After a prolonged slumber, market volatility returned to the financial markets with a vengeance in late August. Many concluded that a slowing Chinese economy combined with the then-still-imminent prospect of a Federal Reserve rate hike had sent stocks on their wild ride.

My Uncommon Sense view—where I challenge a prevailing consensus driving the market—is that there is something much bigger wreaking havoc on the capital markets than worries over China’s economic growth and a Federal Reserve (Fed) rate hike.

While there have been about 700 rate cuts by global central banks since the last Fed rate hike in 2006, investors are now starting to concede that monetary policy alone isn’t enough to stoke inflation, solve the world’s debt problems and return economic growth to historical norms.1

There is a growing realization that public and private sector reforms are needed in conjunction with sound monetary policy to boost inflation and get back to more normal rates of growth, and investors are starting to grasp that this path to economic recovery will be a long, bumpy one. I believe this is the true cause of those August squalls.

The real story in China

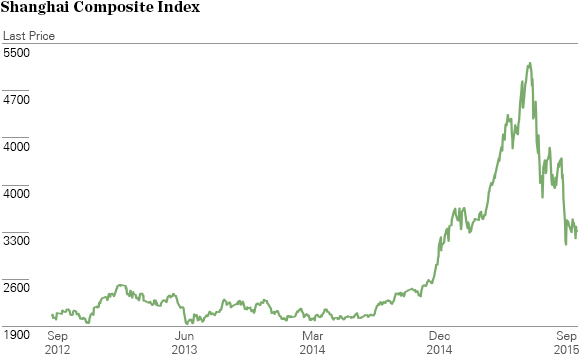

China was the scapegoat for the August sell-off and subsequent market volatility, yet I would argue that the situation is more nuanced.

{kind=link}

Source: Bloomberg, State Street Global Advisors. Period: 9/18/2012 to 9/18/2015. Past performance is not a guarantee of future results. Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss, and the reinvestment of dividends and other income.

The measures taken by the Chinese government during the last year couldn’t have been more aggressive, and yet they have failed to slow declining economic growth. Now China is spending huge sums to prop up the stock market and influence the value of the renminbi.2At this point, China will likely have to spend even more, but that doesn’t alleviate the fact that there’s less and less evidence it will actually work.

It’s widely believed that the current challenge for the Chinese government is to build an economy that relies less on exports and more on consumer demand and services. This shift from an investment-driven export economy to a consumption-driven service economy may take years, and investors are waking up to the fact that China’s transition will be rocky.