{kind=link}

The topic of higher interest rates has been on investors’ minds for seemingly years now. Every time interest rates climb even a little, more and more people seem to be hopping on the “this is finally the end of the 30-year bond bull market” bandwagon. And this is justifiably so given catalysts such as the Federal Reserve finally raising interest rates.

That being said, investors have been fooled before into thinking a higher interest rate regime was finally here. So is this time any different?

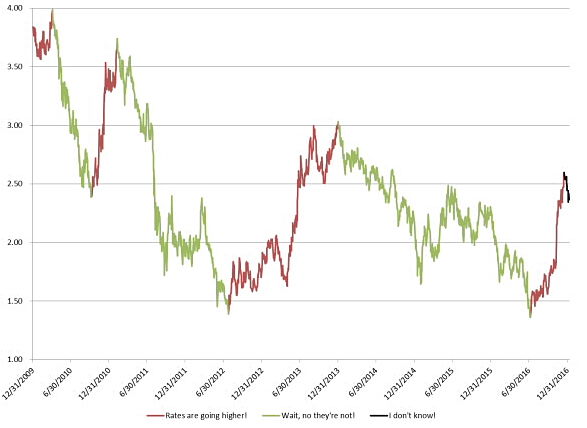

Here is a chart of the 10-year treasury since the end of 2009.

{kind=link}

Excluding the first small period heading out of 2009, there have been three times this decade so far where rates have climbed significantly. The end of 2010 saw a quick 1% move over four months, but that was erased rather quickly in the summer of 2011.

Then over the summer of 2012 and all of 2013, rates again climbed, this time a little more steadily and at higher absolute levels, doubling from 1.5% to 3% over nearly 18 months. During this time, there was a much more distinct cry in the market of higher rates and the end of the bond bull market. There was much discussion regarding the need to shorten duration in portfolios. This was also the time where ETF innovation saw a plethora of interest rate hedged (or even negative interest rate) products come to market. Market participants were seemingly prepped for what they thought would happen next.

And then…..

Right from the start of 2014, rates started declining. And declining rather steadily, recouping the entire 2012-2013 move and sliding back to 1.5%. (There was some trepidation in the early months of 2015, but this move higher was smaller in size and length.)

As we entered the latter half of 2016, rates once again began moving higher. Then came the Trump-sized catalyst (or wrench depending on who you ask) which caused rates to scream higher. Following the election, again there was much discussion on higher rates and the end of the bond bull market.

And then…..

Of course it has been a very short measurement period, but since mid-December rates have once again moved rather steadily lower, seeing the 10-year move from 2.60% back down to 2.33% at the time this was written. Now while a 27bp move hardly represents a shift in regime, it does at a minimum have to cause some concern whether or not the higher rate trend we have seen in the latter half of 2016 is on schedule to continue. As just mentioned, there is a Trump-sized catalyst waiting to happen, and with inauguration day looming, uncertainty is high.

Additionally, the pattern of which rates are moving higher is similar to that of the 2012-2013 move (steadier climb, then a spike, then a continued move higher). If rates were to happen to follow that same trend, this recent dip could be a temporary correction and we may see another short-lived move higher. But again, if rates were to follow the same pattern, the V-shape near the end (of which we could be in the first leg of) was followed by a sustained move lower.

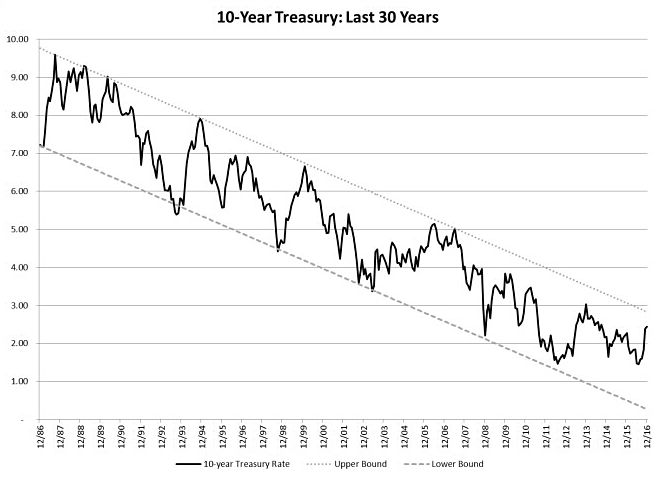

So while we are in a bit of a wait-and-see pattern now it would appear, a longer-term view of interest rates can provide an additional viewpoint. Here is a chart of 10-year treasury rates over the past 30 years through the end of December 2016 (where rates were at 2.45%)

{kind=link}

Right now rates are still decently within the long-term trend channel. So while there is room to move higher, it would seem that a break of the top side of this channel would provide a stronger case that we could truly be seeing the end of the bond bull market.

Right now, the top of that channel sits right about 2.80%, which sits right in the middle of where two well-known pundits have set their line-in-the-sand of where rates need to exceed to be in a new, higher environment (2.60% and 3.00%, respectively).

So where do we go from here? I am not here to predict where rates are going, as predictions more often than not prove to be worthless. Rather a continued monitoring of the market and a reactionary rather than predictive positioning may be warranted.

Clayton Fresk is a Portfolio Manager at Stadion Money Management, a participant in the ETF Strategist Channel.

Disclosure Information

Past performance is no guarantee of future results. Investments are subject to risk and any investment strategy may lose money. The investment strategies presented are not appropriate for every investor and financial advisors should review the terms and conditions and risks involved. Some information contained herein was prepared by or obtained from sources that Stadion believes to be reliable. There is no assurance that any of the target prices or other forward-looking statements mentioned will be attained. Any market prices are only indications of market values and are subject to change. Any references to specific securities or market indexes are for informational purposes only. They are not intended as specific investment advice and should not be relied on for making investment decisions. One cannot invest directly in indexes, which are unmanaged and do not incur fees or charges. Founded in 1993, Stadion Money Management is a privately owned money management firm based near Athens, Georgia. Via its unique approach and suite of nontraditional strategies with a defensive bias, Stadion seeks to help investors—through advisors or retirement plans—protect and grow their “serious money.” Contact Stadion at 800-222-7636 or www.stadionmoney.com. SMM-012017-082