Lowering volatility is key to achieving better compound growth as volatility diminishes the rate at which an investment grows over the long-term. When two investments with the same average return are compared, the one with the greater volatility, or variance, all other things being equal, will have a lower compound return.

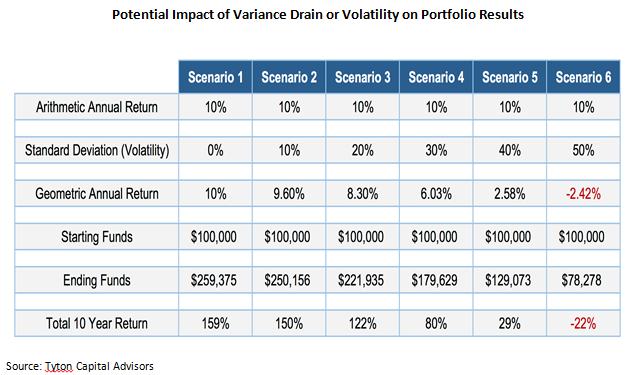

This table shows 6 different scenarios, all having an arithmetic annual return of 10%. However, each scenario has a 10% increase in its volatility of returns. Notice the drain on the geometric annual return and the ending dollar value as the volatility increases.

{kind=link}

Obviously, averages don’t tell the full story. The S&P 500 has averaged roughly 9.5% per year since 1928. You would want that investment, right? Especially in the current market environment, 9.5% sounds pretty great. But how many years did the market actually have a return in the 9%-10% range? The answer might surprise you. Over the last 87 years, in only 2 years was the market near its long-term average returning 9 or 10% and only 4 years within 2% of its long-term average – that’s only 5% of the time (Source: Morningstar). More often than not the market’s return in any given year was much greater or much lower than 9.5%. And that is the problem with averages and focusing on them. Averages, by their very nature, mask volatility.

Of course, in reality, not everyone wants an investment that grows at an “average” 9.5% if it involves multiple -40% to -80% drawdowns and sometimes decades of negative return in order to get there, as has been seen with the S&P 500. This type of ride makes it very difficult for investors to stay the course and actually achieve that return and sequence of returns or withdrawal risk also becomes a bigger factor.

Swan believes these basic mathematical principles are mostly misunderstood or overlooked by many investors today. It is of vital importance that investors study and understand the mathematical principles behind investment returns in order to have proper expectations for their investments and to help them find the best possible solutions for reaching their financial goals. At Swan, we believe that an ETF-managed solution like our hedged equity Defined Risk Strategy (DRS) has some mathematical advantages to traditional equity. By seeking to avoid large losses and lower volatility, the DRS looks to take advantage of these mathematical principles and their important impact on long-term results.

We believe that the majority of an investor’s portfolio should be structured to avoid large losses, not exposed to undefined risk. No matter the portfolio construction though, we want to help investors think outside the box and expand their mindset past focusing on short-term returns by simplifying difficult mathematical concepts to a more understandable level.

Swan’s efforts to expand investor’s understanding of how math impacts their portfolios is explored in further detail in a piece titled “Math Matters: Rethinking Investment Returns and How Math Impacts Results”. Both an executive summary and comprehensive version are available.

Micah Wakefield is Director of Research and Product Development at Swan Global Investments, a participant in the ETF Strategist Channel.

[related_stories]