Note: This article appears on the ETFtrends.com Strategist Channel

The important distinctions between what dominates GDP growth versus S&P earnings

By Hafeez Esmail

The BLS jobs reports from the first quarter of 2016 were generally robust and ahead of consensus estimates. However, for the month of April, a mixed report showed that jobs expanded by 160,000 in total non-farm employment. This number was short of estimates, which were calling for 200,000 new jobs. Nonetheless the monthly average of 203,000 over the past 3 months and 232,000 over the past year indicate respectable growth.

That said S&P 500 profits and revenues have failed to reflect nearly as rosy a picture. According to Factset with 95% of companies reporting Q1 earnings through 5/20/16, just over half of the companies (53%) have reported sales above mean estimates which is below the 5 year average. Although actual EPS above estimates (71%) is above the 5 year average, the earnings trends are not awe inspiring.

Related: Are Interest Rate Hikes ‘Back on the Table’?

The year over year blended earnings decline for Q1 2016 is -6.8%. Factset also notes that this is first time the S&P 500 has seen four consecutive quarters of year-over-year declines in earnings since Q4 2008 through Q3 2009. While Consumer Discretionary and Telecom Services have been the sector leaders in earnings growth, Energy, Materials, and Financials are the key laggards.

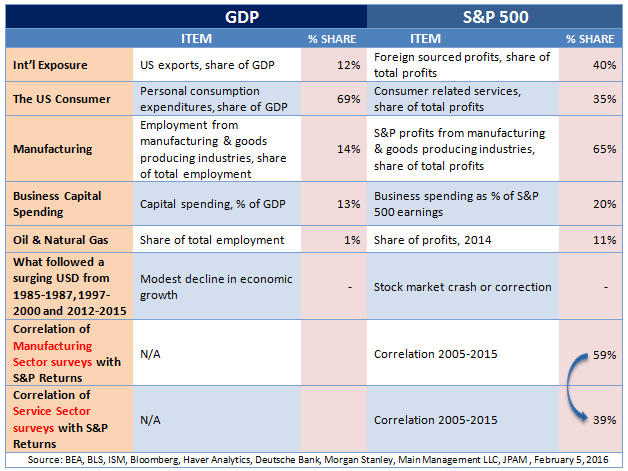

So what might explain the disconnect between the US Economy and Equity Markets? One important factor may be the extent to which S&P 500 earnings are composed of companies engaged in manufacturing and energy production. As the table below underscores, 65% of S&P profits are derived from manufacturing and good producing industries. By contrast only 14% of Americans are employed by manufacturing and good producing industries.

Accordingly drawdowns in manufacturing related businesses may have a sizable impact on S&P 500 earnings while having a notably lesser impact on the employment picture. This could explain why the economy has had fairly strong jobs numbers over the past year which drastically differ from weakening S&P 500 earnings during the same time frame.

Related: A Two Speed Economy

Furthermore it’s a common refrain that two thirds of GDP is driven by the consumer. Various data sources bear this out highlighting that, in fact, personal consumption makes up a 69% of the economy. By contrast consumer related services are almost half this figure as a percentage of S&P 500 earnings at 35%.

Accordingly factors that significantly move the economy appear to have a far lesser impact on equity market profits. To underscore the point the higher correlation of Manufacturing Sector surveys to S&P 500 profits (59%) again points to a greater impact that Service Sector inputs with a correlation of just 39%.

Another key element to note is the currency impact on S&P earnings. Given manufacturing’s influence on corporate profits it is noteworthy that this sector tends to be more influenced by a strong dollar. As the greenback surges, US goods appear more expensive in foreign markets, while overseas goods feel more affordable stateside. So while US exports are a mere 12% of GDP, foreign sourced profits are a considerably larger 40% share of S&P earnings.

{kind=link}

There remains little doubt that the economic factors that drive GDP clearly influence corporate earnings. However it’s important to identify the sectors with a more meaningful impact on each metric. The role of manufacturing on corporate earnings may be underappreciated by investors at their peril.

If the Fed does raise rates more than once during the balance of 2016 foreign buyers, seeking relatively higher yields than the sovereign debt of most developed nations, may look to accumulate more US Treasuries. If that does occur this could bring about further dollar strength. As such this could be an important factor in S&P profits for the balance of 2016 and is certainly worth watching.

Hafeez Esmail is the Chief Compliance Officer at Main Management, a participant in the ETF Strategist Channel.