Minimizing Volatility in a Global Multi-Asset Class Portfolio

Volatility, as measured by the CBOE Volatility Index (VIX), has spiked markedly over the past 6 months. This has left investors looking for ways to minimize volatility in their portfolios. Assuming that an investor already has the correct asset allocation to fit their risk tolerance, there are ways to change the mix of securities to minimize volatility within an investment portfolio. First, investors can own cash. Cash preserves capital in down markets, but can cause portfolios to lag in up markets. Second, investors can own bonds. Fixed income securities typically become safe havens in times of market turmoil, and can prove to be ballast in one’s portfolio that adds stability. Third, investors can tilt their portfolio in a more defensive manner. One such method is to employ minimum volatility strategies within a portfolio to participate in up markets, but limit drawdowns in volatile markets.

Using Minimum Volatility ETFs within a Core/Satellite Construct

At Nottingham, we’ve incorporated minimum volatility ETFs as an overlay within the core of our asset allocation portfolios, choosing to focus on the risk reduction characteristics that a minimum volatility tilt can add to a portfolio over a business cycle (in terms of an improved Sharpe Ratio). However, utilizing a minimum volatility strategy as a tactical, or satellite position can work as well. Portfolio managers looking to de-risk an equity portfolio without eliminating equity exposure outright may find minimum volatility ETFs to be useful. This type of strategy would be akin to tactically using momentum (or a similar factor) in an upward trending market.

Factor based ETFs such as the iShares U.S. Minimum Volatility Portfolio (USMV) seek to optimize the securities within its index by creating a minimum variance portfolio, complete with sector constraints (+/- 5%). This inherently defensive tactic typically lends itself to outperformance in down and volatile markets and keeps sector weights from drifting too far from the benchmark.

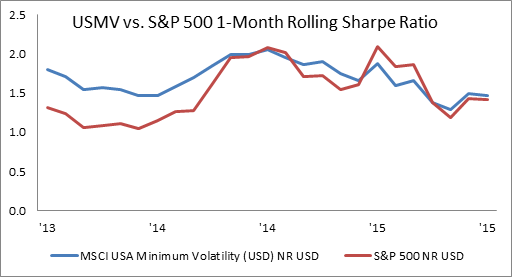

Quantifying the Volatility Reduction

When it comes to quantifying the amount of return generated per unit of risk in a portfolio, utilizing the Sharpe Ratio can provide an “apples to apples” approach. For example, comparing the MSCI USA Minimum Volatility Index (the underlying index of USMV) to the S&P 500 on a year-to-date, 1-, 3-, 5-, and 10-year basis through November 30, 2015 shows meaningful annualized outperformance in all periods, with considerably less risk. This phenomenon carries through to developed international markets and emerging markets alike. Additionally, in all three geographic segments, the minimum volatility approach generates more incremental return per unit of risk (higher Sharpe Ratio), but does so with greater return AND less risk (lower standard deviation), resulting in a superior Sharpe Ratio (shown below). Furthermore, to eliminate period specific results, we examined the rolling period returns, which largely confirm our findings. It should be noted that by design minimum volatility ETFs may lag in bull markets, but should outperform in highly volatile or down markets.

{kind=link}