Stocks and bonds go together like peanut butter and jelly: truly a case where the sum is much, much greater than the composite parts.

Or, at least, it has been.

In 2013, however, John Bogle, renowned founder of The Vanguard Group, began critiquing core U.S. bond indices as being fundamentally broken. At the time, the issuance-weighted Barclay’s U.S. Aggregate Bond Index had a hefty 70% allocation to debt backstopped by the U.S. government, including Treasuries and agency MBS. His argument, at the time, was that the intermediate-term bond portfolio most investors hold looks much more like the other 30% of the portfolio, making the overall index an inappropriate benchmark for passive tracking.

We can look under the hood of the iShares Core U.S. Aggregate Bond ETF (AGG), which tracks the Barclay’s U.S. Aggregate Bond Index, to see that not much has changed since 2013.

{kind=link}

What we see is that U.S. Treasuries and MBS pass-throughs still comprise 60%+ of the portfolio. In fact, over 80% of the portfolio is comprised of just three sectors.

Just how important are these three sectors to the overall return of the portfolio?

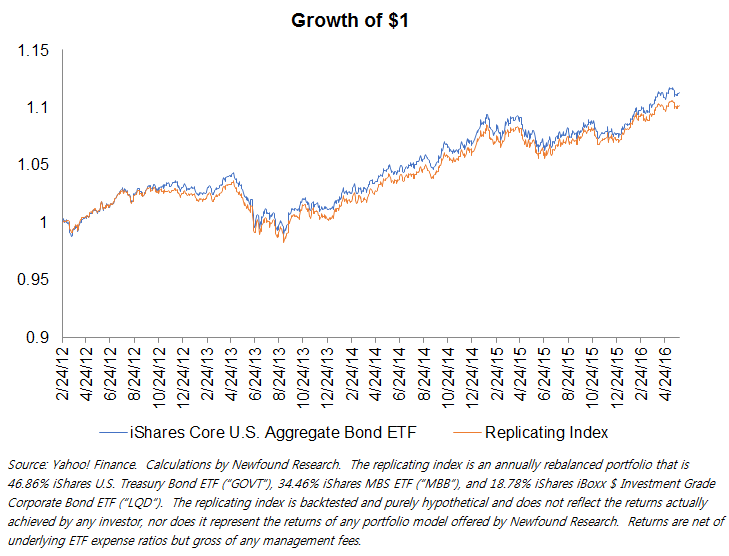

One way to explore this question is to try to cut out the fluff and replicate the index by building a portfolio using just the three primary sleeves. Fortunately, there are ETFs available that represent these three sectors: the iShares U.S. Treasury Bond ETF (GOVT), the iShares MBS ETF (MBB), and the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD).

By setting the other sectors to a 0% allocation and normalizing, we end up with a portfolio that is 46.86% GOVT, 34.46% MBB, and 18.78% LQD. How close does this portfolio come to replicating the performance of AGG?

{kind=link}

Almost spot on. (It is worth noting that the weighted expense ratio of the ETFs in the replicating index is 19.8 basis points (“bp”) while the expense ratio for AGG is 8bp. About half of the performance differential above can be explained by this fee difference.)

So what’s the takeaway? Turns out, for once, the risks may be pretty transparent here: tracking AGG will leave an investor massively over-allocated to U.S. Treasuries and U.S. agencies.

Is that a problem? We think so, for two reasons.

The first has to do with return. With GOVT and MBB yielding 1.42% and 2.00% respectively, the core driver of total return for bonds is pitifully low, especially after we account for inflation.

The second has to do with risk. While the replicating index portfolio is made up of three three sectors – none of which represents more than 50% of the overall portfolio – the returns of the sectors are highly correlated. In other words, they don’t necessarily represent three unique return sources, but share among them a high degree of overlapping risk.

SEE MORE: Rethinking Bond ETFs – Unbundle and Rebuild

Using quantitative techniques, we can back out the implied number of statistically unique factors that are driving returns in the portfolio. As it turns out, 91% of the variance in portfolio returns can be explained by a single factor: risk-free (i.e. Treasury) interest rate risk. The other 9% of variance is explained by credit risk.

For investors looking to diversifying their stock allocation, bonds have historically offered an attractive proposition: lower volatility, a steady source of income, and the potential benefit of offsetting returns from a flight-to-safety in a crisis.

SEE MORE: Alternative ETFs Have a Volatility Problem

Today, the de facto standard for fixed income benchmarks – the Barclay’s U.S. Aggregate Bond Index – offers little real yield and has incredibly low internal diversification. With rates near all-time lows, does it make sense to diversify our stocks with a portfolio where 91% of the risk is driven by long interest rate exposure – a bet that will only pay off if rates go lower?

We think not.