Over the past three years, the standard deviation for the Russell 2000 Low Volatility Index was nearly 300 basis points lower than that of its traditional counterpart, according to Russell data. Over the past year, the low volatility index’s Sharpe Ratio was 1.6 compared to 1.2 for the Russell 2000.

SMLV allocates 46.5% of its weight to the financial services sector. Industrial and utilities stocks each command more than 13% of the ETF’s weight.

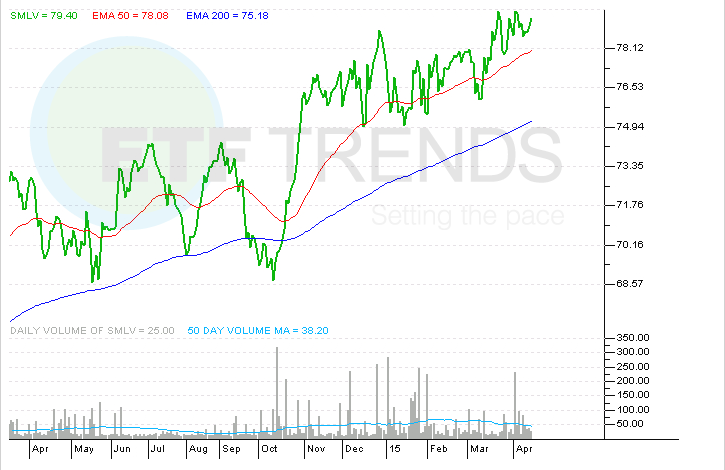

SPDR Russell 2000 Low Volatility ETF

{kind=link}

Tom Lydon’s clients own shares of IWM.