By William Sokol, Director of Product Management

Investors new to collateralized loan obligations (CLOs) may choose to constrain themselves to AAAs, but we believe this is misguided. Although volatility may increase as you move down in quality, the yield and return potential offered by investment grade tranches outside of AAAs is far greater and doesn’t require taking significantly more credit risk.

Consider that:

- The aggregate CLO market, which represents the entire capital structure and is approximately 68% AAA CLOs, outperformed the AAA-only subset by 73 basis points (bps) per year over the past five years.

- Single A CLOs outperformed AAA CLOs by 142 bps per year over the past decade, with volatility that was lower than IG corporate bonds.

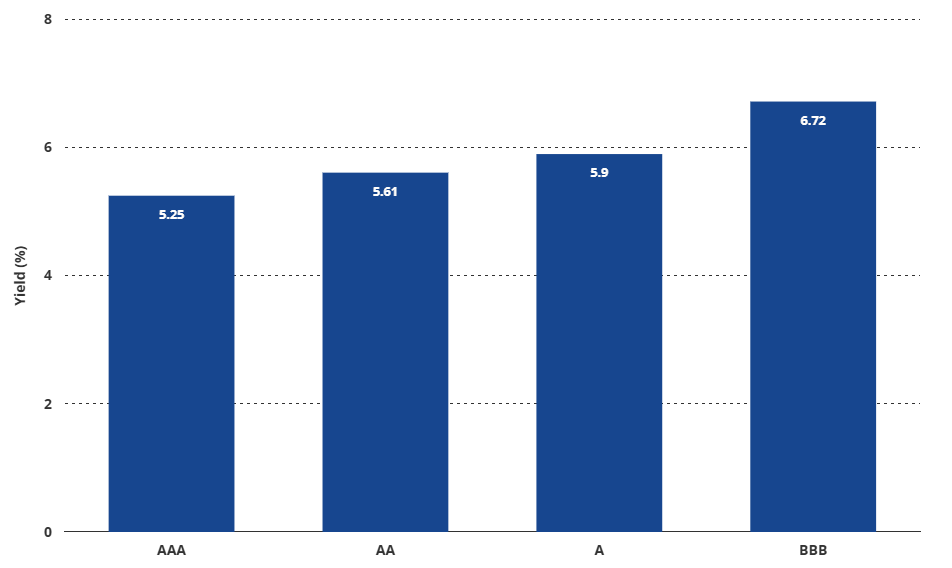

- BBB CLOs provide a yield pickup over AAA CLOs of 147bps, and pay a significantly higher coupon than high yield bonds, with much higher credit quality.

- Defaults have historically been extremely rare in investment grade CLOs, with only a 0.3% cumulative default rate, all which occurred prior to the GFC in CLOs with less robust structural protections than what is found today.*

Higher Yields Can be Found Within Investment Grade

Source: ICE Data Indices, J.P. Morgan. CLOs represented by J.P. Morgan CLO Index or the ratings subset of the J.P. Morgan CLO Index. Index performance is not illustrative of fund performance. It is not possible to invest directly in an index.

We note that the CLO yields in the chart already assume an expected decline in short-term rates, as market convention in the asset class is to use the current forward interest rate curve. Further, CLO yields assume a certain loss rate in the calculation, so default assumptions are already reflected. This may provide additional comfort to those who are wary of investing outside of AAA tranches. Corporate bond yields do not make similar adjustments for potential defaults.

The ability to move into higher yielding investment grade tranches outside of AAA, which have yields that are driven more by credit spreads versus short-term risk-free rates, may allow investors to continue earning high absolute levels of income even in an environment of declining interest rates. For example, in a risk off environment, even if the Fed cut rates aggressively it is likely that overall yields could increase due to spread widening, particularly in single A and BBB rated tranches, dispelling the notion that CLOs are only attractive in rising rate environments. In a more benign environment such as we are in currently, moving further down the CLO capital stack can provide the opportunity for higher carry compared to AAA CLOs, while remaining well insulated from underlying loan defaults and volatility.

Further, the ability to invest broadly within investment grade and move within the full CLO capital structure can provide attractive total return opportunities as the rate and credit environments shift compared to an AAA only portfolio, while avoiding the significant volatility and drawdown potential of a strategy focused on CLOs rated BBB and below. Highly rated CLOs may provide insulation against a risk-off environment, but the ability to capture higher value in mezzanine tranches after a sell-off can allow significant upside potential as prices recover.

Navigating the CLO capital stack is where the value of active tranche management shines. An active approach provides both alpha potential and additional risk protections: through bottom-up analysis of underlying exposures, identifying/avoiding mispriced deals (and in some cases, avoiding lower rated tranches altogether) and active liquidity management. The ability to understand the various drivers of CLO risk is key in assessing the relative value of a tranche. PineBridge has decades of expertise in the CLO market and takes an active, high-conviction approach to investing in CLO tranches.

The VanEck CLO ETF (CLOI) invests primarily in investment grade tranches of CLOs. CLOI is actively managed and based on a strategy that PineBridge has managed for years for its institutional clients, and is now available to all investors with the transparency, liquidity and cost benefits of an ETF.

To receive more Income Investing insights, sign up in our subscription center.

Originally published 05 February 2025.

For more news, information, and analysis, visit the Beyond Basic Beta Channel.