Currently, fixed income investors are more cautious toward credit risk than they were in 2015, especially among the more speculative segments of the market. How do we know? Yield spreads show the amount of compensation investors require to justify holding a risky security.

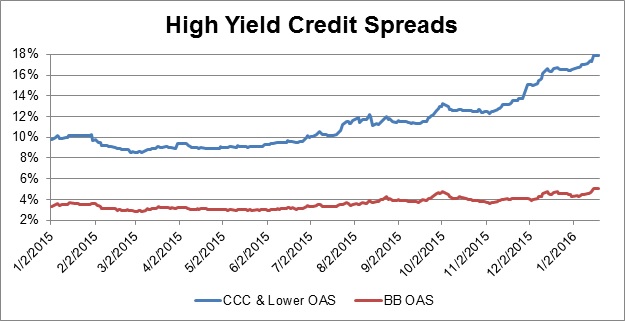

As the first chart shows, option-adjusted spreads (or “OAS”) of issuers rated BB moved from 3.36% at the beginning of 2015 to 5.02% a year later, a change of 166 basis points. Meanwhile, the lower quality issuers (rated CCC and below) rose by nearly five times that amount, from 9.74% to 17.91%. In other words, investors became much more pessimistic about the most speculative areas of the corporate credit market.

{kind=link}

The investment-grade bond market travelled a similar path. Spreads of corporate names rated AA widened by 20 basis points (0.85% to 1.05%) while BBB names moved by 67 basis points (1.99% to 2.66%). Again, the lower quality names widened more than the higher quality names by a wide margin.

The trend in 2015 and so far in 2016 has been clear: for each step down in credit quality investors demanded increasingly higher compensation.

{kind=link}

For those of us who follow the markets closely, this dynamic is typical of the late stages of a credit cycle after fundamentals have peaked and begin declining. There’s plenty of evidence to support this view. In 2015 the par value of corporate issuance was the highest on record. Many companies issued debt to fund stock buybacks. S&P 500 earnings have been declining, quarter-over-quarter. There has also been a pick-up in mergers and acquisitions as corporate managers look to add shareholder value. This combination of factors has undoubtedly created huge concern for bond holders.

In our view, fixed income investors will need to be increasingly selective in 2016. That means choosing more carefully which issuers, sectors, maturities and credit qualities they own. We believe there’s still opportunity to earn decent returns and income. This is certainly true if credit spreads stabilize in 2016, and may even be the case if spreads continue to widen.

Anthony Parish is the Vice President of Portfolio Strategy & Research at Sage Advisory, a participant in the ETF Strategist Channel.