One theory that seems to make some sense is that the market is currently viewing the drop in oil as a reflection of collapsing commodity prices and a world devoid of aggregate demand.

When viewed through that prism, the market may rightly be focusing on the shorter term consequences of oil based debt defaults that could overwhelm the positive effects of lower gas prices for consumers.

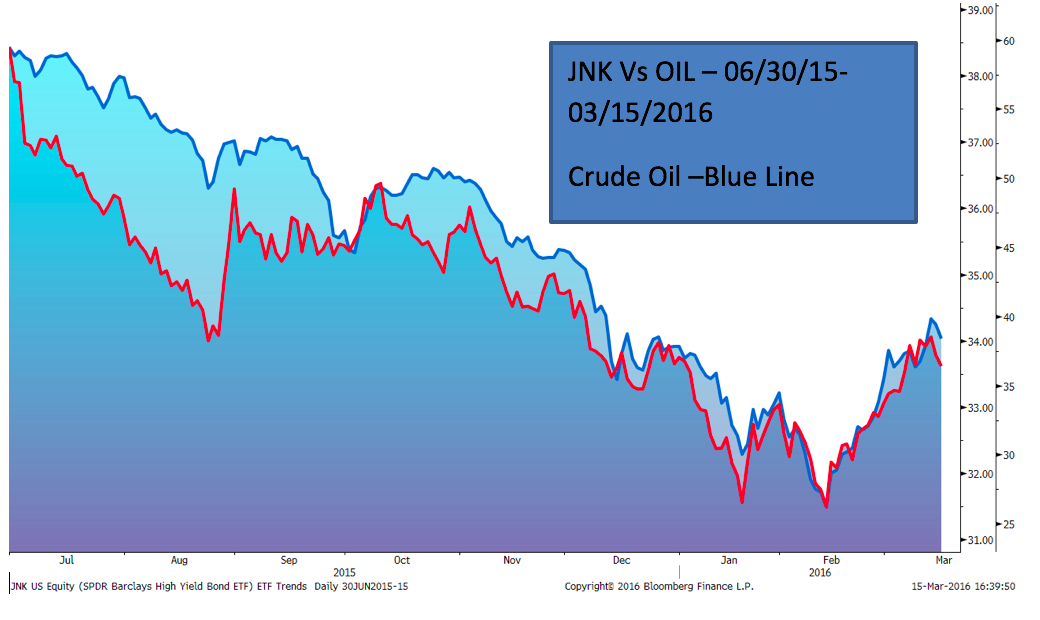

One confirmation that this thesis is on the right track can be seen in high yield bond indices that have a concentration of energy holdings, and have been plunging along with oil and gas for multiple quarters now.

Like equities, the longer term historical correlation between High Yield and oil is somewhat low at .17 but has recently jumped to approximately .52 during 2016 (again, according to data from Ned Davis Research).

{kind=link}

One last angle to consider is the amount of program trading that now occurs on a day to day basis. In a world where computers are moving markets, it is fair to say that algorithmic trading may have something to do with watching oil and stock markets moving in tandem. Eventually we would expect this short term spike in correlations to run its course, much like the direction of the Euro and stock prices did after the European crisis of 2011 began to calm down. But until the correlation breaks and computer trading systems change their calculations, a view on oil will likely be synonymous with a view on equity markets. So if you want to know where markets are headed in the shorter term, keep watching oil.

Note: Our next article will cover our view of whether crude oil has truly bottomed, or is just in the midst of a dead cat bounce. Stay tuned.