Note: This article appears on the ETFtrends.com Strategist Channel

By Marc Odo

Read the fine print of the disclosures of a leveraged exchange traded fund (ETF) and you’ll probably come across something like the following:

“This leveraged ETF seeks a return that is +200% or -200% of the return of its benchmark index for a single day. The ETF should not be expected to provide double or negative twice times the return of the benchmark’s cumulative return for periods greater than a day.”

Wha…?!

This simple disclosure describes an important mathematical property that can have a large impact on investors, but is especially pronounced for those using leveraged ETFs.

The situation being described here is known as volatility drag. Also known as variance drain, volatility drag is the long-term, detrimental impact that volatility has on an investment. Any volatile investment will be subject to volatility drag. But the greater the volatility and the longer the time horizon, the more detrimental the impact of volatility drag tends to be.

Leveraged ETFs, by their very nature, are designed to be more volatile than their underlying investment, so the impact of volatility drag is especially pronounced with leveraged ETFs.

The best way to illustrate the impact of volatility drag is via a simple example.

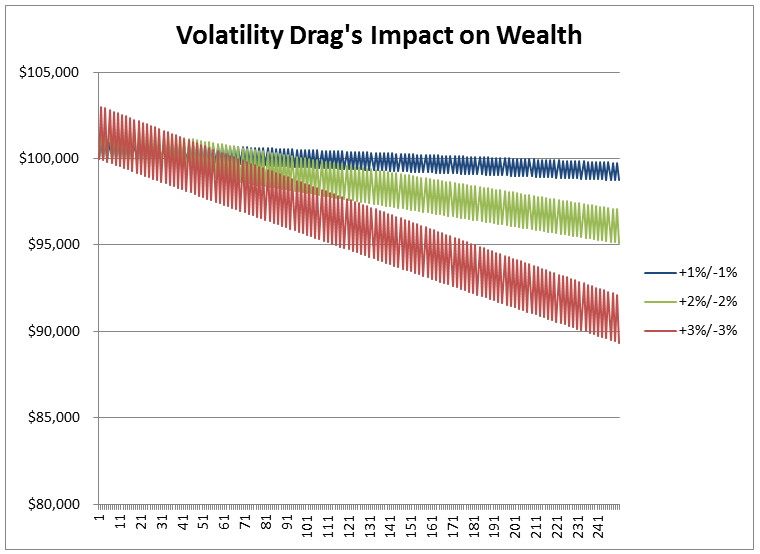

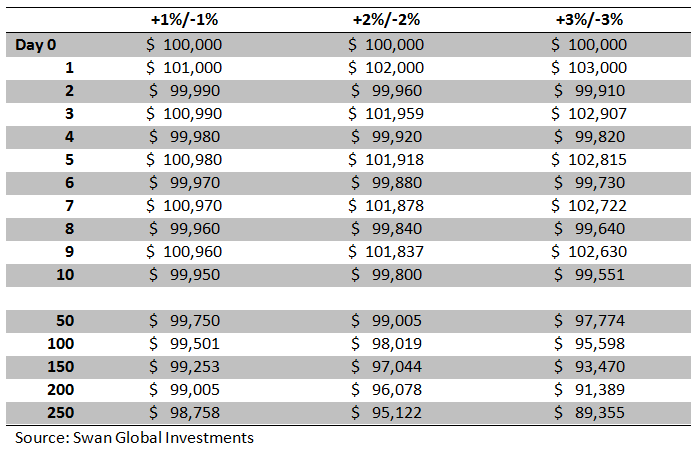

Let’s say, for example, we have an investment that returns +1% on even number days and -1% on odd numbered days. Setting aside calendar vagaries like weekends, holidays, and the like, let’s assume that the investment alternates between gains and losses of 1% every day it trades. Let’s also assume that we have x2 and x3 leveraged versions of this same investment that will return +2%/-2% and +3%/-3% in the same pattern. At the end of some holding period, what will the final values be?

Simple, back-of-the-napkin math might lead one to conclude that the gains and losses perfectly offset each other and at the end of a year or so the net return for all three alternatives will be zero.

However, that simple analysis is grossly incorrect.

Why?

Because it fails to take into account the compounding impact of returns. Once all of the daily returns are linked together in a sequential fashion, it becomes painfully obvious that volatility can “drain” return. Moreover, the longer the time horizon, the worse the results.

{kind=link}

{kind=link}

Starting with an initial theoretical investment of $100,000, after ten trading days the +1%/-1% investment is down $50 from its starting point. Meanwhile, the +3%/-3% leveraged investment is down almost $450 over that same time span. After 250 days, roughly the number of trading days in a year, the unleveraged investment has lost $1,242, or 1.24% of its initial value. However the triple-exposure option has lost $10,645, or 10.65% of its value.

Another way to interpret the above example is that avoiding losses is more important than capturing all the gains. In the above example, the size and count of the individual moves are equal on the upside and the downside. However, the final, aggregate results are tilted towards losses because losses have more of an impact than gains.

Of course in the real world investment returns are nowhere near as predictable as illustrated in this simple example. This case study was simply meant to illustrate the three general take-aways regarding volatility drain, namely:

- Volatility tends to have a detrimental impact on wealth

- The more volatile the investment, the bigger the impact

- The longer the time horizon, the bigger the impact

Certainly if one seeks to profit handsomely from short-term, high-conviction, speculative positions then leveraged ETFs might provide a good vehicle for doing so. Also, if we had an investment that always posted positive returns, never negative returns, volatility drain wouldn’t be much of a concern. However, as a long-term, buy-and-hold investment vehicle, leveraged ETFs carry risks that need to be fully understood to be appreciated. Alternatively, those investing for the long haul should be actively seeking out solutions that minimize volatility.

Swan Global Investments explores volatility drain and several other key mathematical principles in a new white paper called “Math Matters: Rethinking Investment Returns” by Micah Wakefield. Often overlooked or misunderstood, these key mathematical principles are essential to the success or failure of a long-term investment plan.

Swan Global Investments is a SEC registered investment advisor providing asset management services utilizing the Swan Defined Risk Strategy, allowing our clients to grow wealth while protecting capital. Please note that registration of the Advisor does not imply a certain level of skill or training. Swan Global Investments, LLC is affiliated with Swan Capital Management, LLC, Swan Global Management, LLC and Swan Wealth Management, LLC. Disclosure notice and privacy policy. 112-SGI-051016