Currency hedged ETFs are not perfect. No issuer has made that claim and there have been examples of some of these trailing their unhedged peers. That was seen earlier this when the British pound was strong while a stubbornly strong Korean won, at least until recently, has crimped the WisdomTree Korea Hedged Equity Fund (NasdaqGM: DXKW) and the Deutsche X-trackers MSCI South Korea Hedged Equity Fund (NSYEArca: DBKO). [Strong Won a Problem for Some South Korea ETFs]

“Investors with a view of the U.S. dollar relative to foreign currencies should ensure that their foreign market investments reflect their currency outlooks, either by being hedged or unhedged as the case may be. On a total return basis, currency-hedged investments should outperform corresponding unhedged investments during periods when the U.S. dollar is strong. Conversely, when the U.S. dollar weakens, currency-hedged investments generally underperform,” according to DAWM research.

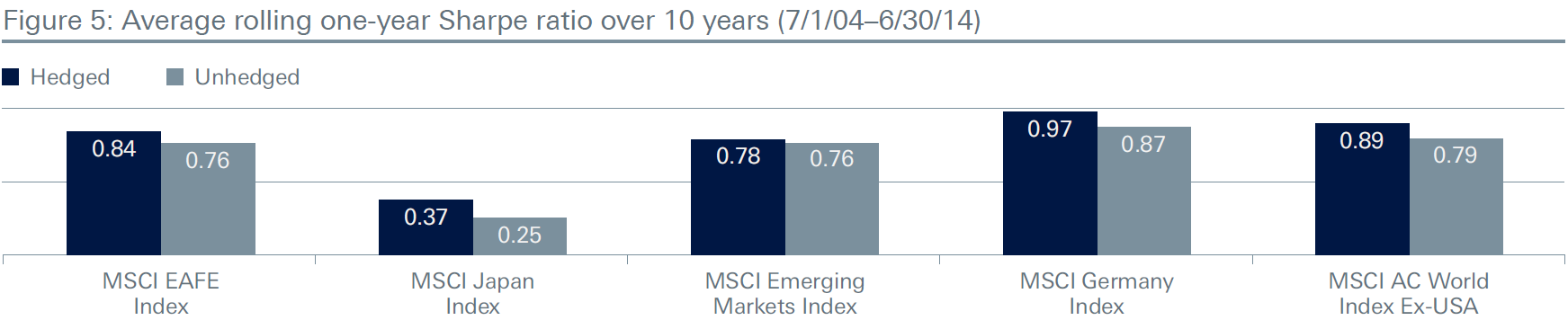

Often overlooked in the discussion about the effect currency fluctuations have on a portfolio’s returns is the volatility those currency gyrations subject investors to. Currency hedged ETFs help ameliorate that situation as well.

Over the 10 years ending in the second quarter of 2014, the hedged equivalents of the MSCI EAFE, MSCI Germany, MSCI Emerging Markets and MSCI All-County World indices were less volatile than their unhedged counterparts, according to DAWM data. Adding the MSCI’s hedged Japan index to that group, all five had higher rolling one-year Sharpe ratios than the unhedged indices for the 10 years ending June 30, 2014.

{kind=link}

Table Courtesy: Deutsche Asset & Wealth Management

Tom Lydon’s clients own shares of EFA.