One way of looking at the importance of Exxon and Chevron maintaining their dividend increase streaks is this: Sure, dividend cuts are bad, but in the case of these companies, not extending lengthy dividend increase streaks could garner the same treatment from Wall Street as an outright cut. Put simply, the message, for now theoretical, from Exxon and/or Chevron not maintaining payout increase streaks is bad and that is not up for debate. [Energy ETFs Still Have Firm Dividends]

With Freeport, only three S&P 500 members have cut dividends this year. The other two are oil services firms Ensco (NYSE: ESV) and Diamond Offshore (NYSE: DO). Those stocks are down an average of 29% this year.

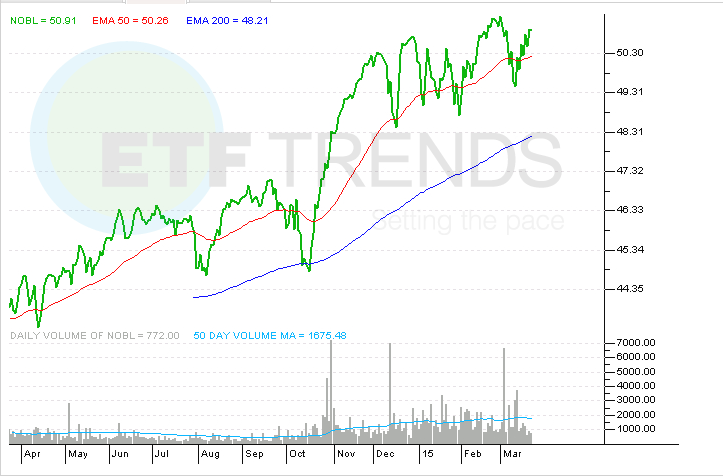

If Exxon and Chevron do not raise their dividends this year, the stocks will be expelled from several large dividend ETFs that use payout increase as part of the funds’ stock selection criteria. For example, NOBL has over $700 million in assets under management.

Exxon and Chevron combine for nearly 7% of the $356 million PowerShares Dividend Achievers Portfolio (NYSEArca: PFM), an ETF that requires dividend increase streaks of at least 10 years. Like PFM, theVanguard Dividend Appreciation ETF (NYSEArca: VIG), the largest U.S. dividend ETF with $21.2 billion in assets as of the end of February, requires 10-year dividend increase streaks for admission. Exxon was VIG’s seventh-largest holding at a weight of 3.3% as of Feb. 28. [Different Dividend ETF Strategies]

ProShares S&P 500 Aristocrats ETF

{kind=link}