By Gary Stringer, Kim Escue and Chad Keller, Stringer Asset Management

Operation Twist was the media’s term for the U.S. Federal Reserve’s (Fed) actions in late 2011 and early 2012 when the Fed was trying to “twist” the yield curve by pushing short-term interest rates higher and long-term interest rates lower.

In the 2011 version of Operation Twist, the Fed was trying to stimulate the U.S. economy. We think that next year the Fed will again influence a yield curve twist by increasing short-term interest rates, while global pressure will keep long-term interest rates from moving as much.

Rather than stimulate the economy, this time the Fed’s goal is to offset some perceived harmful side-effects of fiscal stimulus. Short-term yields may increase 1.0%, while global demand for U.S. Treasury bonds may keep a ceiling on long-term yields at about 0.30-0.50% higher than current levels. The collision of fiscal stimulus and Fed monetary policy tightening may increase market volatility, but economic fundamentals remain sound.

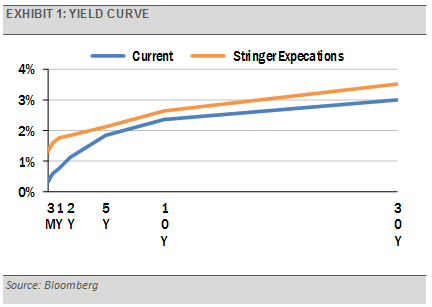

The yield curve reflects the difference between the interest rates on short-term and long-term bonds. The U.S. Federal Reserve (Fed) attempts to manipulate the yield curve from time to time as part of its monetary policy toolset. In late 2011 and early 2012, the Fed attempted to “twist” the yield curve by pushing short-term rates higher and long-term rates lower via actions the media referred to as Operation Twist. In the 2011 version of Operation Twist, the Fed was trying to stimulate the U.S. economy.

With the new presidential administration’s well publicized fiscal stimulus plans coming at a time when the Fed views the economy at near full employment, the Fed may believe that new fiscal stimulus will increase inflationary pressure. As a result, the Fed may raise interest rates more quickly and persistently than the market expects.

We think that for the first time this cycle, the Fed’s “dot plot” underestimates the pace of upcoming Fed rate rises.

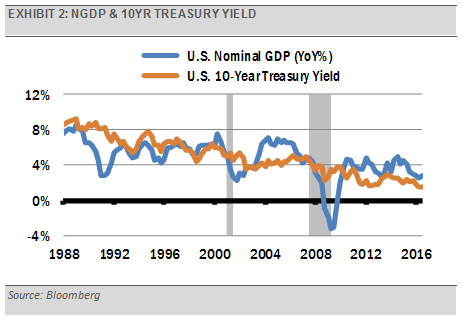

We expect more volatility around interest rates, but most of the movement will be at the short end of the yield curve. We think that the curve will flatten as short-term yields rise faster than long-term yields. Long bonds are priced off nominal GDP (real GDP + headline CPI).

However, Fed policy largely pivots off core inflation measures, excluding food and energy prices. We expect core inflation to move more slowly than headline CPI, which includes food and energy. For example, the recent rally in oil prices has resulted in higher headline CPI, while core inflation remains muted.

As a result, Fed policy may lag inflation and will need to play catch up as inflation builds. Whereas a year ago we thought the data did not support the multiple rate hike plan put forth by the Fed in late 2015, we think there is a high probability that the Fed will raise rates faster and more persistently than currently expected due to increasing inflation pressure coming from fiscal stimulus in 2017. This may push short-term rates up 1.0% next year.

{kind=link}

Meanwhile, stable but sluggish global economic growth should combine with strong demand for U.S. Treasury bonds to keep a lid on long-term interest rates at 0.30-0.50% higher than current levels.

Moving to the broader economy, increased inflation expectations have caused us to raise our forecast for nominal GDP (NGDP) from 3.7% to 4.2%. Our prior forecast already included an increase in productivity from 0.5% to 1.8%, so this expectation does not change much under the new administration’s proposed policy shifts. Instead, we expect increased inflation until the Fed’s tighter monetary policy takes hold.

{kind=link}

Since 1988, the 10-year Treasury has averaged 0.30% more than NGDP overall, roughly even in non-recessionary environments, and is averaging 1.3% lower than NGDP during the current global low interest rate environment. Combining this with our current NGDP forecast gives us: 4.2%-1.3% = 2.9% as an expectation for the 10-year Treasury yield.

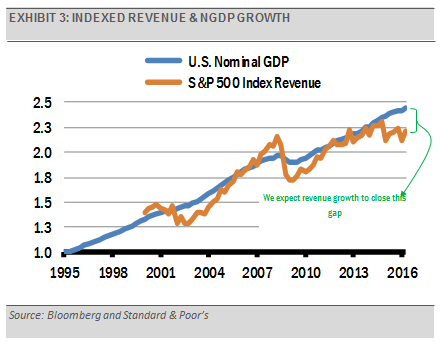

The collision of fiscal stimulus and tightening monetary policy may lead to significant volatility. Economic and market fundamentals remain strong, so we view equity market volatility and declines in this context as buying opportunities. Higher nominal GDP has implications for higher corporate revenue and earnings growth, which we have been saying for months that we expect to accelerate. Higher revenues and increased earnings can support higher stock prices going forward.

In short, we think the U.S. economy will continue to grind forward but uncertainty revolving around the struggle between fiscal stimulus and the Fed’s mandate of keeping inflation contained will result in increased market volatility.

{kind=link}

Gary Stringer is the CIO, Kim Escue is a Senior Portfolio Manager, and Chad Keller is the COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.