By Scott Kubie, CFA, CLS Investments Chief Strategist

On a beautiful fall day in 2002, I walked into a room of financial planning clients full of dread. I was about to present CLS’s then-new Risk Budgeting Methodology to individual investors for the first time. Just the day before, I had presented it to advisors for the first time. It hadn’t gone well. I had struggled to overcome their preference for the stock-to-bond ratio.

To my surprise, the clients loved it and understood it nearly right away. Why had the clients been able to grasp something advisors could not?

Hundreds of presentations later, the answer is easier to apprehend. Advisors struggled because they had grown attached to the stock-to-bond ratio of a portfolio as a good way to express and measure risk. The clients had not. While the clients were free to accept a new idea, the advisors had become tied to stock-to-bond.

Using the stock-to-bond ratio to measure risk exemplifies the made-up word “complify.” Complify means something becomes more complicated as a result of efforts to simplify it. While stock-to-bond looks simple on the outside, its underlying weaknesses make it a poor measure of risk.

{kind=link}

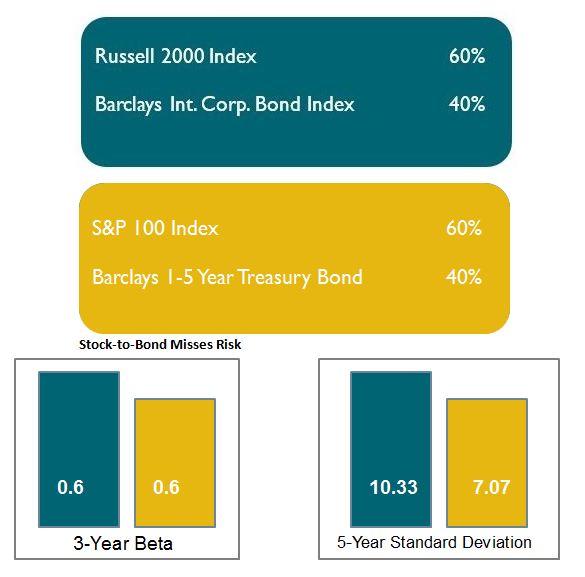

The two portfolios above highlight the challenges of stock-to-bond. Both have a stock-to-bond ratio of 60/40. As the charts below show, the risk isn’t all that close. The top portfolio is riskier using two different risk measures and time frames.