Environmental, Social, and Governance (ESG) investing has become more popular in recent years.

While not a new phenomenon within the institutional space, the popularity of ESG investing in ETF land is increasing. While the number of both broad and more niche ESG-type ETFs keep increasing, AUM in two of the original ESG-type ETF is nearing a combined $1 billion dollars:

I will not go into the benefits of ESG investing, whether qualitative or quantitative, as there are numerous sources available that can further delve into this issue!

Up to now, the broader ESG ETFs had a primarily US focus. However, recently there have been a few new ETFs that focus on the international markets. In the following, I will examine these new broad-based international ESG ETFs

Developed

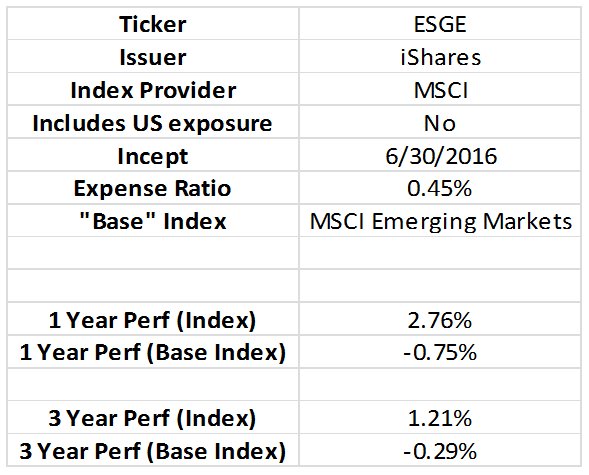

In the developed market space, there are two new ETFs offering broad ESG exposure. Here is a table with some characteristics:

{kind=link}

While the iShares offering focuses solely on EAFE exposure, FlexShares is Global so it will include US exposure (about 56.5% at month end).

Starting with the FlexShares offering, you can see there is a rather large amount of (positive) performance differential between its index and its base index. Here is a description of the ESG filter applied to the base index (via the FlexShares site):

The STOXX® Global ESG Impact Index offers exposure to a set of global, developed-market companies that is tilted towards companies scoring better with respect to a select set of environmental, social, and governance (ESG) key performance indicators (KPIs). Eligible securities are selected from the STOXX Global 1800 Index. The bottom 50% of such companies based on their ESG KPI scores are excluded from the Index, as are companies that do not adhere to the UN Global compact principles, are involved in controversial weapons or are coal miners (ICB Subsector 1771). Components are then weighted by free-float market cap combined with a cap factor that is based on a company’s aggregate ESG KPI score. Component weightings may also be adjusted to ensure that the weight representation of each country in the Underlying Index does not vary from that in the STOXX Global 1800 Index by more than +/-1 percentage point and that the weight of a single company is less than 5% at time of each index rebalancing or reconstitution.

As you can see, the index rules are a bit exclusionary, with over 50% of the base index names being eliminated through low scores and other criteria. This could lead to some idiosyncratic risk, but the other index rules in place should mitigate some of these concerns.

SEE MORE: Digging into Two Thematic Health ETFs

Moving onto the iShares offering, you can see the performance differential is much smaller, although still positive on the periods analyzed. An index description from MSCI (which applies to both EAFE and Emerging Markets, which I will touch on later) sounds somewhat similar to that of the STOXX index mentioned above:

MSCI ESG Select Indexes: The indexes are designed to maximize exposure to positive environmental, social and governance (ESG) factors while closely tracking the risk and return characteristics of the underlying market capitalization weighted indexes. Each index is constructed by selecting constituents from a Parent Index through an optimization process that aims to maximize exposure to ESG factors, subject to a target tracking error budget under certain constraints. The indexes are sector-diversified and target companies with high ESG ratings. Tobacco and Controversial Weapons companies are not eligible for inclusion in the indexes.

So while they both focus on the top tier ESG scoring companies, it appears the MSCI index has a bit more focus on tracking and limiting factor divergence from the base index, while STOXX has a bit more leeway in tracking the base index.

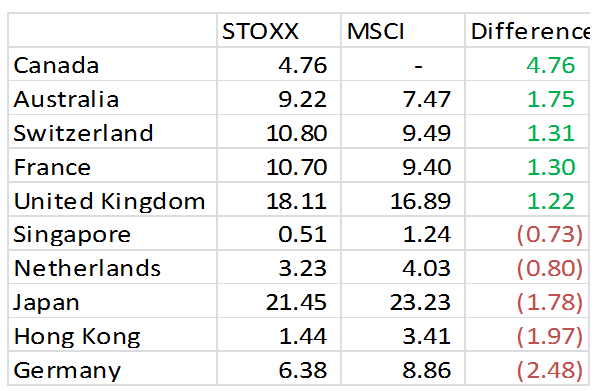

There are also differences, outside of the Global vs EAFE aspect, between the MSCI EAFE and STOXX Global 1800 that can affect the differentials as well. Here I have isolated the non-US exposure in the STOXX version and common sized it back to 100 to get a more apples-to-apples country comparison (showing top and bottom five differentials only):

{kind=link}

Since STOXX is Global and MSCI is EAFE, the largest differential is going to be the Canada exposure. On the opposite end, the STOXX version has a comparative underweight to the Asian countries.

Stepping back a bit, here are some examples of the sector and industry deviations in ESGD compared to the base index as of month end:

- Sector Overweight: Industrials +1.62%

- Industry Overweight: Road & Rail +0.73%

- Sector Underweight: Consumer Staples -1.45%

- Industry Underweight: Tobacco -1.78% (which is completely expected since ESG investing excludes tobacco companies)

Emerging

To fill out the international ESG ETF lineup is one Emerging Markets offering:

{kind=link}

Although similar in design to its EAFE counterpart, the index has experienced a greater amount of positive dispersion from its base index over these periods. Here are some current exposure deviations:

- Sector Overweight: Financials 1.62%

- Industry Overweight: Banks 4.15%

- Sector Underweight: Consumer Staples -1.83%

- Industry Underweight: Food Products -1.07%

Summary

While the popularity of ESG investing in the US seems to be taking off given the increased AUM and number of tickers available, ETF investors can now apply similar ESG constraints to the international portion of their portfolios as well. While these new ETFs are in their infancy, the performance of the benchmark indices seems to show some positive price performance over their non-ESG counterparts. Combine this with the qualitative benefits of ESG investing and these new ETFs could soon find their way into portfolios.

Clayton Fresk is a Portfolio Manager at Stadion Money Management, a participant in the ETF Strategist Channel.

[related_stories]Disclosure Information

Past performance is no guarantee of future results. Investments are subject to risk and any investment strategy may lose money. The investment strategies presented are not appropriate for every investor and financial advisors should review the terms and conditions and risks involved. Some information contained herein was prepared by or obtained from sources that Stadion believes to be reliable. There is no assurance that any of the target prices or other forward-looking statements mentioned will be attained. Any market prices are only indications of market values and are subject to change. Any references to specific securities or market indexes are for informational purposes only. They are not intended as specific investment advice and should not be relied on for making investment decisions. The STOXX Global 1800 Index contains 600 European, 600 American and 600 Asia/Pacific region stocks represented by the STOXX Europe 600 Index, the STOXX North America 600 Index and the STOXX Asia/Pacific 600 Index. The MSCI EAFE (Europe, Australasia, and Far East) Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. One cannot invest directly in indexes, which are unmanaged and do not incur fees or charges. Founded in 1993, Stadion Money Management is a privately owned money management firm based near Athens, Georgia. Via its unique approach and suite of nontraditional strategies with a defensive bias, Stadion seeks to help investors—through advisors or retirement plans—protect and grow their “serious money.” Contact Stadion at 800-222-7636 or www.stadionmoney.com. SMM-082016-566