By Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- The U.S. labor market remains robust, with the three-month moving average for payrolls surging to its highest level since March 2023, challenging expectations of near-term Federal Reserve (Fed) rate cuts.

- Persistent labor strength, inflation uncertainty and policy risks could delay or limit monetary easing in 2025.

- Given the likelihood of heightened bond market volatility, Treasury Floating Rate Notes (FRNs) offer a compelling fixed income solution, balancing income generation with reduced volatility.

The money and bond markets received their first look at the U.S. employment situation for 2025, and on the surface, the results were somewhat of a mixed bag. Given the importance the Fed has placed on both the inflation and labor market aspects of its dual mandate, it is prudent to “check under the hood” of the data to see if anything stands out. Well, after going through this exercise with the January jobs data, one discovers that the employment data may not have been a mixed bag after all, but rather another indication that the nation’s labor market remains solid, a key factor when trying to ascertain the outlook for any potential rate cuts.

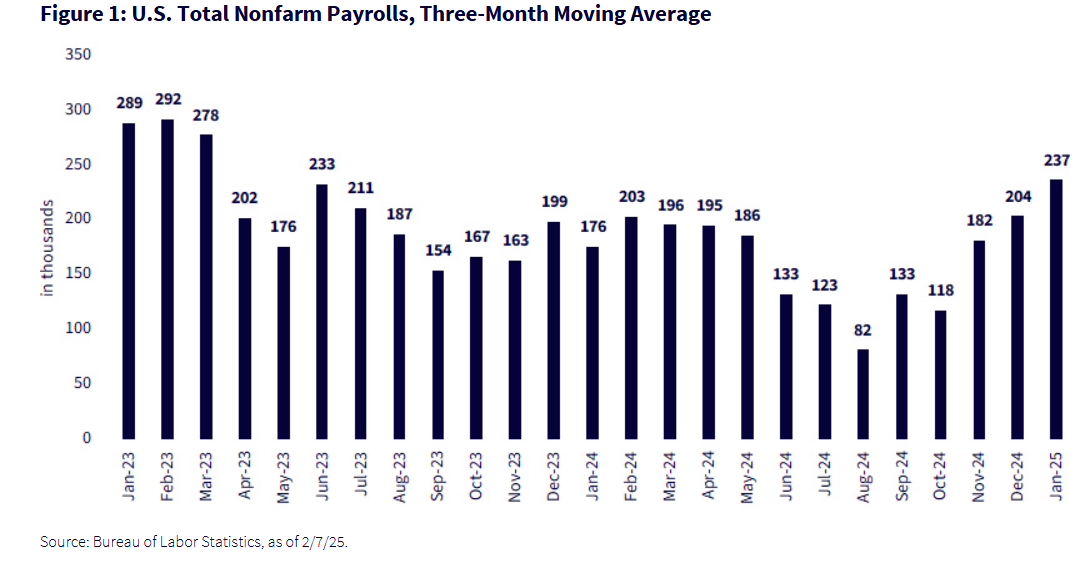

Figure 1 below represents the three-month moving average for U.S. total nonfarm payrolls. Utilizing this means of analysis helps not only to “smooth out” any outsized increases or decreases but, more importantly, can provide guidance for underlying trends.

Source: Bureau of Labor Statistics, as of 2/7/25.

Here are some highlights of what Powell & Co. are looking at now as compared to when they began cutting rates in an aggressive way back in mid-September.

- The three-month moving average increase for payrolls has been on a rather noteworthy ascending trend since November, with the current reading now at its highest level since March 2023

- When the Fed cut rates by 50 basis points (bps) in mid-September, the policy maker was operating under the premise that the labor markets may be cooling too much, as the three-month moving average had fallen to +82k in August

- The labor market narrative has done a “180” since that first rate cut, and now the current three-month number is at +237

- Post jobs and CPI, Fed rate cut expectations now point toward only one rate cut for 2025.If the labor market backdrop remains solid, inflation stays “bumpy” and policy/tariff-related uncertainty continues, the hurdle for future easing is raised accordingly

- The ascending trend in new job creation does not provide the underlying macro support for a continued rally in the Treasury 10-Year yield (it dropped nearly 40 bps from its January peak). In fact, heightened volatility and renewed pressure to the upside is the more likely scenario

Conclusion

The investment backdrop for fixed income highlights the value of Treasury Floating Rate Notes (FRNs) as the cornerstone of our active/passive barbell approach, where the emphasis is on income without the volatility.

This article originally appeared on WisdomTree’s website and is reprinted on VettaFi | ETF Trends with permission from the author. For more information, please visit WisdomTree.com.

For more news, information, and strategy, visit the Modern Alpha Channel.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.