{kind=link}

ETFs provide investors a wide range of choices to access world markets via a liquid, cost-effective vehicle. The growth of ETFs has seen many types of exposure become available, especially in equities. Of course, the most popular ETF is the SPDR S&P 500 (SPY), which tracks the S&P 500. The S&P 500 Index is a cap-weighted index that is based on the market cap of each stock. Market cap is driven by price and shares outstanding; the higher the price, the higher the size of the stock in a cap-weighted index.

A hot topic the last few years in the financial industry has been smart beta (or strategic beta). Many ETFs have launched that take various different “smart beta” or alternative weighting approaches to cap-weighted indices. At Swan, we believe in being always invested and always hedged and that this combination will provide for a smoother and better risk-adjusted experience for an investor over the long-term. But in this post, we want to focus on an alternative way to use ETFs to approach the “always invested” side when considering the S&P 500. There are many different types of alternative weighting methods to a cap-weighted index, like fundamental or factor-based weighting, but we will mostly focus in this post on just one of these, equal sector weighting.

Swan believes there are numerous benefits to an equal-weighted sector approach to the S&P 500 (let’s just call it EQW from here on out). These include:

- Potential for increased performance

- Better diversification

- Potential for lower volatility and beta

- Ability to lessen the impact of sector bubbles within the stock market

- Slight tilt to value and mid-cap/smaller stocks (as compared to mega cap)

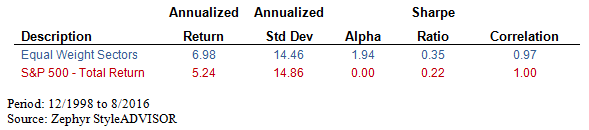

Here are some of the risk and performance metrics between cap-weighted and EQW since late 1998 when the SPDR Select Sector ETFs were launched:

For each of the past 4 calendar years EQW has slightly underperformed the cap-weighted SPY, but prior to that there were 12 straight years of outperformance. When using the S&P 500 sector indices back to 1990, prior to the launch of the SPDR Select ETFs in late 1998, EQW outperformed in 5 of those 9 years. The average annual difference over the entire time period (1990-2014) was +1.01% for EQW, with a maximum of +10.95% and a minimum of -6.35%. (Source: Morningstar) Furthermore, EQW provided better diversification over this time frame and lower volatility and beta than the cap-weighted price-driven SPY.

The main points for an equal-weighted sector approach are these:

- Seeks to avoid the flaws of cap weighting (cap weighting only focuses on price and bubbles/overvaluation can form more easily)

- Applies a built-in “buy low/sell high” discipline that is based on the principle of mean reversion

- An equal weight approach is more value conscious and tilts to mid/smaller stocks

- Numerous studies across various assets indicate an equal-weight approach outperforms cap-weighted

In today’s post, we will only focus on the first two points in favor of equal sector weighting. In next month’s post, we will take a look at the last two points.

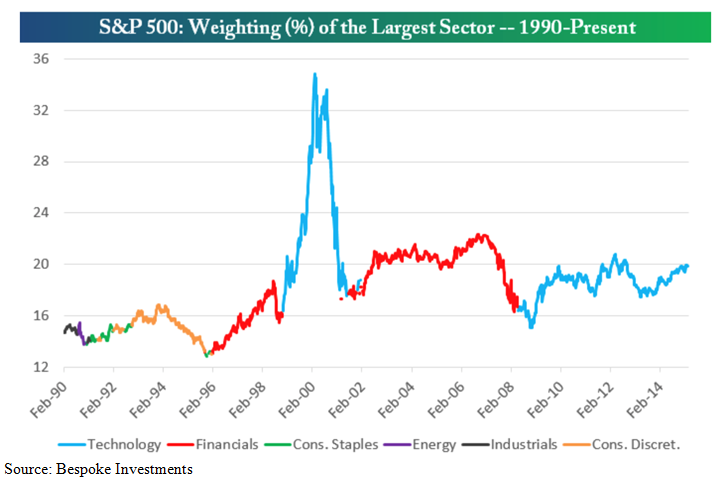

The only thing that matters to a market capitalization index is price; nothing else is taken into consideration. This means an “anti-value” approach is taken. As stocks and sectors become overvalued, bubbles can develop within a cap-weighted index. This can be easily seen during the years leading up to the Tech Crisis and the Financial Crisis. Tech stocks in 1999 and Financial stocks in 2007 became overvalued and occupied a larger than normal portion of the S&P 500 index. As seen below, the leading sector in the S&P 500 can vary over time and be driven to abnormal percentages of the index. The graph visualizes the largest sector of the cap-weighted S&P 500 and the weighting of it over time. An equal-weight approach helps to avoid this potential for bubbles and some of the collapse that inevitably follows them. In fact, the last three “bubbles” all occurred in the largest sector of the S&P 500 at the time; sectors which had grown to be the largest in a relatively short period of time (Energy in the 80’s, Technology from 2000-2002, and Financials in 2008-2009).

Charles Mackay once said: “Men, it has well been said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

Stock markets have a tendency for this to happen as people herd into stocks, usually within a particular sector. Although there might be a good reason for the enthusiasm initially, eventually business conditions change and the sector can’t keep up with investor’s expectations. With an equal weight sector weighting, exposure to any specific sector or bubble is always kept limited. This will mean underperformance while that sector is on the upswing, but outperformance when it falls back to earth. This approach, however, does not completely insulate the investor from overvalued and price-driven stocks since it is still cap-weighted within the sectors, but it does have less dependency on the largest holdings.