Related: The Bayesian View to Multi-Factor ETF Investing

Simple enough, right? This would keep investors broadly diversified and invested, while altering their risk profiles slightly during weaker periods of time. Many practitioners have followed a similar strategy with different tools.

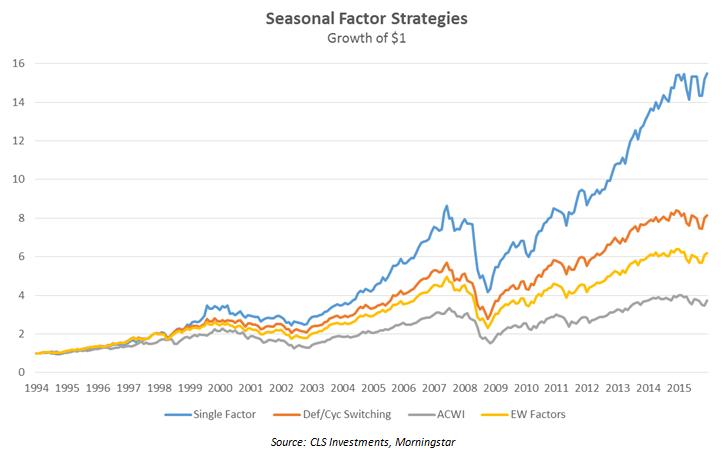

In the chart below, the orange line demonstrates the performance of this strategy over time, generating significant alpha above the ACWI and above an equally-weighted mix of all six factors we covered here. Of course, this is excluding transaction costs and ignoring the fact that there aren’t currently ETFs covering all of these ACWI factors.

{kind=link}

Source: CLS Investments, Morningstar, MSCI

If one were to simply invest each month in the factor that has historically had the highest batting average (percent chance to outperform), the results are quite impressive, as indicated by the blue line. This is similar to that of the defensive and cyclical-switching strategy, but utilizes only a single factor. During the months of January and February size is favored; minimum volatility is utilized in the summer; and momentum in the later months of the year. Very simple, yet very impressive results. However, we are faced with the possibility that past results won’t correlate with the future and the potential for incurring sizeable transaction costs associated with making those monthly trades.

While seasonality is thought by many to be consequential, there are still important and relevant considerations for the active manager when allocating throughout the year. Utilizing factors in strategies like these greatly increases diversification and can also reduce the chances of being wrong, particularly versus a sector-timing strategy. Factor investing is becoming a more important part of the investing landscape, particularly as high fees and active management come under pressure. Being able to utilize factors to an investor’s advantage is crucial. Now we just need the ETFs to do it!

Related: Are Factor ETFs the Key to Unlocking Your Portfolio’s Risk DNA?

This information is prepared for general information only. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. The graphs and charts contained in this work are for informational purposes only. No graph or chart should be regarded as a guide to investing.

Grant Engelbart is a Portfolio Manager at CLS Investments, a participant in the ETF Strategist Channel.