The headline story in oil is that it settled at its highest level of the year. Prices got a boost from a weaker U.S. dollar and there is an expectation in the market that weekly data will show a decline in U.S. crude inventories. The next story is that energy stocks rallied on higher oil, but historical data shows that energy stocks may not be the best bet to play an oil rally.

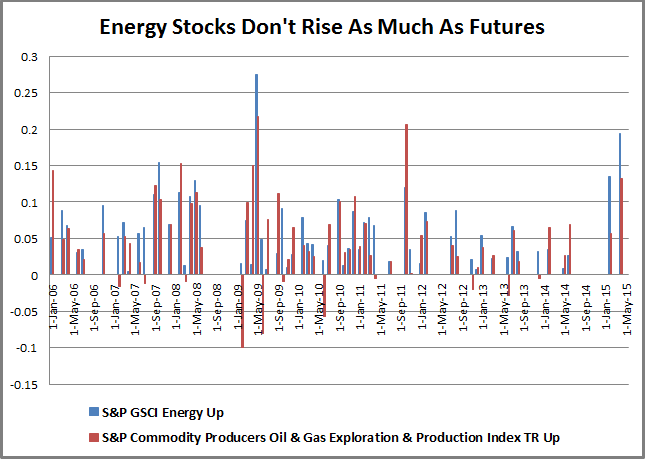

Of course, energy futures and oil and gas producing stocks, are related as evident in the chart below, but it may not be as much as expected. The correlation is 0.79 between the S&P GSCI Energy and S&P Commodity Producers Oil & Gas Exploration & Production Index TR, using monthly data from Dec 30, 2005 – May 29, 2015. There are influences on stocks of producers that may not be related to the oil price but aim to maximize shareholder value. For example, decisions on dividends, debt/equity ratios or even hedging out the price of oil may drive the stock price independently from the underlying oil price. Source: S&P Dow Jones Indices

The annualized volatility of the stocks of producers is basically the same as the futures at 28% versus 29% but for every 1% move in oil futures (up or down), the stocks only move 74 basis points as measured by beta. What is more interesting to study is how oil stocks perform versus oil futures in up and down markets. On average in a down month for oil, futures drop 6.8% versus only 4.9% for the stocks; however, when oil rises, futures rise 6.1% on average in a month but stocks only rise 4.9%.

The bottom line is if oil is dropping, stocks may be the safer way to play, but when oil is rising, it might be time to switch to futures.

This article was written by Jodie Gunzberg, global head of commodities, S&P Down Jones Indices.

© S&P Dow Jones Indices LLC 2013. Indexology® is a trademark of S&P Dow Jones Indices LLC (SPDJI). S&P® is a trademark of Standard & Poor’s Financial Services LLC and Dow Jones® is a trademark of Dow Jones Trademark Holdings LLC, and those marks have been licensed to SPDJI. This material is reproduced with the prior written consent of SPDJI. For more information on SPDJI, visit http://www.spdji.com