gaga going on tour for the first time in seven years.

MUSQ ETF

The only pure-play ETF offering exposure to this theme is the MUSQ Global Music Industry ETF (MUSQ), and it is up 5.6% YTD, considerably better than the VettaFi Full World Index return of -1.4% and VettaFi 500 Index, down -5.7% for the year. With investors concerned about inflation and economic weakness, music may indeed be a tariff-proof, defensive sector to consider in the current market environment.

For more news, information, and analysis, visit the Disruptive Technology Channel.

VettaFi LLC (“VettaFi”) is the index provider for MUSQ for which it receives an index licensing fee. However, MUSQ are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of MUSQ.