“The value factor was one of the first isolated in the original Fama and French asset pricing model, which corroborated the previously observed strong and positive relationship between low price-to-book stocks and returns. The authors argue that this value effect stems from the stocks’ capture of cross-sectional variation in returns that is related to relative distress,” according to a paper published in September on strategic beta advantages written by J.P. Morgan Asset Management’s Head of ETF Strategy and Business Development Ogden Hammond.

JPIN comes to market in the midst of a strategic beta boom. As of late August, assets under managements across smart beta ETFs totaled $350 billion, a 30% year-over-year increase. Much of that growth has been driven by institutional investors, including large money managers, endowments and pensions. [Institutions Flock to Smart Beta ETFs]

“Assets flowing into strategic beta ETFs have exploded in recent years, and the growth shows no sign of abating. Out of the approximately $1.7 trillion of assets in all exchange-traded products (ETPs),there were 342 strategic beta ETFs, with collective assets under management of about $291 billion, or 18% of that total,” Hammond’s paper noted, citing Morningstar data.

Financial advisors who are interested in learning more about strategic-beta or smart-beta ETFs can register for the Tuesday, November 11 webcast here.

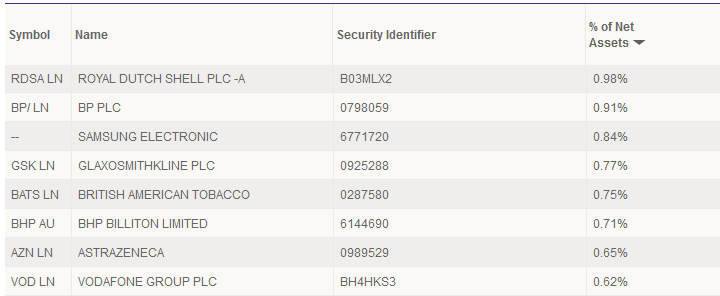

JPIN Top Holdings

{kind=link}

Table Courtesy: J.P. Morgan