e into the global market. Despite the relative cheapness of U.S. gasoline to the international markets from the fundamentals, the transportability has allowed benchmarks to measure the global seasonality.

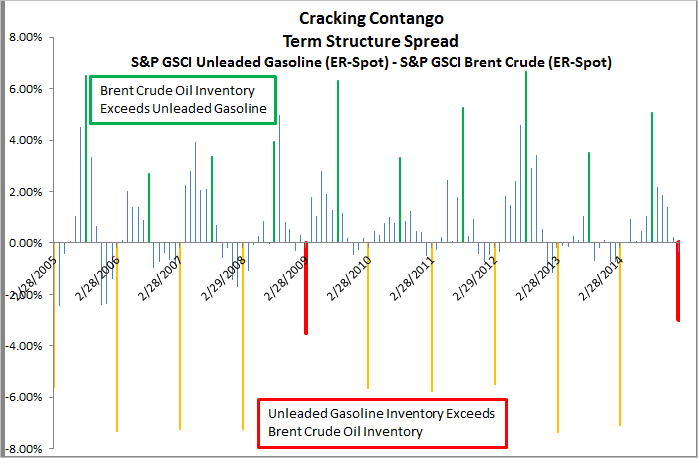

In indexing, the difference in roll yields can be measured to theoretically reflect the relationship between excess and shortage in the oil and gas markets since it is the storage markets that drive the shape of the curves. There is a historically wide roll spread between unleaded gasoline and brent crude oil, seasonally in each February, where the excess inventory of unleaded gasoline markedly exceeds the excess inventory of brent. What is interesting so far this February is that the spread is the narrowest in six years.

According to the IEA (International Energy Agency), global refining capacity is expected to rise after falling to a six-year low and that global refinery margins will come under renewed pressure. They predict further consolidation in the refining industry, especially in Europe and developed Asia as product markets continue to expand and globalise.

While the excess inventory of brent crude oil is larger at this time than in last February, when brent showed a shortage with a positive roll yield, the excess inventory of unleaded gasoline shown by the roll yield of -3.3% is down half from last year and is seasonally very low. This is illustrated in the graph below: