By Sean Clark, Clark Capital Chief Investment Officer

Before we get into our 2017 Outlook, let’s look at last year and some of our previous annual predictions (see full Outlook Forecast chart further below).

Our forecast for 2016 called for the S&P 500 to end the year at 2200, which would have been a 7% gain for the year. We expected a positive year for the market, and we were more bullish than most given the normal presidential election year trends, the favorable economic backdrop, and the fact that good years normally follow flat years.

As it turned out, our expectation for the market was almost right on target as the S&P 500 closed the year at 2238, very close to our 2200 target. In addition to being fairly accurate with the year end target, we also expected a sharp post-election rally, which was definitely a contrarian view. We put a lot of time and effort in preparing our annual Outlooks.

As you can see from the table further down, we have been fairly accurate in our forecasts since we started making annual predictions. While there were years that our expectations were not realized, we were right on in 2009, 2012, and 2016 and only missed slightly in 2010.

Outlook 2017

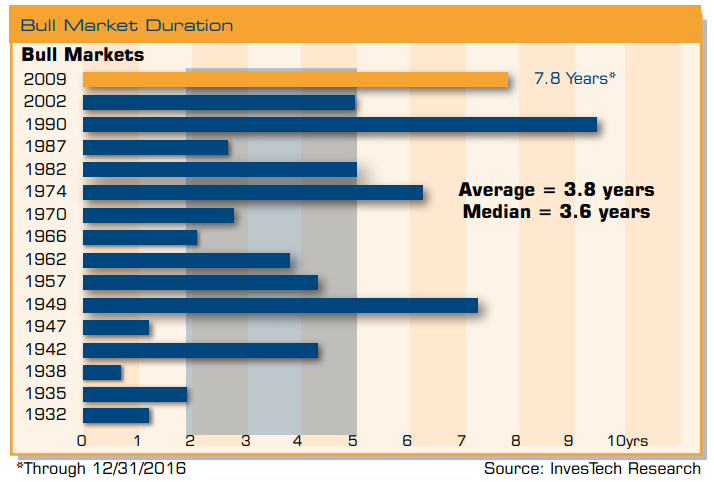

Our long-term view is that we are in a secular bull market in stocks. We enter the New Year on solid economic footing and within a long-term secular bull market. We are now almost eight years into the secular bull and seven and a half years into the economic expansion. Nearly every economic indicator we look at suggests continued growth in the U.S. For example, the Conference Board’s Index of Leading Economic Indicators is hitting new highs, consumers are optimistic with Consumer Confidence at a new recovery high, and jobless claims are hitting their lowest levels since the early 1970s.

These all suggest that the economy is set to accelerate in 2017. The positive economic environment is supportive for risk assets. With the economy on solid ground and the earnings recession behind us, we see stocks continuing to advance and expect high single-digit returns for the U.S. stock market in 2017, with a 2400 yearend target for the S&P 500.

The market gains could be frontloaded on expectations of policy initiatives that may not be fully realized, which could result in some volatility in the second half of the year. We continue to favor credit over duration, especially in an environment of rising yields. Historically high yield bonds have done very well in years that interest rates rise given their leverage to the economy. There are risks.

The first year of a new president’s term has historically been weak, and more so when it’s the first year of a Republican in office. In addition, valuations remain stretched, interest rates are set to continue moving higher, and the Federal Reserve seems to be behind the curve with upside risks to inflation.

The latest comments out of the Federal Reserve are somewhat at odds between letting the economy “run hot” and setting expectations of three additional rate hikes in 2017. However, if recent history is any guide, the Fed will fall short of hiking rates as often as they suggest, given that they only raised rates once in each of the past two years.

Economy

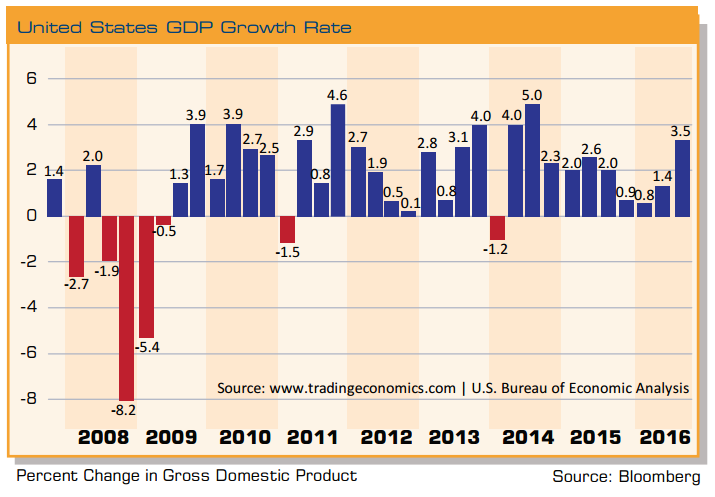

The U.S. economy has expanded for seven and a half years now but only at a 2.1% annualized pace, which is the slowest post-WWII recovery on record. However, over the past several quarters it has been strengthening, and the third quarter 3.5% growth rate was the strongest in two years. It appears the economy is building momentum, and we expect that trend to continue as the new administration’s pro-growth and market-friendly policies should drive GDP higher than the trajectory it has been on.

The consensus of major economists puts economic growth at 2.2%, which is about equal to the growth rate since the end of the recession. That seems way too conservative considering that data has been surprising to the upside recently with GDP tracking above 2.5% over the past six months. Thus, we see more room for upward revisions to the consensus.

{kind=link}

We expect the U.S. economy to grow by 3.0% in 2017 as pro-growth policies stimulate spending, tax reform adds to disposable income, and regulatory reform adds to productivity. Consumer confidence has surged in recent months, the labor market is tightening, wage pressures are rising, and economic indicators we look at are on solid footing.

Global growth should outpace U.S. growth and we expect stronger growth across both the developed and emerging economies than we saw in 2016. We expect 3.5% global growth as monetary conditions remain accommodative in the aggregate, and fiscal stimulus should help boost growth. There are plenty of risks to these outlooks, including trade protectionism, a stronger U.S. dollar, higher interest rates, and geopolitical risks in Europe and in the Middle East.

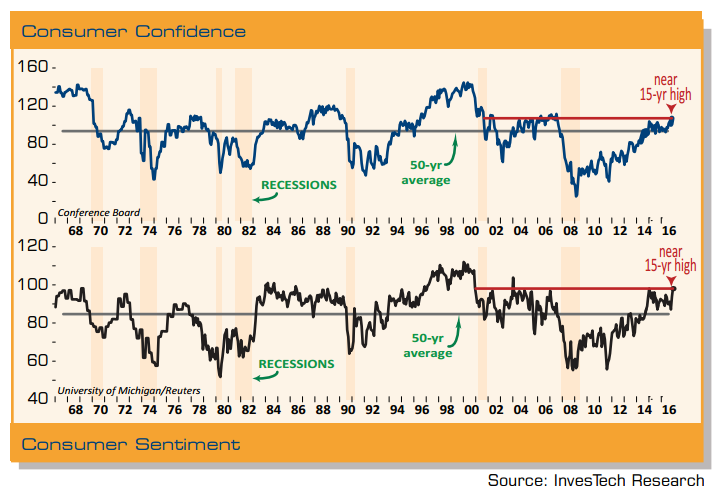

In the U.S., consumers are the most upbeat they have been in 15 years. Consumer Confidence as measured by the Conference Board (top graph) and Consumer Sentiment as measured by the University of Michigan/Reuters (second graph) are both currently near their highest levels since the early 2000s. Where confidence goes consumer spending usually follows – which accounts for roughly two-thirds of U.S. economic activity. Consequently, an upbeat consumer suggests that we have a stable and accelerating economy as we move into the New Year.

{kind=link}

The economy is now seven and a half years into its economic expansion. Only three economic expansions in the post-WWII period have lasted longer than the current one. Going all the way back to 1900, the current boom ranks as the fourth longest.

From 1961 through 1969, the economy saw uninterrupted growth for nearly nine years. Then from 1982 through 1990, the economy went just over seven and a half years without a recession. If we don’t see a recession before March, this cycle will surpass that one. The longest boom of them all, though, was from 1991 into 2001 when the expansion lasted a full decade.

{kind=link}

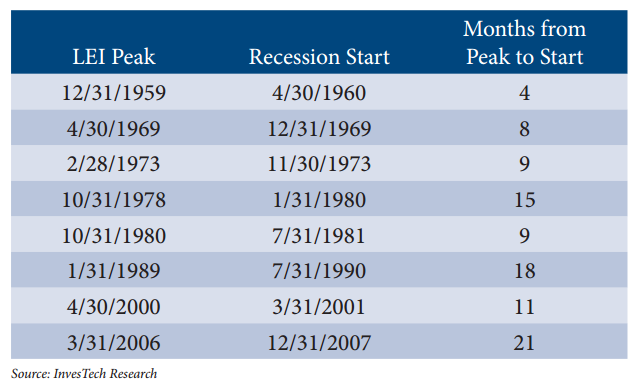

We have a high degree of confidence that the U.S. economy has further growth potential. The Conference Board’s Index of Leading Economic Indicators (LEI) has risen to its highest level since early 2006 and is almost out to a new all-time high.

In fact, there have been only five other months in the entire history of this index that have been higher. We put a lot of emphasis on leading indicators because over the past 50 plus years, early weakness in the LEI has preceded every recession in the U.S.

The typical lead time between the peak in the LEI and the start of a recession has ranged between four and 21 months. Since 1960, the average lead time has exceeded 11 months. We are not seeing any weakness currently in the leading indicators index, and if history is any guide, which it usually is, the U.S. economy should continue its expansion through 2017.

In addition to leading indicators, the labor market is also suggesting continued economic expansion. Initial jobless claims are hitting new lows and the four-week moving average of initial jobless claims is not only hitting post-recession lows but also lows not seen since the 1970s. This is important because our research shows that an upturn in jobless claims typically occurs six to 12 months prior to a recession. This is not even on the horizon currently.

The strength of the labor market can also be seen in rising compensation across the board. Wage and price increases may be rising faster than anticipated, and the Fed could easily fall behind in their efforts to keep inflation in check. Average hourly earnings are up 2.4% year over year and the Atlanta Fed’s Wage Tracker, which tracks hourly wages for workers that have been employed full-time for at least a year, shows wages up 3.9% over the past 12 months. In addition, the focus on job creation by President Trump is likely to intensify the wage inflation pressures.

Presidential Election Cycles Now that the election is behind us and a new administration is about to take office, many are asking how the market normally performs under different parties. Does the market do better under a Republican or Democratic president? Well, it depends on the time frame being looked at. The total performance from 1928 until today shows returns being over twice as good under Democratic presidents than under Republican presidents. However, if one is selective in choosing the starting and ending points, one could identify periods where the market does slightly better under Republicans.

For example, the market did great under Presidents Reagan, and Bush 41, and Clinton. Then stumbled when it was in a secular bear market under Bush 43 and then was great again under Obama, who came into office at the time a new secular bull was beginning. So our conclusion is that it likely depends on the environment. Last year marked the twenty-third presidential election since 1928.

Prior to the current political outcome, Republicans have won the White House 10 times and Democrats 12 times. But what happens after the election is over, and does it matter which party wins the presidency? Overall, the likelihood of a stock market gain in the first year after a presidential election has been a little more than 50% (12 out of 22 instances).

While the average gain for these 22 post-election years is a modest 5.2%, strong moves in one direction or the other are frequent occurrences. In fact, 77% of these years saw double-digit changes in the S&P 500 – nine with double-digit gains and eight with double-digit losses. In addition, as is the case now, when a Republican followed a Democrat, the market declined during the first year of the term in all four cases. However, looked at differently, dating back to 1901, the Dow Jones Industrial Average has risen at a 7.03% annualized pace when there has been a Republican president and Republican Congress.

While a recession is not our expectation, early on in a president’s term is usually when they begin. Over the past 88 years, nine of the 14 U.S. economic recessions began in the year following the election. Additionally, three others began during the presidential election year (1948, 1960, and 1980). That would definitely put a damper on market returns this year, but a recession in 2017 is not our expectation.

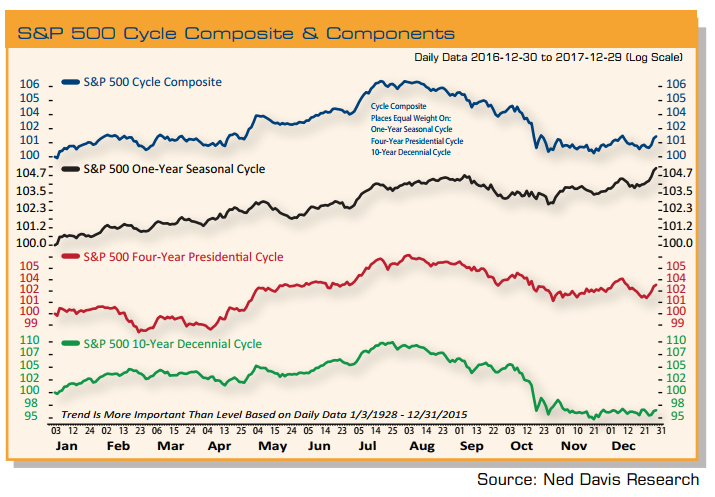

In fact, as noted earlier, we expect the economy to accelerate given pro-growth policies of the new administration, tax reform, regulation reform, and a strengthening global economy. U.S. Equity Market The Ned Davis Research Cycle Composite is a combination of the market’s historical one-, four-, and ten-year cycles combined into a single composite.

It is a tool we use that helps provide a framework for or possible roadmap of how the market may trade in the coming year. In the past it has served us well in formulating our Outlooks and the market tracked the cycle composite very closely last year.

{kind=link}

The top clip in this chart is the cycle composite for 2017. The other three clips are the components of the composite, the one-, four-, and ten-year cycles. The cycle composite suggests a mostly positive trend during the first half of the year, but then reverses early in the third quarter due primarily to the decennial cycle. Postelection years have also tended to be weak in the second half. Part of the reason is that government stimulus tends to decline after the election.

A big fiscal stimulus plan, which is being talked about by President-elect Trump, would contradict that tendency. In addition, the market gains could be front loaded on expectations of policy initiatives that may not be fully realized, which could result in some volatility in the second half of the year.

In last year’s Outlook, we discussed the historic tendencies of how the market traded in election years and noted the trading range that it had been in since peaking in May 2015, which ultimately continued throughout the first half of 2016.

Historically election years are typically weaker in the first half and then rally strongly in the second half of the year. History proved to be a good guide as that certainly was the pattern last year. The market broke to the upside in early July after the Brexit vote, but it wasn’t until after the presidential election that the market really advanced sharply.

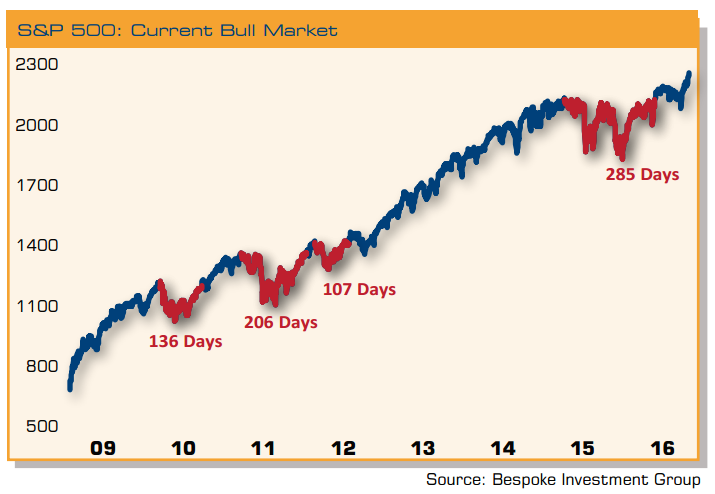

This chart shows the S&P 500 during the current bull market and highlights in red those periods of consolidation of 100 or more trading days without hitting a closing high. While it’s normal for stocks to consolidate, the 285 trading day period that spanned May 2015 into July of 2016 was the longest consolidation period of the current bull market by nearly eighty trading days.

{kind=link}

Establishing a new high for the S&P 500 is a rare occurrence following a pause of 300 or more calendar days. According to analysis from Merrill Lynch this has happened only 23 times since 1929 and the resulting advances have been very strong. The S&P 500 has gained an average of 15.6% during the year following such an extended pause and has been higher 91% of the time.

If that historical average gain is realized, it targets 2470 on the S&P 500 in mid-July. In addition, within the context of secular bull markets, weak years (defined by an S&P 500 total return of 5% or less) have historically been followed by two years of strength. In secular bull market periods dating back to 1946, there have been nine years prior to 2015 with gains of 5% or less. The subsequent gain over the next two years has averaged 49.4%.

In 2015, the S&P 500 posted a total return of 1.4%, which qualifies as a weak year. If history repeats this trend, the S&P 500 could have a surprisingly strong year in 2017. For example, the S&P 500 gained a total return of 11.95% in 2016. To reach the historic two year average of 49.4% referenced above, the S&P 500 would need to post a 33.5% gain in 2017. Now we don’t expect the market to achieve those types of gains, but these historic trends help to underscore the positive backdrop for the equity markets.

Risks In the market Outlooks that we have done over the past two years, we have said that “Our single biggest concern continues to be stretched valuations.” Well, here we are again and we can say the same thing. But a year later in the bull market, there are additional concerns including the age of this bull, geopolitical risks from the rise of Populist movements across Europe, the Middle East immigration crisis, and now, for the first time in over a decade, the real threat from rising interest rates.

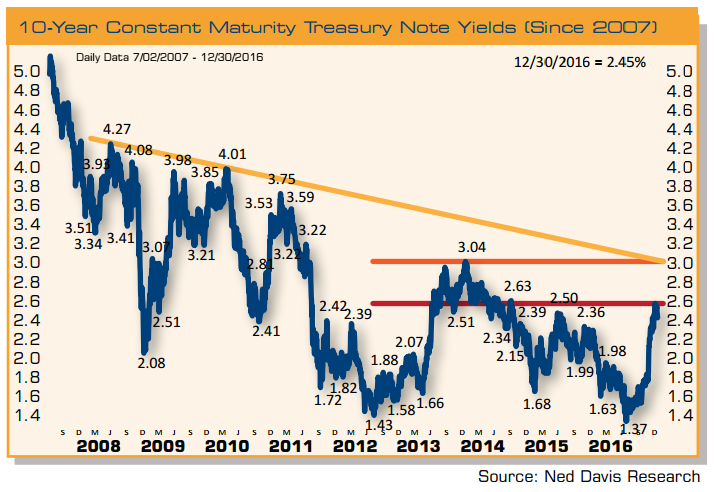

On the valuation front, the median P/E ratio for the S&P 500 is 22.9, which is near the upper end of its range excluding the late 1990s/early 2000s bubble. Interest rates and multiples tend to be inversely correlated, so multiples could contract if the Treasury yield climbs toward 3%, which is our upside target for yields over the intermediate term.

{kind=link}

Valuations can and have remained stretched for extended periods so they are not timing tools, but more of a measure to assess potential risks. Our conclusion is the same as it was for the past two years, stretched valuations don’t necessarily mean that a bear market is imminent, but they do place increased importance on earnings growth. And fortunately the earnings recession of last year is over. Earnings declined for six consecutive quarters with earnings turning positive again in the third quarter of 2016.

With valuations and multiples stretched, the market needs earnings growth to support the expensive valuations. Earnings growth is expected to be in the low single digits for the fourth quarter of 2016 but to jump into the double digits in the first and second quarters of 2017. For all of 2017, current estimates project S&P 500 earnings growth to be very solid at 12.3%. That would be very supportive for the market. We think there is potential for an upside surprise affecting even these earnings expectations based on the accelerating economic growth and corporate tax reform, which is not currently reflected in the consensus numbers.

Earnings are in the sweet spot for the market having turned up following a six quarter decline and are set for solid growth. Earnings growth is an offsetting factor to the valuation concerns. Margin debt is another risk that bears watching. Margin debt is a reflection of speculative excesses that often develop late in a bull market. As a percentage of GDP, margin debt hit an all-time high in April 2015 and has since contracted.

This is something we have been watching, looking for clues that the bull run is beginning to wane, since past peaks in margin debt have occurred near market tops. However, for now, margin debt has rebounded with the market but it so far has failed to surpass the previous peak and therefore remains a concern that we are monitoring closely.

The S&P 500 has now been up on a total return basis for eight straight years and we have been mostly bullish over that span. The all-time record for consecutive up years is nine (1991—1999), so another year of gains would tie that record. That helps underscore one of the risks of this aging bull. This is now the second longest bull market since 1932, only the bull market of the 1990s was longer. We have said many times over the past couple of years that bull markets don’t typically die of old age, but at the same time, a longlived bull market can be a risk that bears close scrutiny.

{kind=link}

Fixed Income Inflation is a growing concern for the Fed but they still may be underestimating what lies ahead. Fed officials currently expect core inflation for personal consumption expenditures to remain below their 2.0% target until late 2018. Yet emerging evidence and leading inflation indicators paint a different picture. While Core CPI has been relatively stable at 2.1% over the past year, the Future Inflation Gauge from the Economic Cycle Research Institute moved up to an eight-and-a-half-year high and the Ned Davis Research Inflation Timing Model is in a solid uptrend. Both of these indicators point to inflation pressures building, in addition to the wage pressures we discussed earlier.

As we observed before, the Federal Reserve seems to be behind the curve with upside risks to inflation. The latest comments out of the Fed are somewhat at odds between letting the economy “run hot” and setting expectations of three additional rate hikes in 2017. However, if recent history is any guide, the Fed will fall short of hiking rates as often as they suggest given that they only hiked rates once in each of the past two years. We expect the Fed to hike rates twice in 2017.

However, in our opinion, it is not how many times the Fed raises rates that is most important, but what the Federal Reserve Board looks like over the next couple of years. Janet Yellenwill not be reappointed as Fed Chair when her term expires on January 31, 2018. Trump will have an incredible opportunity to shape the Board of Governors. In addition to nominating a new Chair, he will fill at least two other vacancies on the board. The 10-year Treasury yield surged from a post-Brexit low of 1.36% to a post-Trump victory high of 2.60%, rising nearly 125 bps. The 10-year yield ended 2016 at 2.45%. Essentially the 10-year Treasury yield made a round trip with the journey beginning with a 100 bps decline early in the year, followed by a Trump election victory surge.

Our expectation is that the pace of the backup in yields will slow as widespread pessimism among bond investors is now evident. As a result, we may witness this current area holding for the moment as yields consolidate. Our intermediate-term stance is that we will see the 3.0% level on the 10-year Treasury Note, which represents the January 2014 high, and in our opinion, that level is key to the long-term outlook. While 3.0% is our intermediate-term upside target for yields, we think yields could back off that level and we have a yearend target of 2.75%.

{kind=link}

Our long-term view on interest rates is that the low is in and a new secular bear market has begun. However, that does not mean that fixed income investors are doomed to experience losses. History suggests quite the opposite. For example, the 10-year Treasury yield has risen in 19 of the 41 years since the inception of the Barclays Aggregate Bond Index.

In 16 of those years, or 84% of the time, the Aggregate Bond Index gained as rates rose. In addition, yields rose in 13 of the 33 years since the inception of the Barclays High Yield Index. High yields rose in 10 of the 13 years, or 77% of the time, and the average gain in those years was 11%. In addition, yields rose in 16 of the 37 years since the inception of the Barclays Municipal Bond Index. Muni bonds rose in 11 of the 16 years, or 69% of the time that rates were rising. Finally, using the Barclays Aggregate Bond Index since its inception, only 1% of the total return has been from price appreciation, 16% of the index total return has been from coupons, and a staggering 83% of the index return has been from reinvesting coupons.

This is why higher rates are not entirely bad, higher rates often mean higher coupons and more reinvestment income. In our Outlook last year, we stated that “High yield bonds have one of the best risk-adjusted return profiles.” High yield bonds certainly did turn in great performance in 2016 with the Barclays High Yield Index up 17.13%. In a highly anticipated and telegraphed move, the Federal Reserve hiked interest rates for only the second time in over a decade during the fourth quarter and, leading up to the event, there was some fear and trepidation about the impact that any rate hike would have on the fixed income markets. So far this time, as with the rate hike in 2015, there has been no real negative impact on the markets. We have often said that we believe high yield would outperform in rising interest rate environments.

Over the past 23 years, there have been seven instances where the 10-year Treasury yield has risen by over 100 bps. In each one of those cases, high yield bonds posted positive total returns while Treasuries were lower across the curve. The current case, now the eighth time rates have risen by at least 100 bps, is no exception.

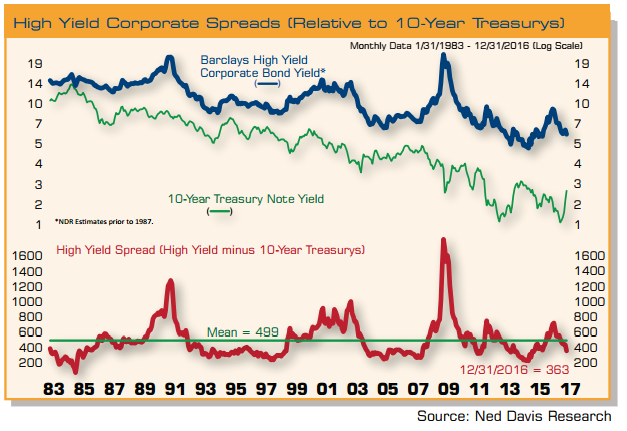

The 10-year Treasury yield bottomed on July 8th at 1.36% and so far has risen to a high of 2.60% on December 16th, rising nearly 125 bps. From that point to the end of the year, the Barclays 7-10 Year Treasury Index was down 6.96% while the Barclays High Yield Index was up 5.93%, outperforming Treasuries by 1289 bps. High yield credit spreads have fallen from a peak of 840 bps in February to 363 bps at yearend.

The only times in which high yield bonds as an asset class traded at a higher spread to U.S. Treasuries than this past February was in the recession of 1990, the early 2000s, and the 2008-2009 credit crisis. Further, the only time that high yield spreads came close to the same level as on February 11th in a non-recessionary environment was during the U.S. debt downgrade in 2011. In each of these examples, once spreads contracted they stayed low for several years.

{kind=link}

It is unlikely that we will see the same surge in credit this year as we saw in 2016, but with little chance of recession over the next 12 months and higher interest rates coming, we continue to overweight credit. We enter 2017 favoring high yield, as history shows that spreads can remain tight for a long period of time without an economic downturn.

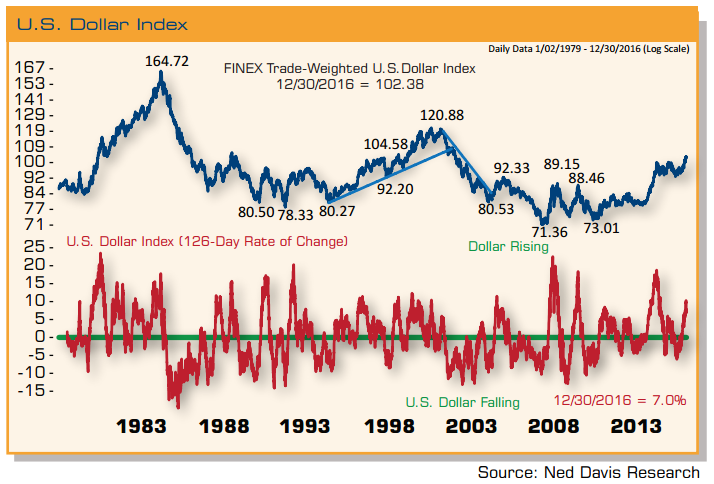

Additionally, higher inflation means a reduced probability of default, and historically, higher inflation expectations have correlated with falling credit spreads. U.S. Dollar The trade-weighted U.S. dollar gained 3.6% in 2016, but that only tells part of the story.

The dollar traded in a large sideways consolidation pattern from March 2015 until breaking out to the upside just after the presidential election. The dollar has gained 10.4% since hitting its low of that consolidation in May. As the Fed continues along its tightening cycle, the dollar will likely continue to rally and that will have economic implications here in the U.S.

A general rule of thumb is that each 10% move in the dollar is about the equivalent of a 1% hike in the Fed Funds rate. So a strengthening dollar has a tightening effect, which could be another reason why the Fed may fall short in the number of hikes this year.

{kind=link}

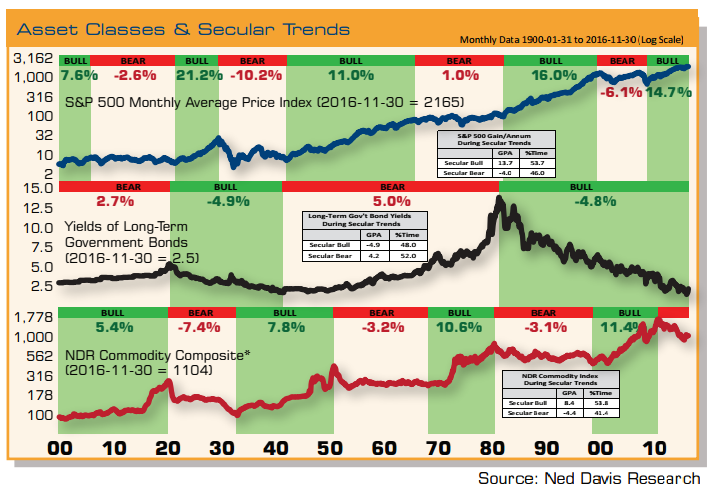

Secular Let’s shift focus and look at the secular trends. We like to keep the secular trend in focus as it helps to put the short-term environment into its proper perspective. This chart shows asset classes and secular trends. Stocks are on top, Treasury yields in the middle, and commodities on the bottom. The shaded green areas represent secular bull markets in each asset class.

The key to this chart is the checkered look and identifying when each asset class is in a secular bull. We can see that when commodities are in a secular bull, stocks are in secular bear, and when stocks are in a secular bull, commodities are in secular bear. Such is the case currently and this reinforces our view. Stocks have risen at a 14.7% average annual rate since bottoming in 2009. We have been highlighting the fact that the next secular trend to come to an end is likely that of bonds. The long-term sentiment in bonds has quickly shifted from lower for longer to too low for too long and the Fed is behind the inflation curve.

{kind=link}

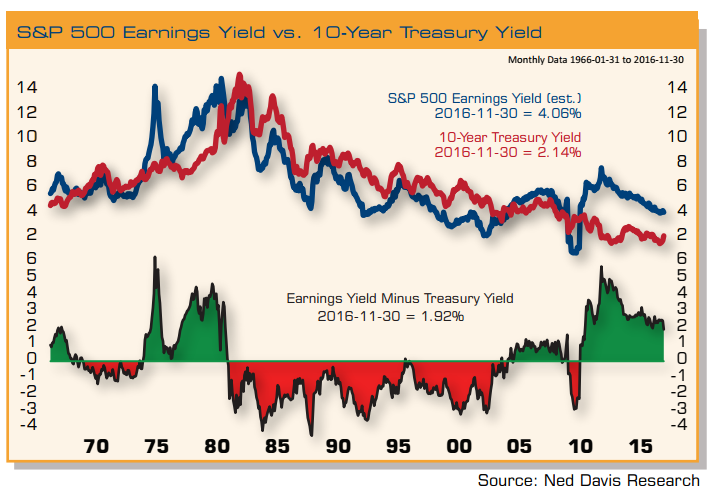

As we mentioned at the outset, our long-term view is that we are in a secular bull market in stocks. While stocks are expensive in absolute terms based on P/E multiples, price to book ratios, and almost any fundamental measure, on a relative valuation basis stocks look cheap compared to bonds. Comparing the relative valuation of stocks to bonds using the S&P 500 earnings yields and the 10- year Treasury yield, stocks are undervalued compared to bonds.

{kind=link}

Over the past 10-years, the S&P 500 is up 95% and the Barclays Long Term Treasury Bond Index is up 91%. It is rare for stocks and bonds to have similar returns and even more rare for bonds to outperform stocks over a rolling 10-year period. When it does happen, stocks usually go on to dramatically outperform bonds over the next period. We are just coming off a period when bonds outperformed stocks, and on a 10-year total return basis, stocks are one standard deviation undervalued compared to bonds.

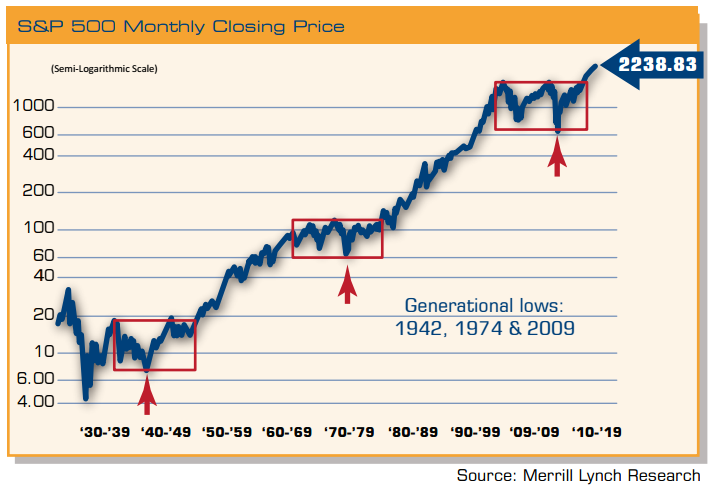

This is a long-term supporting factor in favor of a continued secular bull market in stocks, especially with interest rates now moving higher. As we finish I’d like to look at past secular trends. The three boxes in red highlight the last three secular bear markets. Of note is that once the market eclipsed its prior secular peak, it continued higher for many years. The prior two secular bull runs lasted 22 and 18 years. That is the environment we live in today. Of course there will be cyclical bull and bear markets as always, but the primary secular trend appears to be higher and if history is any guide it has the potential to have some staying power.

{kind=link}

In conclusion, we are still in a secular bull market in stocks and have a positive outlook. According to post-election year trends, we should see strength early on with potential weakness in the back half of the year. The economy should accelerate based on progrowth policies and we expect 3.0% GDP growth, while the economic expansion continues through yearend. The secular trends are in favor of stocks while the long-term trend has changed from bull to bear for bonds. Treasury yields are likely to continue rising but at a slower pace. Given the trend change in fixed income, we see the need to really manage risk in fixed income by taking an active and opportunistic approach.

Sean Clark is the Chief Investment Officer at Clark Capital Management, which is a participant in the ETF Strategist Channel

Disclosure Information:

Forward-looking statements are not guaranteed. The discussions, outlook and viewpoints featured are not intended to be investment advice and do not take into account specific client investment objectives. The opinions expressed are those of the Clark Capital Management Group Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Clark Capital investment portfolio. Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. For educational use only. This information is not intended to serve as investment advice. This material is not intended to be relied upon as a forecast or research. The investment or strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Past performance is not indicative of future results. Clark Capital Management Group, Inc. reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security, sector or industry. There is no assurance that any securities, sectors or industries discussed herein will be included in or excluded from an account’s portfolio. It should not be assumed that any of the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services can be found in its Form ADV which is available upon request. The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 75% of U.S. equities. Barclays 7-10 Year Treasury Index tracks the investment results of an index composed of U.S. Treasury bonds with remaining maturities between seven to ten years. Barclays 20+ Year Treasury Index tracks the investment results of an index composed of U.S. Treasury bonds with remaining maturities greater than 20 years. S&P GSCI Index is an unmanaged world production-weighted index composed of the principal physical commodities that are the subject of active, liquid futures markets. S&P GSCI Industrial Metals Index is considered representative of investment performance in the industrial metals market. The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performers of developed markets outside the U.S. and Canada. The MSCI World Index is a freefloat-adjusted market capitalization index that is designed to measure global developed market equity performance. The MSCI World Index ex. U.S. is a freefloat-adjusted market capitalization index that is designed to measure global developed market equity performance excluding the U.S. The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index. The Value Line Arithmetic Composite Index uses the arithmetic mean change in the index reflects change if a portfolio of stocks in equal amounts were held. The S&P MidCap 400 Index measures the performance of mid-sized companies, reflecting the distinctive risk and return characteristics of that market. The S&P Small Cap 600® measures the small-cap segment of the U.S. equity market being designed to track companies that meet criteria showing that they are liquid and financially viable. The VIX Index is a forward looking index of market risk which shows expectation of volatility over the coming 30 days. Barclays U.S. Government/Credit Bond Index measures the performance of U.S. dollar denominated U.S. Treasuries and government-related & investment grade U.S. Corporate securities that have a remaining maturity of greater than one year. The Barclays U.S. Aggregate Bond Index covers the U.S. investment-grade fixed-rate bond market, including government and credit securities, agency mortgage pass-through securities, asset-backed securities and commercial mortgage-based securities. To qualify for inclusion, a bond or security must have at least one year to final maturity, and be rated investment grade Baa3 or better, dollar denominated, non-convertible, fixed rate and publicly issued. The Barclays U.S. Corporate High-Yield Index covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. The iPath® S&P 500 Dynamic VIX ETN is designed to provide investors with exposure to the S&P 500® Dynamic VIX Futures™ Total Return Index. The S&P 500® Dynamic VIX Futures™ Total Return Index (the “Index”) is designed to dynamically allocate between the S&P 500® VIX Short-Term Futures™ Index Excess Return and the S&P 500® VIX Mid-Term Futures™ Index Excess Return by monitoring the steepness of the implied volatility curve. The Index seeks to react positively to overall increases in market volatility and aims to lower the roll cost of investments linked to future implied volatility. Index returns include the reinvestment of income and dividends. The returns for these unmanaged indexes do not include any transaction costs, management fees or other costs. It is not possible to make an investment directly in any index.