Note: This article is part of the ETF Trends Strategist Channel

By Chris Hausman

On any given day, ETF trading volume is usually some of the heaviest in the world. Increased volume in the underlying ETF can directly lead to an increase in the corresponding option volume. The option markets can provide a way for investors to hedge their portfolios and/or the potential to produce portfolio yield enhancement through the use of “income” producing strategies. There has been a paradigm shift between trading stocks on individual equities to trading ETFs.

The increase in option volume has stemmed from not only active traders, but end users such as portfolio managers. Trading ETFs provide certain advantages including, but not limited to, transparency, cost-effective structures, and tighter bid-ask spreads for options. The shift to ETF options only makes sense as users demand “cleaner” and more versatile products. Option volume on all ETFs now accounts for nearly 70% of aggregate option volume while trading in actual ETFs account for approximately 30% of equity volume (Source: Bloomberg).

Most ETFs provide specific exposure to a certain industry or even a commodity. Some of the ETFs that are on the higher end of the option volume ladder are: iShares Russell 2000 (IWM), PowerShares QQQ (QQQ), SPDR Gold Trust (GLD), iShares Barclays 20+ Year Treasury Bond (TLT), and the United States Oil Fund (USO).

However, the distinction for the most ETF option volume belongs to the SPDR S&P 500 (SPY). Options on SPY represent about half of all ETF option volume. Not only is SPY option volume the leader of all ETFs, but it is usually near the top for global equity indices battling other products such as the CNX Nifty Options, Kospi 200 Options, and Euro Stoxx 50 Options. The popularity of SPY options can be attributed to more money managers using options in their portfolios. In addition to substantial liquidity, bid-ask prices are usually 1-2 cents wide.

Related: Why Volatility Can Be a Drag for Investors

A portfolio manager can execute substantial size in the SPY options without having a significant impact on option prices. Below is a sample option chain for the SPY showing Bid-Ask prices and Open Interest. At the money options, and options closer to expiration customarily see the most “action.” Nevertheless, liquidity in strikes away from the money and further out in time still provide excellent liquidity providing traders and portfolio managers the ability to execute more esoteric option strategies.

{kind=link}

Tighter bid-ask prices on individual calls and puts can also lead to better prices on spreads. What many portfolio managers do not realize, in addition to the listed exchange markets, there is an “upstairs world” of market makers and liquidity providers. They have been a primary driver in the growth of the industry and why options have become so mainstream over the years.

The perceptions on the use of options has shifted from speculative instruments to manageable investment vehicles. The advent of ETFs has allowed the use of options in portfolios to flourish in recent years. The graph below shows monthly option volume in the SPY with a 10 month simple moving average. Even though the average may not be near its peak during 2011, option volume remains extremely firm over the last five years. Unfortunately, looking at option volume only paints half the picture and one must analyze open interest as well.

{kind=link}

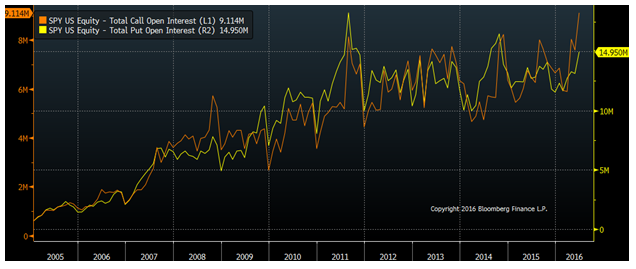

The next chart, clearly shows a rising trend in open interest for both calls and puts. Open interest now completes the picture indicating more participants. Volume may be about the same over the last five years, but a higher open interest implies positions are being held. One interpretation may be a longer holding period for options via long-term hedging or more spreads being traded as a result of tighter bid-ask spreads, or simply more end-users.

{kind=link}

The creation of ETFs has created a world of opportunity from stock indices, currencies, sectors, commodities, and bonds and this world has been expanded through the use of options. Options are a versatile tool to control risk or enhance returns either broadly or tactically in a portfolio at a fraction of the cost of an outright ETF. Option strategies that involve hedging, overwriting, equity replacement, or cross-asset hedging have now shifted from individual equities to ETFs.

Related: Math Matters – Rethinking the Calculations Behind Investment Returns

Due to increased liquidity and open interest trends, options on ETFs provide traders and portfolio managers the ability to enter and exit positions with ease and little impact to overall pricing. The bottom line, volume engenders volume and the end result is increased liquidity leading to tighter bid-ask prices and more opportunity for all.

Chris Hausman is a Senior Trader and the Chief Market Technician at Swan Global Investments, a participant in the ETF Strategist Channel.

[related_stories]Disclosures:

Swan Global Investments is a SEC registered investment advisor providing asset management services utilizing the Swan Defined Risk Strategy, allowing our clients to grow wealth while protecting capital. Please note that registration of the Advisor does not imply a certain level of skill or training. Swan Global Investments, LLC is affiliated with Swan Capital Management, LLC, Swan Global Management, LLC and Swan Wealth Management, LLC. Disclosure notice and privacy policy.