When will economic indicators finally be considered strong enough for the Fed to act?

{kind=link}

By Hafeez Esmail, Main Management Chief Compliance Officer

While sovereign bond yields appear to be edging higher around the world, thus far the Fed seems to be persisting in their reluctance to acknowledge this reality. US economic indicators, on the whole, have been consistently positive (albeit not dramatically so) over the past 6 months. As a result, it looks like the Fed will be following interest rate movements higher, not leading them.

Globally, China’s growth seems to be picking up again, and Europe continues to muddle along, including the U.K. which has, thus far, fared well economically post the Brexit vote. There is also a growing perception that the Central Banks recognize that Quantitative Easing (QE) has its limitations. Concerns that European Central Bank (ECB) may curtail its monthly 80 Million Euro bond purchases have rattled fixed income markets. Japan has put a cap on its 10 Year Note at zero, no doubt to provide a sliver of opportunity for inflation to develop. As a result, interest rates may have bottomed and possibly be heading higher.

{kind=link}

While the US economy is not robust, it may be the strongest among the developed world as a number of leading indicators continue to move up. The recent Institute of Supply Management (ISM) data on manufacturing and services and both exceeded estimates. The manufacturing number swung back into expansion at a 51.5 level, up from 49.4 and the non-manufacturing numbers notably improved from a level of 51.4 up to 57.1 as can be seen below.

{kind=link}

One of the economic indexes that Main Management follows closely is put together by the Economic Cycle Research Institute (ECRI) which was founded by Geoffrey Moore, whom The Wall Street Journal called “the father of leading indicators”. The Index of Leading Economic Indicators (LEI) is based on his original work. Before there was a committee to determine U.S. business cycle dates, Moore decided all those dates on the National Bureau of Economic Research (NBER’s) behalf from 1949 to 1978, and then served as the committee’s senior member until he passed away in 2000. The ECRI Index has been getting steadily stronger as can be seen below and is beginning to look like it may surpass the 2007 highs.

{kind=link}

The September Jobs Report also brought additional encouraging data points. One positive was that the Civilian Labor Force expanded by 444,000 people. Labor force expansion usually occurs when people feel more confident about finding a job and thus begin to actively seek to do so. Consequently, the bump in the unemployment rate from 4.9% to 5.0% was actually a result of greater job market participation. Also notable was that wages in September were up 2.6% year over year, a particularly bright spot that bodes well for the Fed’s inflation target of 2%.

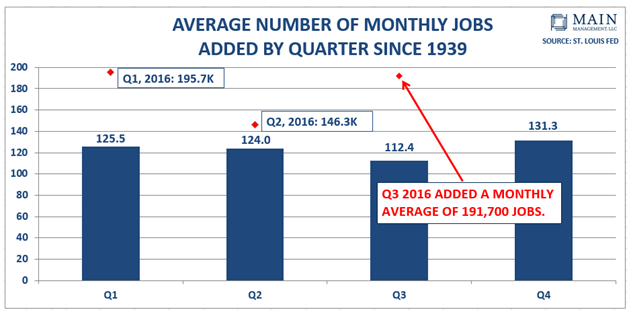

While the September jobs number itself wasn’t particularly strong at 156,000 jobs, if you include the total number of jobs added in July and August and take a monthly average, the third quarter (Q3) on average added 191,700 jobs per month. The chart below shows this is well above the average number of monthly jobs added for the third quarter (Q3) which averages 112,400 monthly jobs dating back to 1939. Moreover, this closely mirrors the robust 195,700 average from the first quarter of 2016.

{kind=link}

There are a number of positive data points that might ordinarily prompt the Fed to act on raising interest rates. Perhaps the prevalence of negative sovereign interest rates to combat a weaker global economy weighs on their collective minds. The fear that higher interest rates will strengthen the dollar, which may put more pressure on corporate margins and thereby negatively impact the outlook for exports, may also have created some trepidation. That said, the greenback is still lower than it was at the start of 2016. However, domestic economic indicators continue to provide ample ammunition for the Fed to pull the trigger, an event we anticipate finally occurring in December.

Hafeez Esmail is the Chief Compliance Officer at Main Management, a participant in the ETF Strategist Channel.

A pioneer in managing all-ETF portfolios, Main Management LLC is committed to delivering liquid, transparent and cost-effective investment solutions. By combining asset allocation insights with smart implementation vehicles, Main Management offers a unique approach that translates into distinct advantages for our clients, including diversification, cost efficiency, tax awareness and transparency. http://www.mainmgt.com