By Rod Smith, Chairman of the Board

Let the politics begin.

President Joe Biden has laid out an ambitious tax and spending plan incorporating most of the ideas from his 2020 campaign. It focuses on two main areas: an industrial policy geared to building a ‘green’ infrastructure and a clear change in social priorities. We stress ‘laid out’ because we believe this represents a ‘wish list’ of the things this administration would like to do. What actually gets passed by Congress will not be known for months. The Biden administration’s plan is bold, with echoes of President Lyndon Johnson’s ‘Great Society’ changes from 1964-1968. The question for investors is just how much of Biden’s proposal has the political support to pass, and how might it impact markets.

The Context

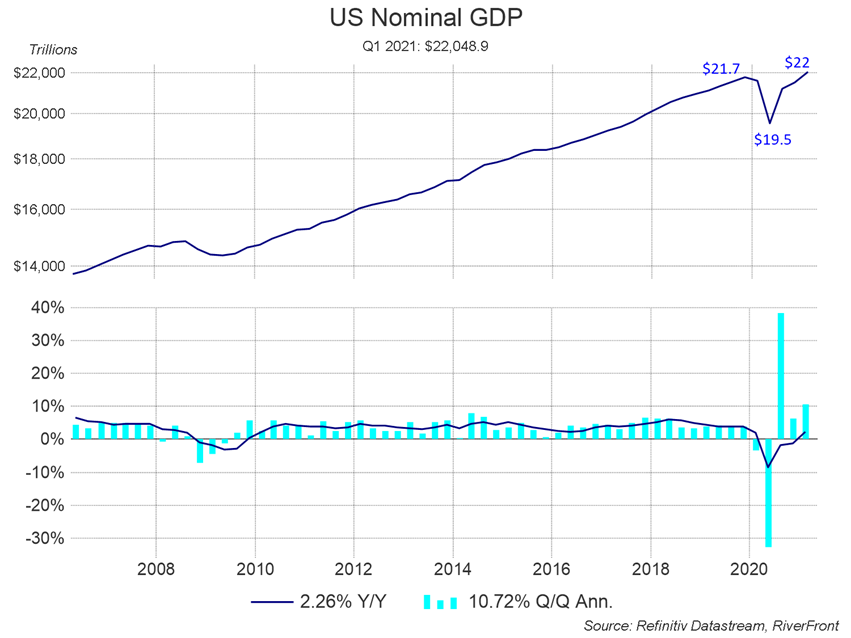

To put $4.7 trillion in context, the US is currently a $22 trillion economy. The pandemic reduced US GDP (Gross domestic product) by about $2.2 trillion (10% of GDP) and as you can see from the chart, GDP has now surpassed its pre-COVID-19 high. Congress approved $4.5 trillion (just over 20% of GDP) in COVID-19 relief in three separate bills, two under President Trump and one under President Biden. While the new $4.7 trillion proposals are similar in size, the proposed spending and tax revenue are spread over roughly 10 years (see appendix). At that size and timeframe, their economic impact– even if fully enacted – will be considerably less than the COVID-19 relief packages which were designed to be spent immediately and had no tax offsets. That said, from the tax perspective, these proposed increases would be roughly 1.3% of GDP. This is considerably larger than those enacted under Presidents Obama, Clinton, G. H. W. Bush, and Reagan, which averaged around 0.4% of GDP. You must go back to President Johnson’s 1968 tax hikes to find a bigger percent of GDP at 1.7%. (Data courtesy of Strategas research).

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Biden’s Gamble

With a slim majority in the House of Representatives and a divided Senate, Biden’s mandate is much smaller than that enjoyed by the Johnson administration and so the politics of this will be critical. President Biden has chosen to throw everything into his two plans, without clearly identified prioritization. The plan will be paid for with a significant overhaul to corporate taxes as well as a multifaceted increase in taxes for those earning over $400,000. The administration is taking a gamble by pushing for such a wide-ranging set of proposals all at once. This strategy could work in its favor if moderate Democrats decide they do not want to be seen voting against the party’s broad agenda. Equally, if it is perceived as too ambitious by these moderate Democrats, and subsequently cut into pieces, a lot less may get done. There is also the risk that there will be a political backlash which costs the Democrats control of Congress in 2022. Those Democrats with slim majorities in moderate constituencies have tough choices to make.

What seems clear, based on the reaction so far, is that the plan will receive little or no Republican support. That means whatever is finally agreed on is likely to be passed by a process called ‘reconciliation’ whereby any planned spending increases must be budget neutral in ten years. The ability to agree on tax hikes (more controversial than spending) will be one factor limiting the plan’s overall size. We think that over the next six months or so we will see a spirited internal debate on spending priorities, and then another on how much of the proposed tax increases the Democrats are willing to pursue. A reasonable guess is that the final package will be closer to a fiscally neutral $2-3 trillion, spread over 10 years.

Our View of the Implications

We believe the combination of aggressive COVID-19 fiscal relief and a highly accommodative Federal Reserve will deliver very strong economic growth in 2021 and 2022. The Biden proposals signal a shift in priorities. For stocks, we think higher taxes will reduce corporate earnings by 5-10% depending on the size of the bill. Set against this will be the pace of recovery, which we think will absorb some of the effect of tax increases. Within the stock market, we think the Technology and Healthcare sectors have the biggest exposure to increased taxes on their overseas earnings, but there will also be benefits for companies who stand to gain from the proposed government spending, and from higher wages for low-income workers. Due to the pace of the recovery, we expect further increases in bond yields and a gradual shifting in Fed policy towards being less accommodative. The Biden proposals will likely increase spending faster than revenue in the early years and because they follow the COVID-19 relief spending, will put upward pressure on prices especially where the pandemic has created supply shortages.

Conclusion

There is so much we cannot know with any certainty about how the next six months will play out…today we can only start to analyze the possibilities. Financial markets are absorbing all this and thus far, both the stock and bond markets seem to be unfazed. Indeed, the S&P 500 hit a new high on Thursday (4/29/21), apparently more focused on higher-than-expected Q1 earnings. More important than seeking to predict such a politically complicated outcome, we believe our tactical and risk management processes will help us navigate a summer/fall period that is likely to create lots of headline news.

Appendix:

The Numbers in More Detail:

Spending: Broadly, President Biden is seeking to spend roughly $4.7 trillion over 10 years. This is divided into two similarly sized bills: The American Jobs Plan and the American Families plan. The American Jobs Plan is focused on infrastructure and industry, and The American Families Plan focuses on social projects. Ultimately these may be combined into one omnibus bill.

Revenue: The spending is to be funded by increased taxes on companies and individuals respectively to pay for the two plans as follows:

- Raise the corporate tax rate, and tax income on overseas earnings plus ‘book income’, defined as income reported to shareholders which is generally higher than the ‘taxable income’ that is reported to the IRS’.

- Raise a variety of taxes strongly geared to those earning more than $400,000.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1631751