Note: This article appears on the ETFtrends.com Strategist Channel

By Scott Kubie, CFA, CLS Chief Strategist

Market bubbles occur when the price of an asset significantly deviates from its intrinsic value. There have been numerous bubbles predicted in my 20 years as a professional investor. Fortunately, only two, from the perspective of U.S. investors, came to pass. The technology bubble in 2000 and the financial crisis in 2008.

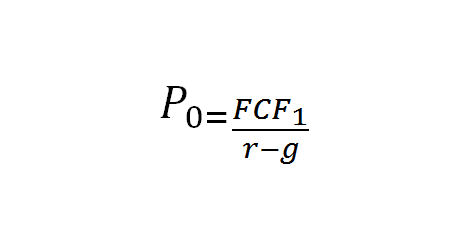

Bubbles are hard to identify until they occur. Let’s look at this equation:

{kind=link}

It offers a way to identify the next bubble: understand how previous bubbles formed. Before expanding that thought, a little about the equation. P0 represents the fair price or intrinsic value. It is a function of three variables:

- Free cash flow (FCF) one year in the future

- The required rate of return (r in this equation, although k is sometimes used)

- The future growth rate (g in this equation)

Whether you totally grasp the equation or not, the key points are: higher cash flow and growth raise the value of the firm, and a higher required rate of return lowers the value. The last two U.S. market bubbles occurred because investors were fooled by inflated values in one of these numbers.

[related_stories]Interestingly, the 2000 and 2008 bubbles occurred in different parts of the equation. In 2000, investors assumed Internet companies would take over every aspect of commerce. Small startups were projected to grow into behemoths down the road. The growth rates assumed far outpaced potential, and a bubble ensued. High price-earnings (P/E) ratios for technology stocks were an expression of high growth expectations. As growth (g) gets closer to the required rate of return (r), valuations can get very high.

2008 resulted from inflated cash flow. In this period, investors assumed the high profits and cash flow generated from housing loans were sustainable. Instead, those numbers were based on errant assumptions about the housing market. Those profits were restated as massive losses in the following years. In this case, the valuations looked legitimate the entire time; it was the profit numbers that were inflated.

Related: The Bayesian View to Multi-Factor ETF Investing

So, where should we look for the next bubble? Investors and generals are known for fighting the last war. People looking for financial decline due to increasing student loan debt or riskier car loans are looking in the wrong places. Even the optimism in Internet firms or biotech companies pales in comparison to 2000’s tech bubble. Instead, look to the variable in the equation that hasn’t caused a recent bubble. Required rates of return (r) may be too low for some assets.

While I don’t expect a bubble, there are three areas I consider as possible sources:

- Reduced-volatility strategies: ETFs have provided access to asset classes not previously available. Low- and minimum-volatility strategies have become very popular with investors because they can lower the risk of the portfolio. While these strategies lower risk consistently, they can still become overvalued.

- Interest rates: In spite of trends to the contrary, I remain concerned bonds offer very little premium for assuming inflation risk.

- Income portfolios: Income investors often assume they will earn yield and a couple of percent, in the long run, from capital appreciation. What if the pursuit of yield has made price depreciation the more likely scenario?

Bubbles are hard to predict, and are predicted far more often than they occur. While I don’t expect any of the scenarios above to become bubbles, that doesn’t mean the CLS portfolio management team isn’t watching.

Related: Do ETFs and Moving Averages Mix?

Investing involves risk. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. This information is prepared for general information only. Past performance is not a guide to future performance. An ETF is a type of investment company whose investment objective is to achieve the same return as a particular index, sector, or basket. To achieve this, an ETF will primarily invest in all of the securities, or a representative sample of the securities, that are included in the selected index, sector, or basket. ETFs are subject to the same risks as an individual stock, as well as additional risks based on the sector the ETF invests in.

Scott Kubie is the Chief Strategist at CLS Investments, which is a participant in the ETF Strategist Channel.