Astoria’s High Conviction Views

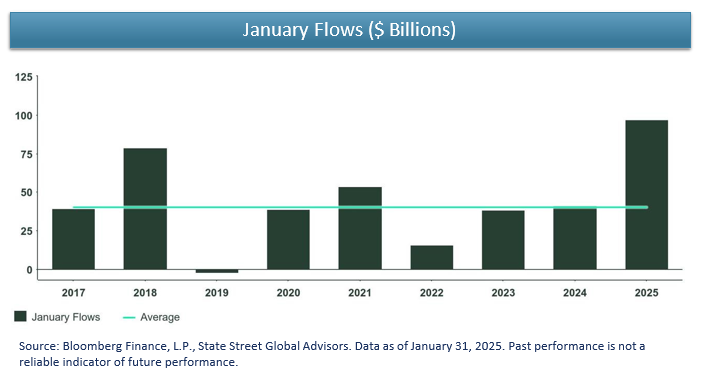

- January ETF flows were over 2x the normal average (most went into US large-cap funds). Why do investors keep pouring money into such equity ETFs despite record high valuations, Mag 7 concentration, and increasing asymmetric risks (i.e., deficit, tariffs, less rate cuts)?

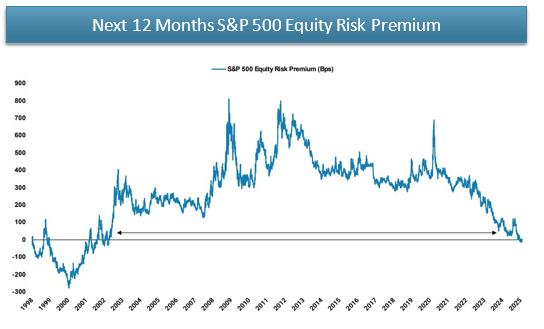

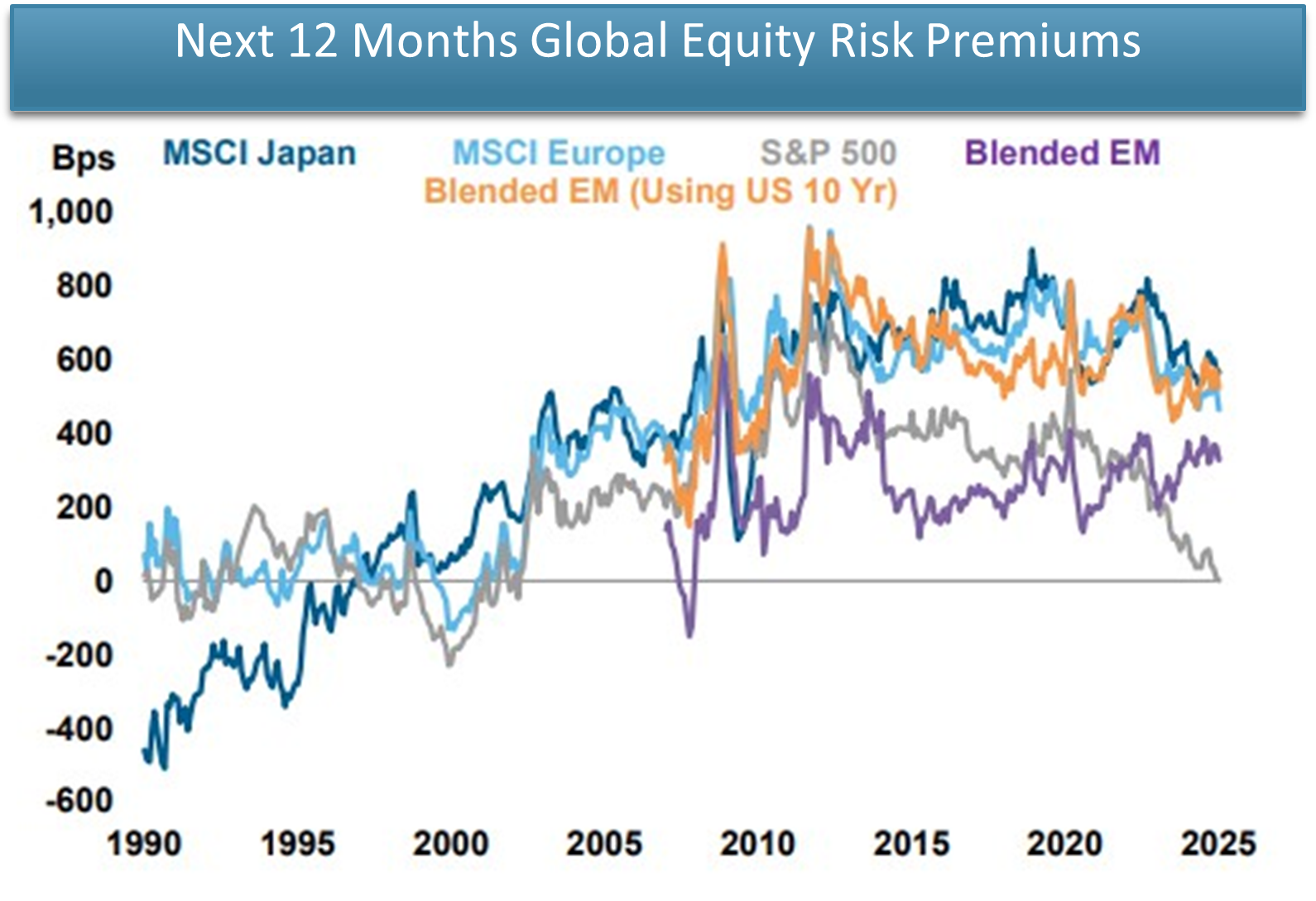

- The US large-cap equity risk premium is near 20-year lows, implying little premium for taking equity risk given high valuations and high rates.

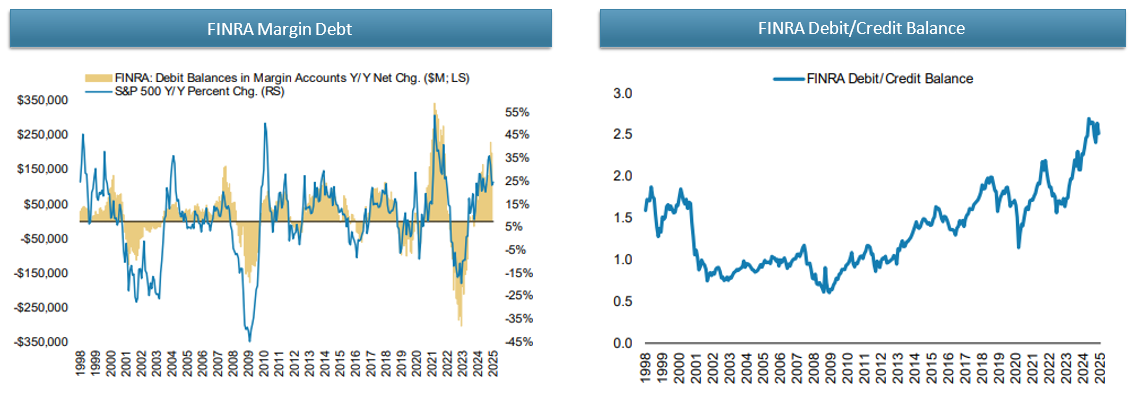

- Leverage is running With increased asymmetric risks and rates that have more risk of increasing than decreasing (inflation running hotter, rate cuts pushed further down the road), we would caution investors who are running higher risk levels.

- Jan ISM Manufacturing PMI is back in expansionary territory with new orders, production, and employment components all stronger than the previous reading.

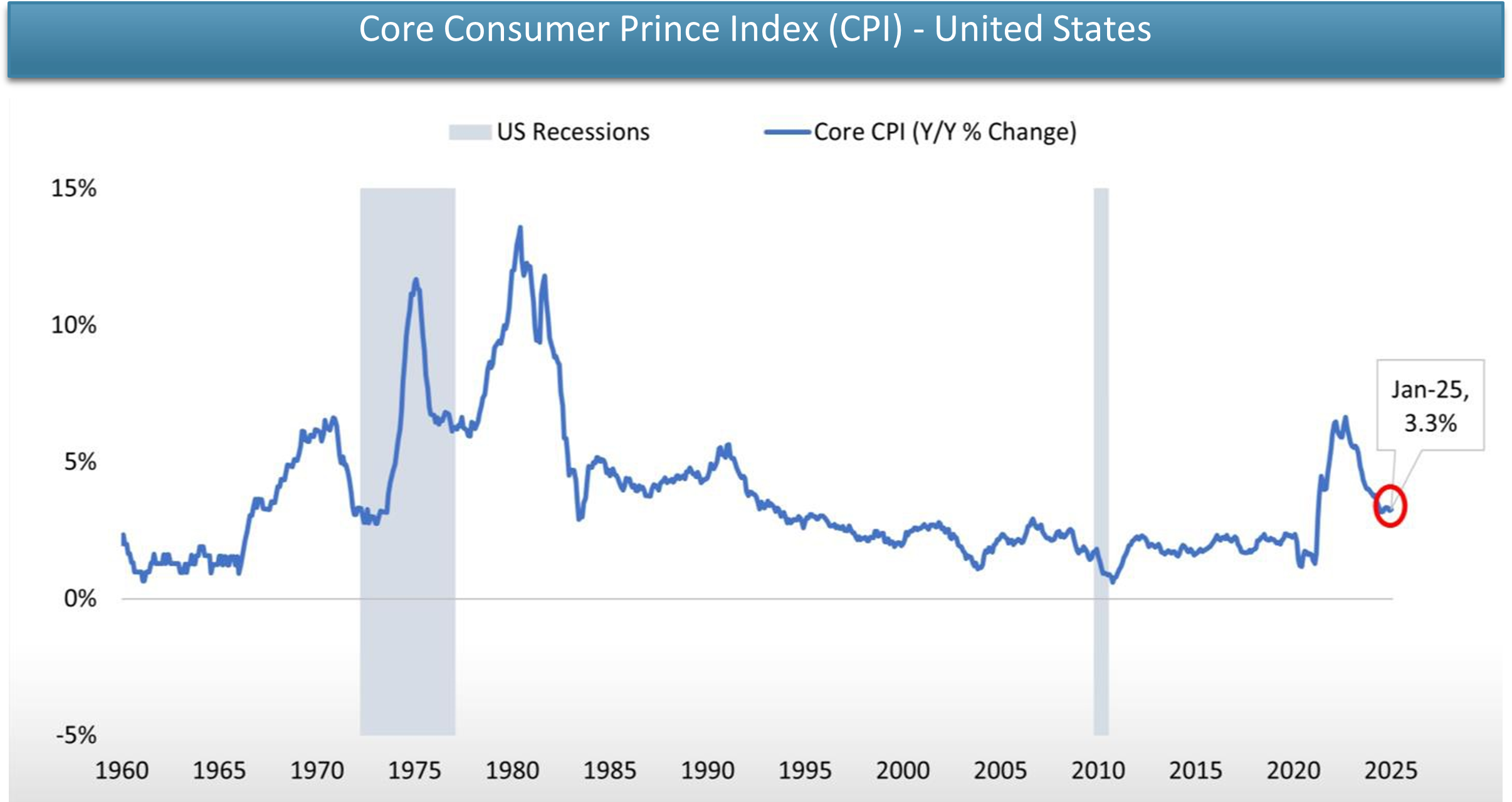

- All Jan CPI measures came in hotter than expected, with the core annualized measure ticking up to 3%. Headline PPI prints also came in above consensus. Worth owning real assets?

- Less tight Senior Loan Officer Survey data points to a rebound in loan growth in 2025. The relative valuation level of the financials sector is below average on a 20-year look-back.

- S&P 500 earnings revisions breadth has remained in negative territory for the last 6 months and continues to fall.

- The spread between earnings growth for Mag 7 the S&P 493 is projected to notably decline in 2025. Mag 7 is expected to see 20% EPS growth while the S&P 493 is expected to see 12% EPS growth (a spread of 800bps). In 2024, this spread was 33%.

- Be careful with equal weighted Most are underweight technology relative to the benchmark. Technology is a long-term winner in our view.

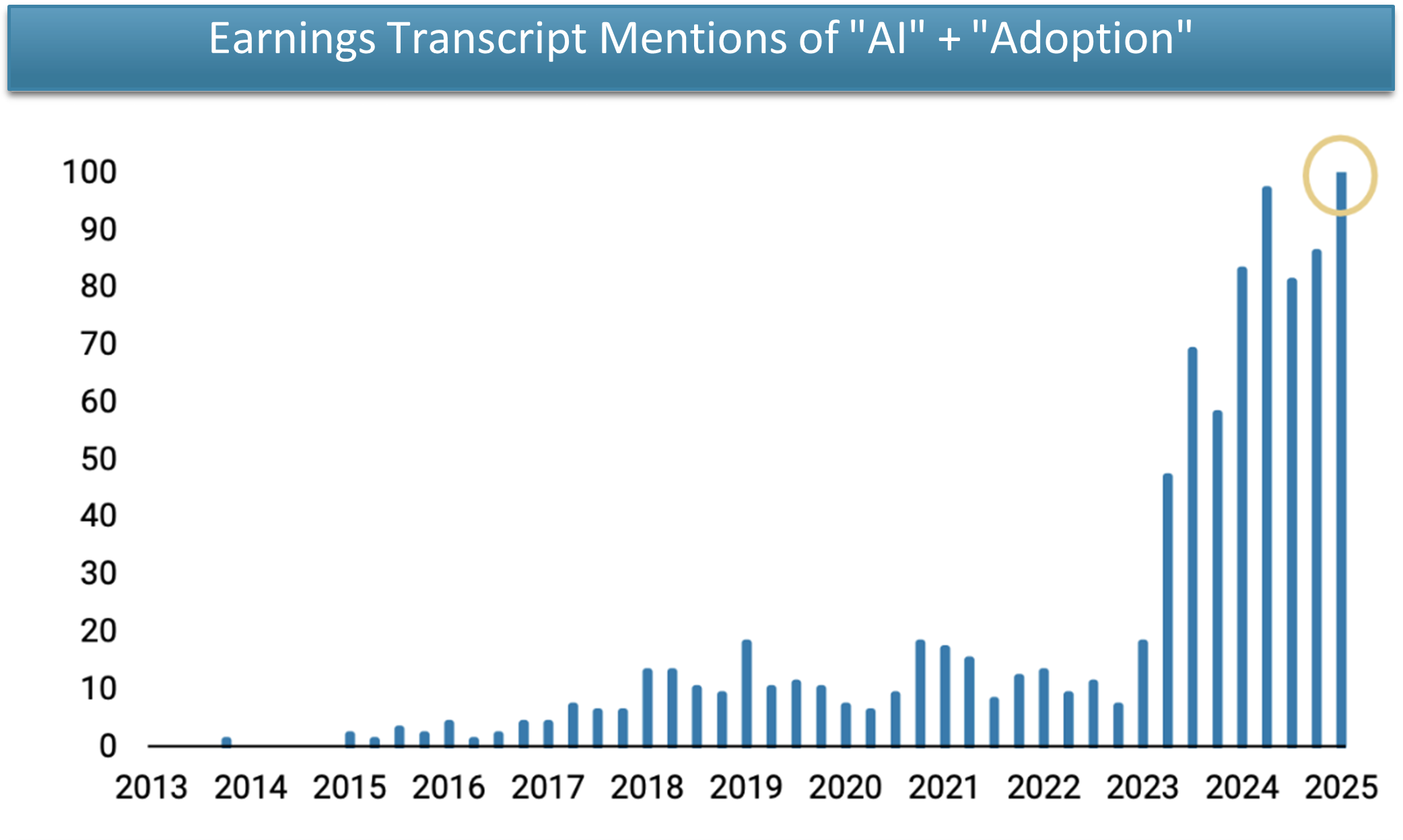

AI mentions in earnings calls are at record highs. At Astoria, we think the opportunities are in the 1) adopters (software + other non-tech industries) 2) data centers 3) power plays as opposed to the enablers (semis/chips) as we navigate the AI cycle.

Source: AlphaSense, Morgan Stanley Research. Includes related terms. Normalized trend shown. US companies > $1B market cap. Data as of February 10, 2025

January ETF flows were over 2x the normal average, with the majority going into US large-cap core funds. Why do investors keep pouring money into such equity ETFs despite record high valuations, increasing asymmetric risks, and greater potential for rate hikes compared to rate cuts?

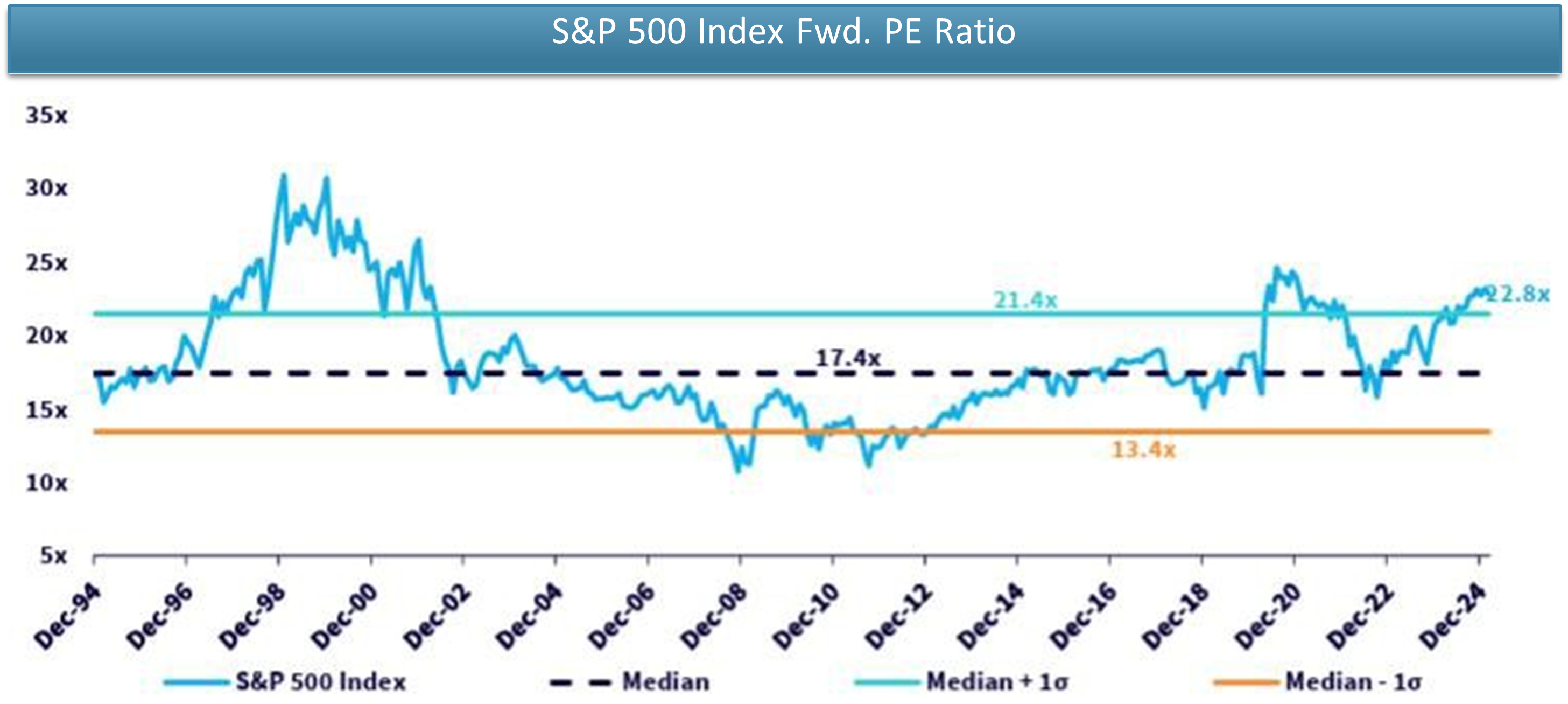

Why do we want to utilize international equities? (1) They have lower valuations and can potentially provide some protection (2) most of the major countries are cutting rates trying to stimulate their economies (3) many offer healthy dividend yields. Meanwhile, the S&P 500’s current forward P/E ratio of 22.8x is one standard deviation above the median, suggesting US index valuations are expensive.

Source: WisdomTree. Data as of February 6, 2025

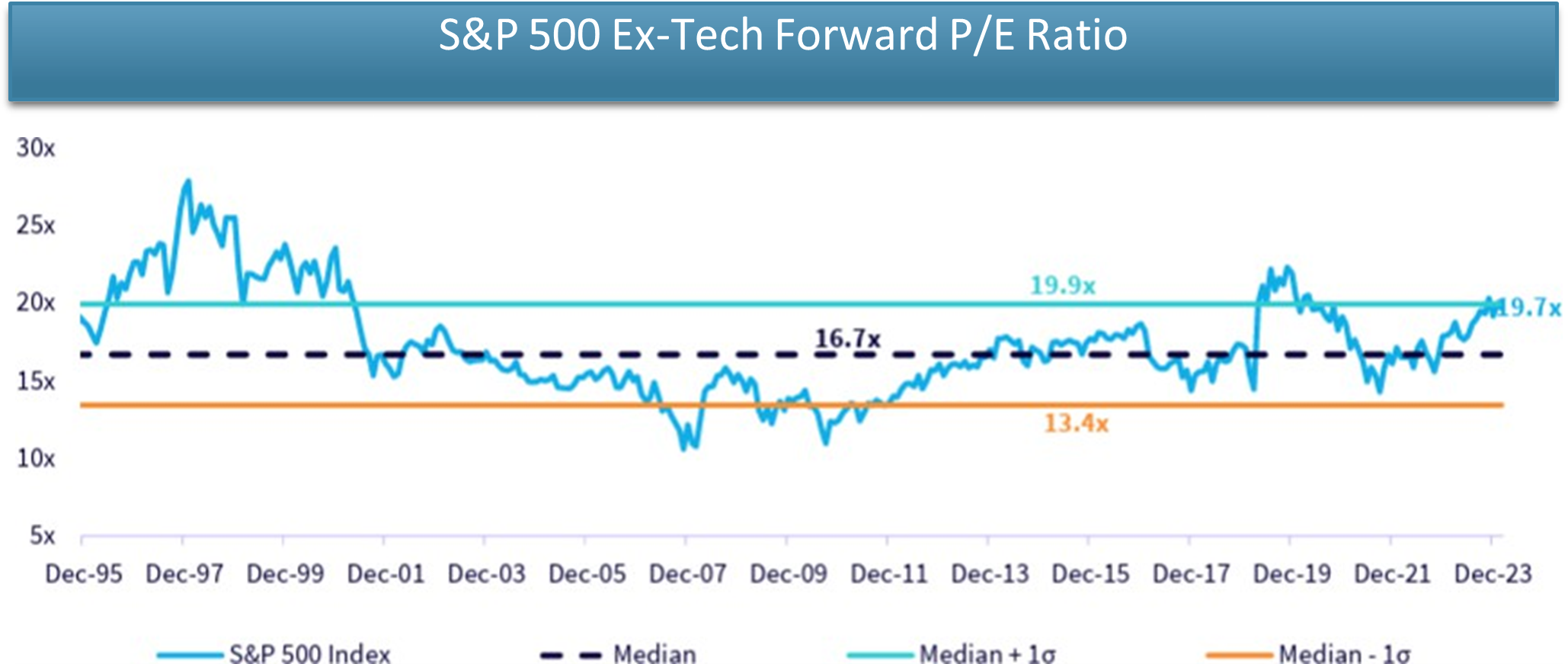

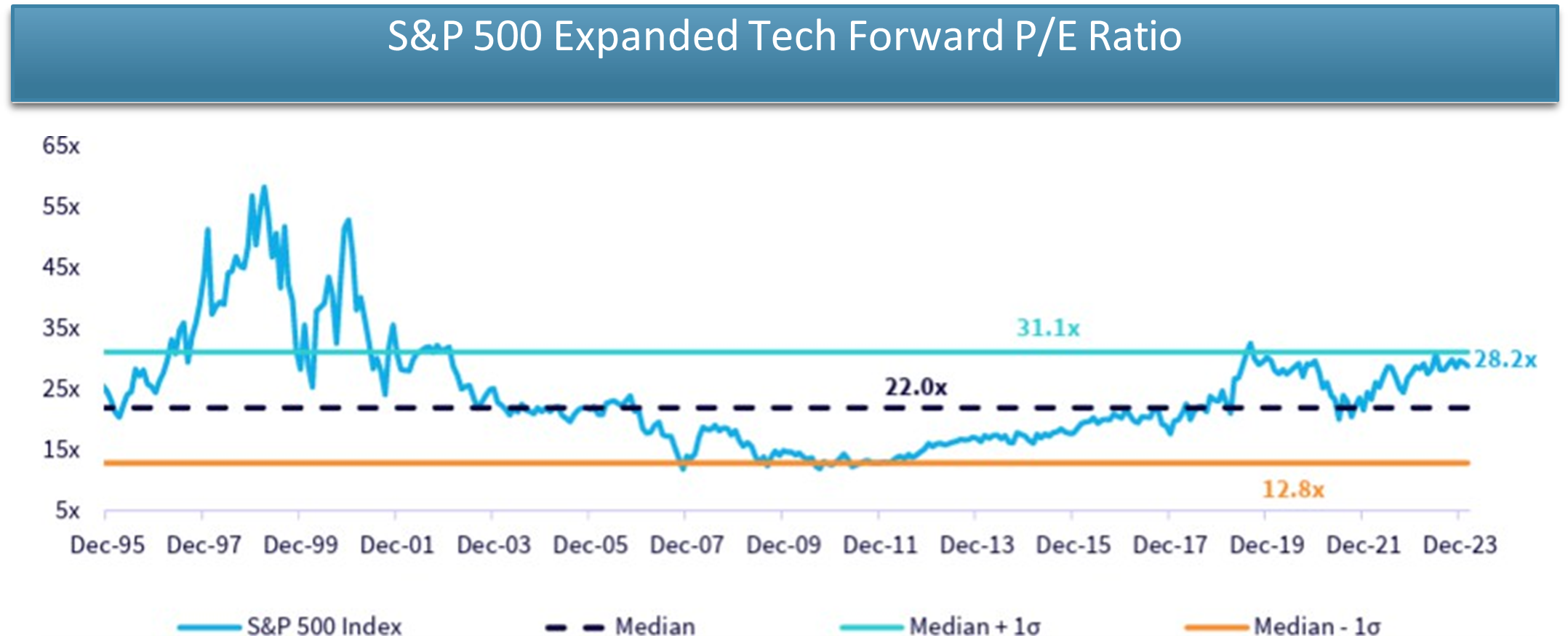

The S&P 500 Ex-Tech forward P/E is now at 19.7x while that of the S&P 500 Expanded Tech is around 28.2x.

Source: WisdomTree Daily Dashboard. Data as of February 10 , 2025

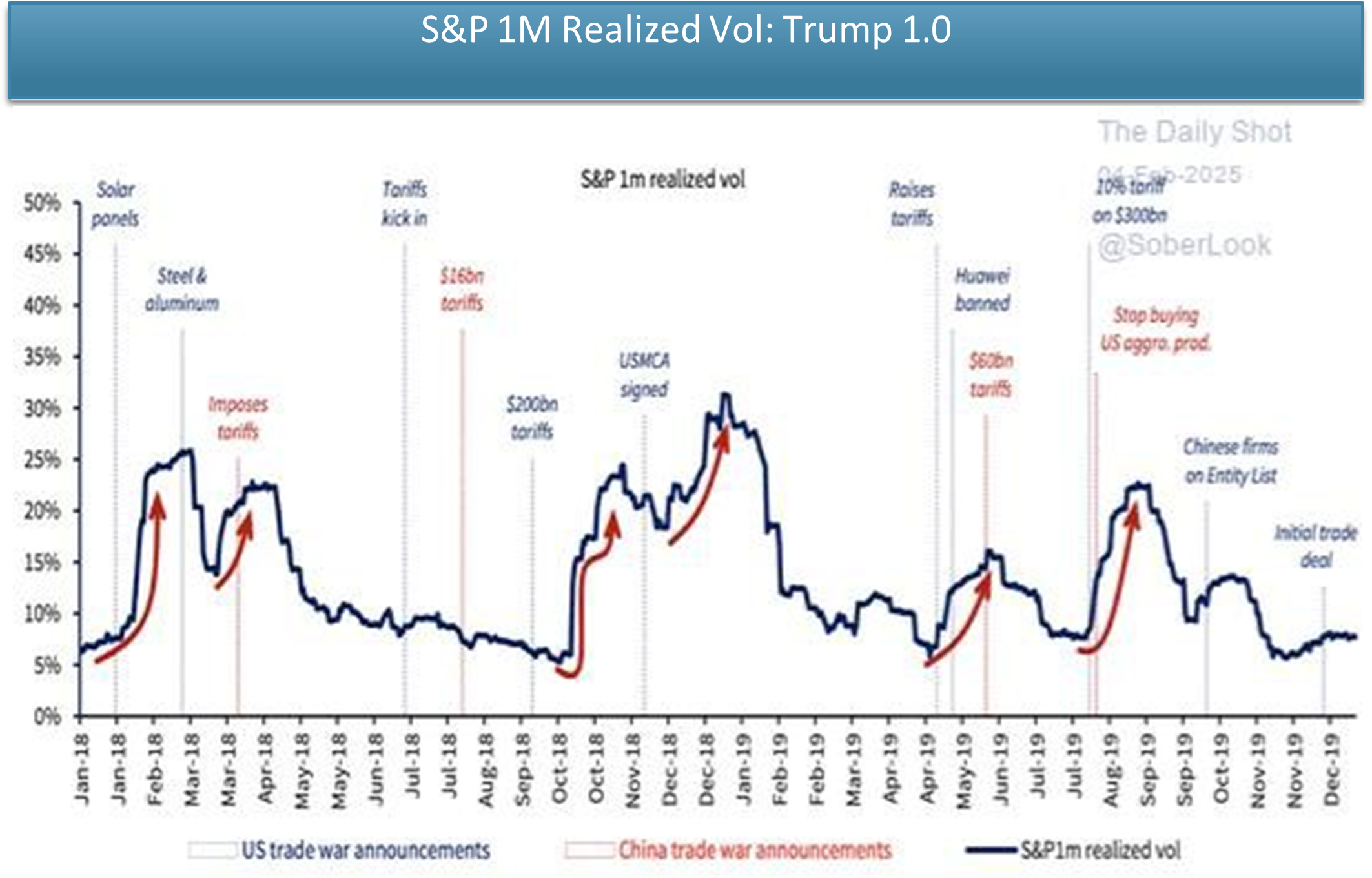

Get ready for volatility spikes in 2025. Equity volatility saw sharp moves regarding trade war announcements during Trump 1.0.

Source: Bloomberg, Barclays Derivatives Research, The Daily Shot.

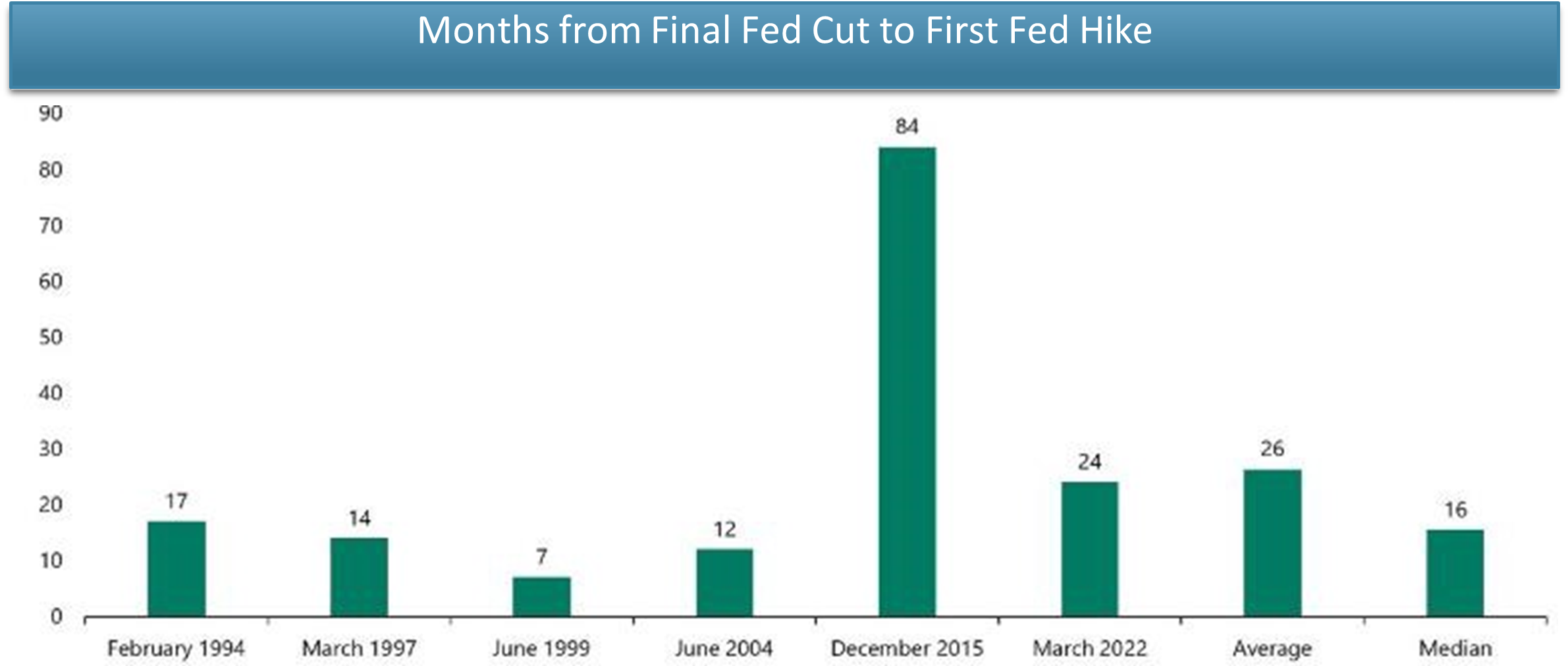

According to Apollo’s Chief Economist, the last Fed cut was in December, and the number of months from the final Fed cut to the first Fed hike has historically been as low as seven months.

Source: Federal Reserve, Haver Analytics, Apollo Chief Economist. Data as of February 7, 2025

The US large-cap equity risk premium is near 20-year lows, implying little premium for taking equity risk given high valuations and high rates.

Source: FactSet, Bloomberg, Morgan Stanley Research as of Jan. 31, 2025 Note: ERP based on forward earnings yield and 10-year Treasury Yield.

Leverage is running high. With increased asymmetric risks and rates that have more risk of increasing than decreasing (inflation running hotter, rate cuts pushed further down the road), we would caution investors who are running higher risk levels.

Source: Bloomberg, FactSet, Haver, Morgan Stanley Research; FINRA data As of Dec 31, 2024 (data lag). S&P data as of Jan 31, 2025

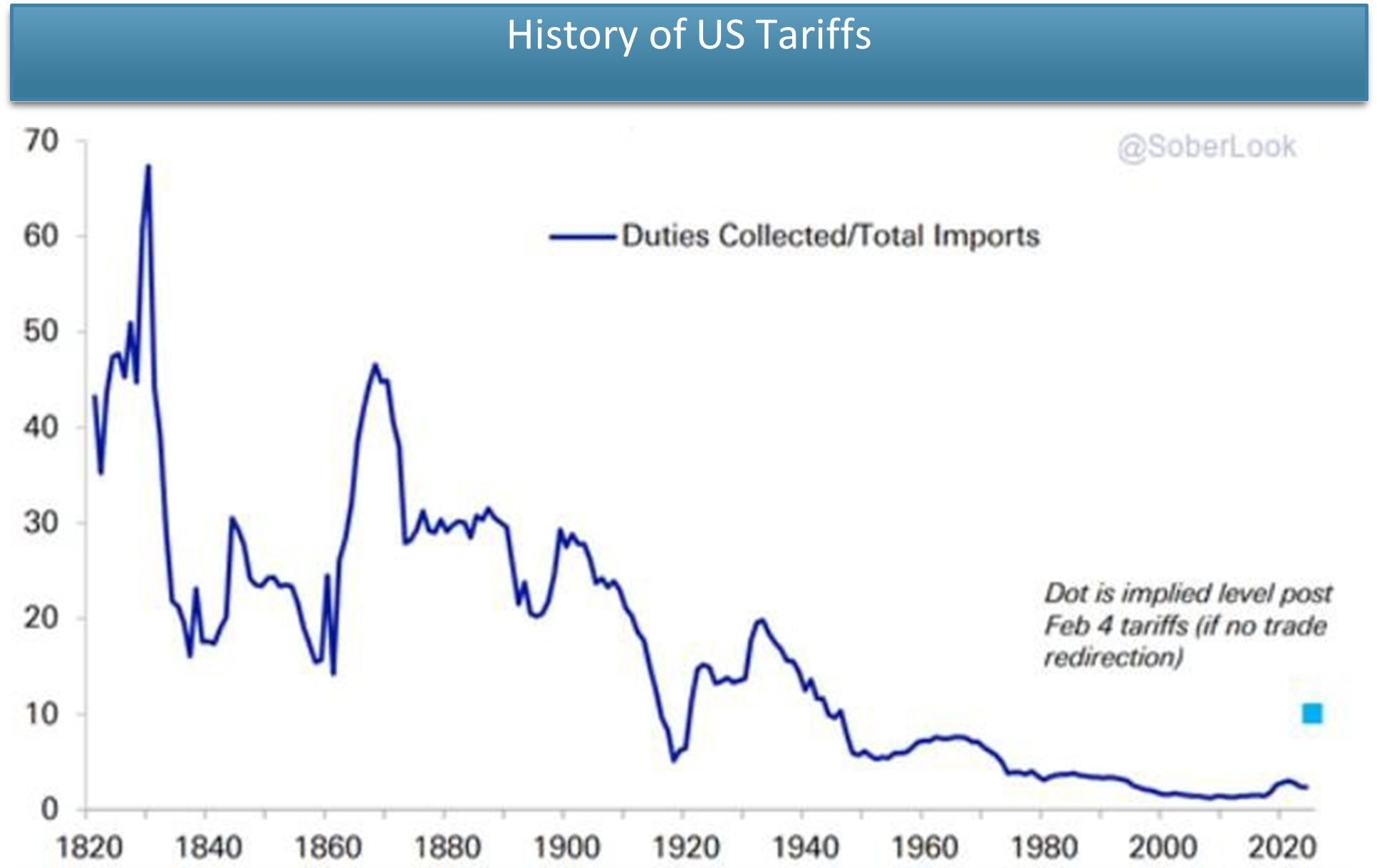

If the newly announced tariffs take effect, US tariff levels could revert to those last seen in the 1940s, marking a significant shift in trade policy.

Source: Historical Statistics of the United States, St. Louis Fed, Deutsche Bank.

Meanwhile, the US economy keeps chugging along. Jan ISM Manufacturing PMI is back in expansionary territory with new orders, production, and employment components all stronger than the previous reading.

Source: FactSet, ISM – Institute for Supply Management, Astoria Portfolio Advisors. Data as of February 3, 2025

Core CPI rose 0.4% month-over-month in Jan, with headline inflation up 0.5%, driven by shelter and used vehicle prices. Both readings came in hotter than expected, and the core annualized measure ticked up to 3.3%.

Source: FactSet, BLS – US Bureau of Labor Statistics, Astoria Portfolio Advisors. Data as of February 12, 2025

Appendix

2024 ETF Statistics

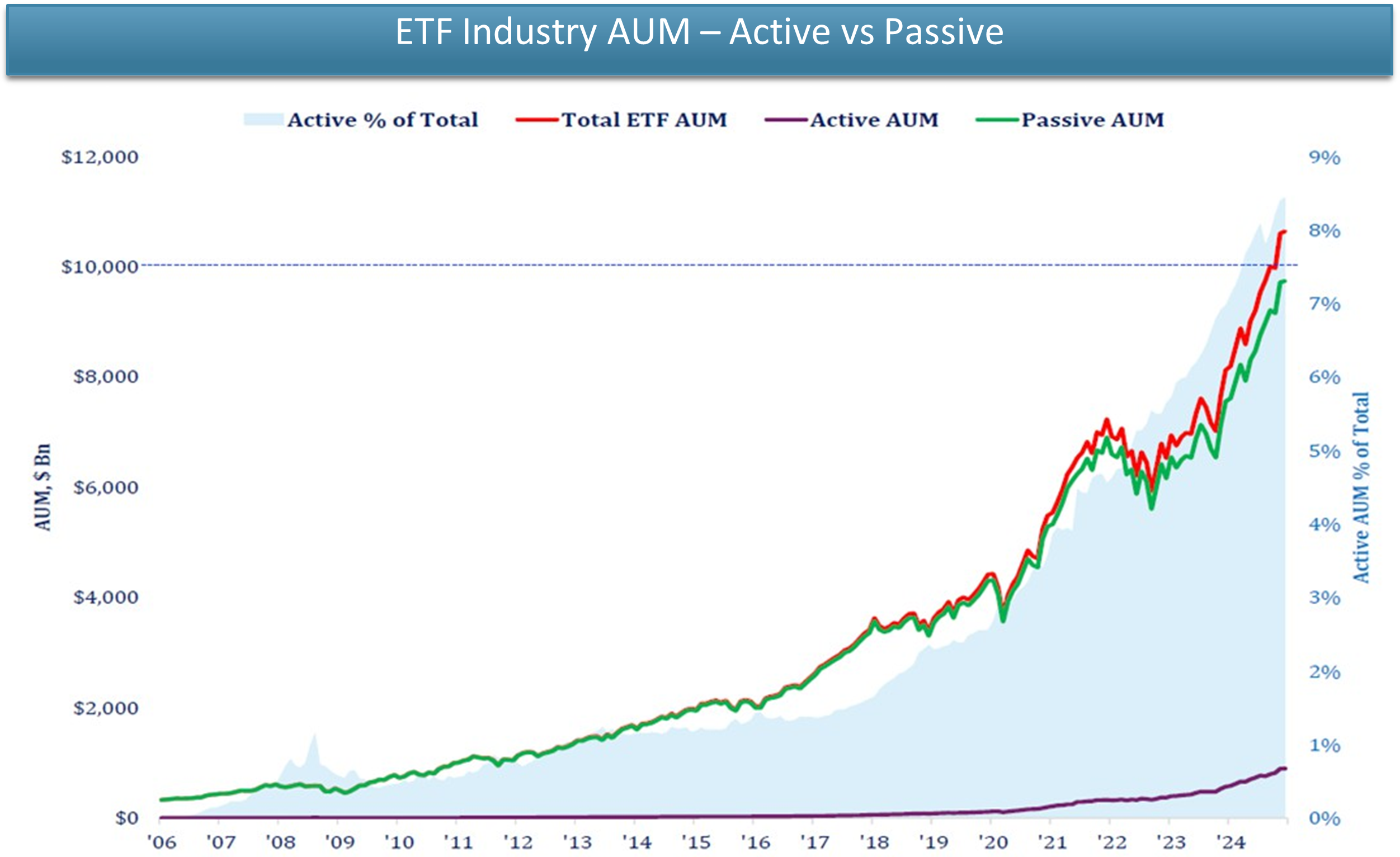

- ETF assets have surpassed $10 trillion in total Equites represent the lion share with over $8 trillion. Fixed Income continues to rapidly grow and has over $1.8 trillion.

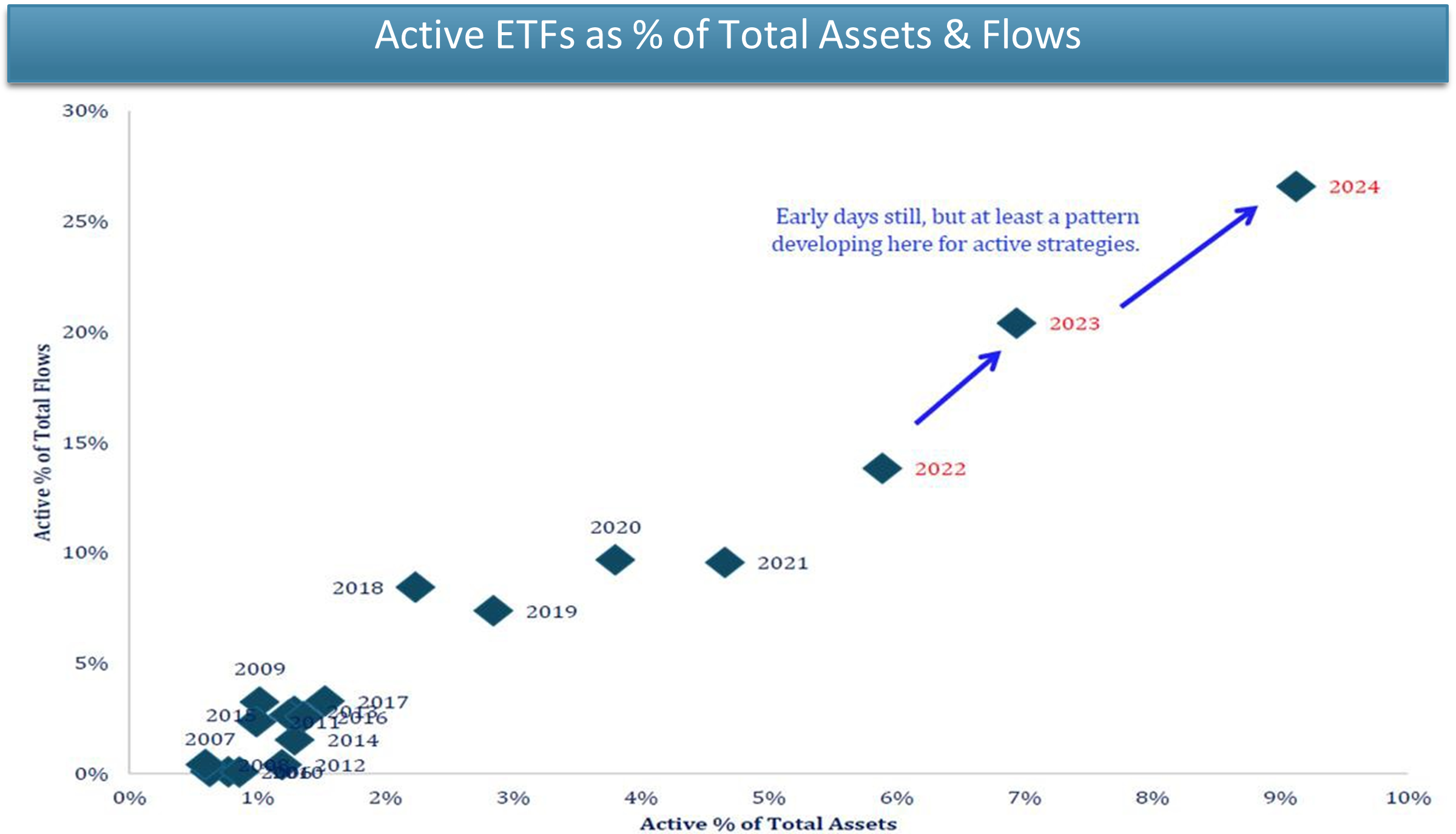

- Over 700 new ETFs launched in 2024, with over 500 of those under the active label. Astoria believes active ETFs will gain in popularity if the market rotation away from the Mag 7 gains momentum over a multi-year period.

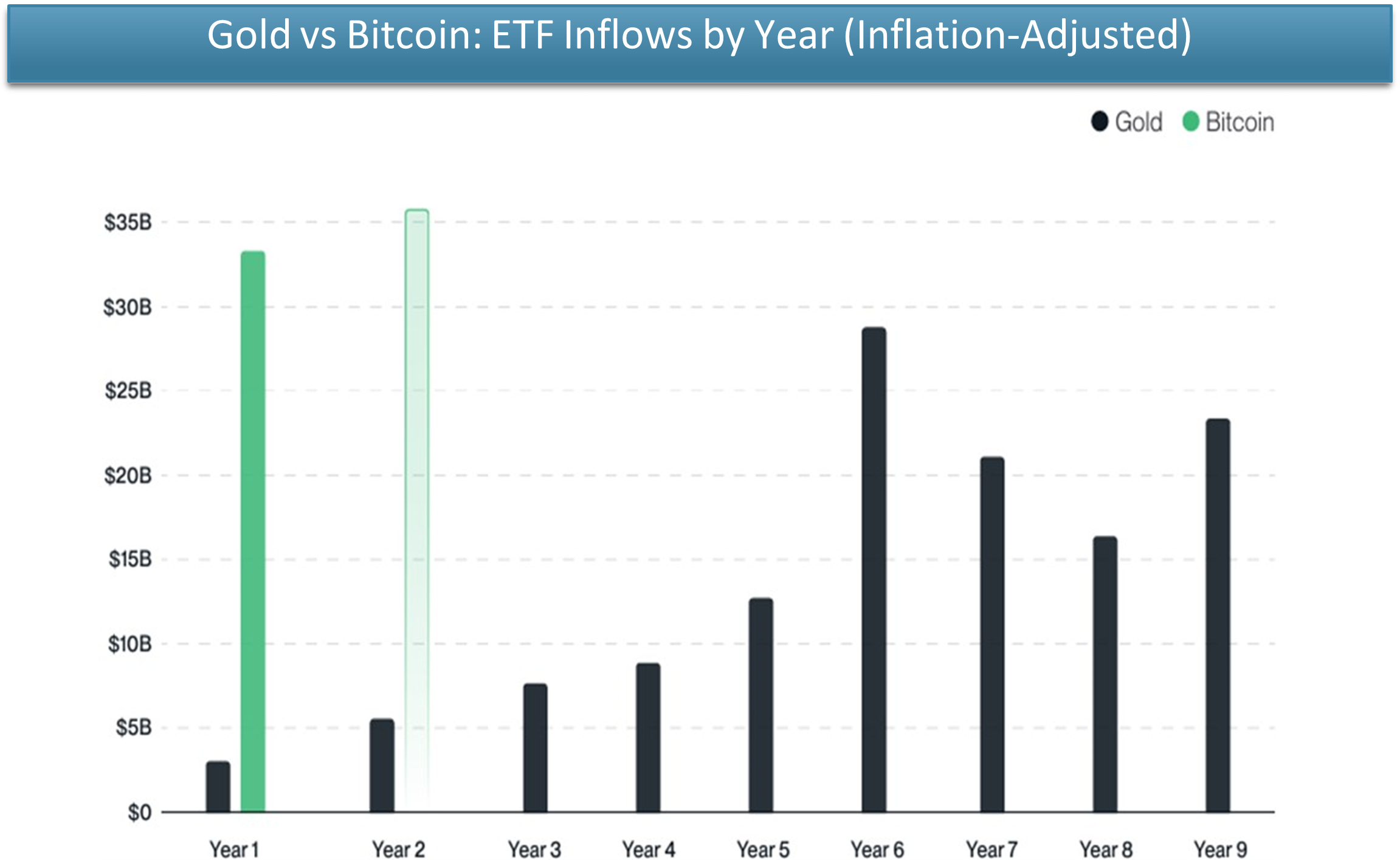

- Crypto ETFs exploded last Net flows were over $40 bln in year 1. With a pro crypto administration and large wirehouses who have yet to approve the product, its easy to see more inflows in Year 2 than Year 1.

- Watch single stock leverage ETF products. With ample liquidity sloshing around the system and a bull market that continues to run, levered stock ETFs are the one area to watch for irrational exuberance.

- According to Todd Sohn, derivatives-based strategies exploded in both product number and assets in There were almost 300 new funds that use the derivatives market to some capacity. Levered single stock funds, option writing, and structured outcomes are the key areas here,

- Active Fixed Income ETFs ‘quietly’ took in $100 bln of Astoria believes there are large systemic risk with the longer term debt cycle and one needs to be tactical in fixed income. Hence, we believe active fixed income could have a big year from an asset gathering standpoint.

ETFs have surpassed $10 trillion in assets. In recent years, the bulk of the assets have gone into Core US Equity Large-Caps. Has this fueled the Mag 7 fire?

Source: Bloomberg, Strategas. Data as of December 18, 2024

Over 700 new ETFs launched in 2024, with over 500 of those under the active label. If the market broadens out and Mag 7 relatively underperform, we’d expect more product proliferation in this space and the pace of inflows to continue.

Source: Strategas, ETF Action. Data as of December 18, 2024

With Trump’s pro-crypto administration, its hard to imagine inflows into bitcoin and other crypto ETFs won’t continue. Bitwise Asset Management expects more inflows into Bitcoin ETFs in Year 2 compared to Year 1.

Source: Bloomberg, Farside Investors, Bureau of Labor Statistics, and Bitwise. Data as of December 6, 2024

When liquidity is flowing and bull markets running, investors have flocked toward leverage. Single stock ETF volumes exploded in 2024 and are expected to increase, per Todd Sohn.

Source: Bloomberg, Strategas. Data as of January 6, 2025

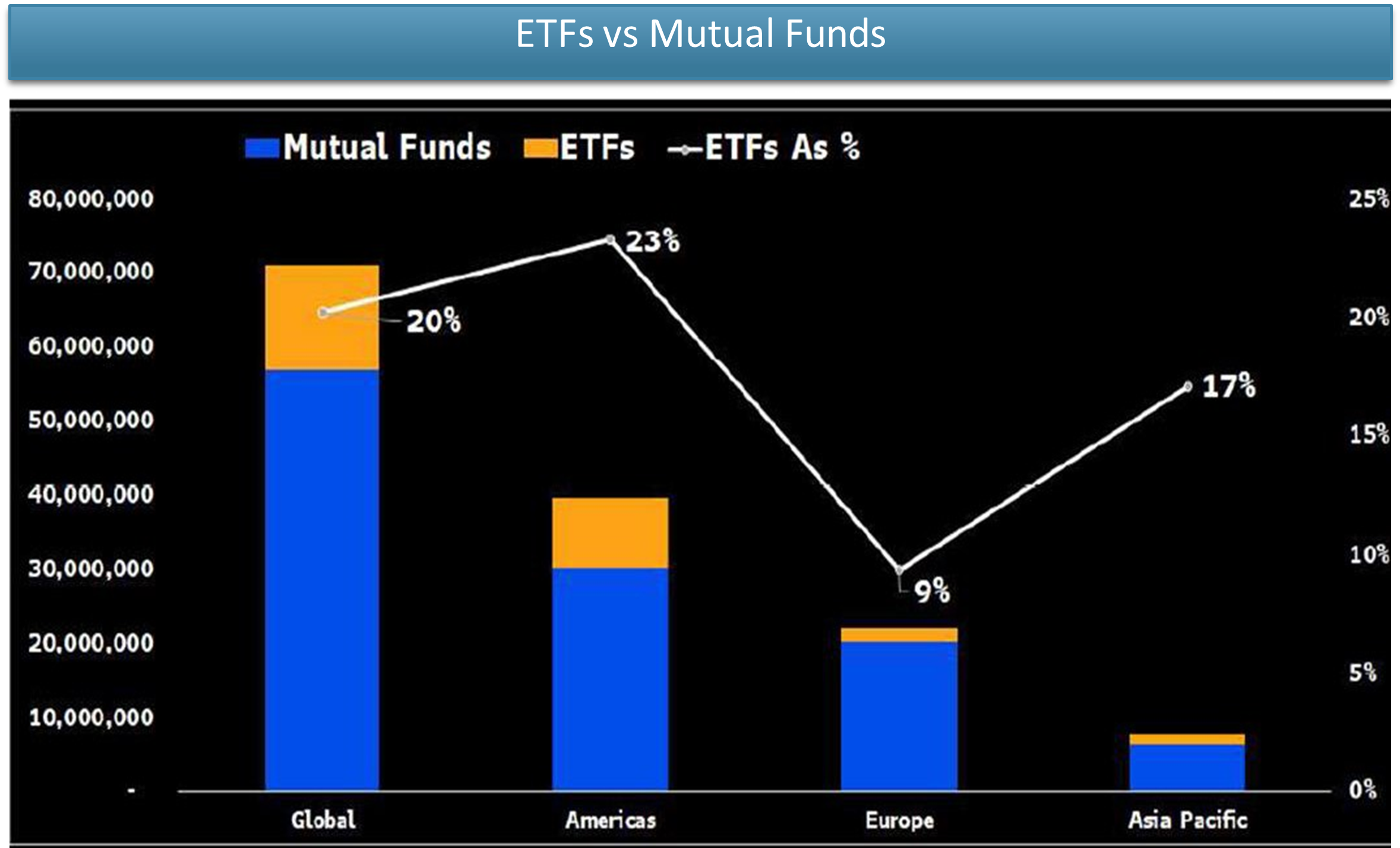

The ETF bull market has ways to go.

Source: Bloomberg Intelligence. Data as of January 14, 2025

For more news, information, and strategy, visit the ETF Strategist Channel.