With the volume of news headlines and the speed of information, tid bits of news, some with the potential to be significant, can naturally get lost in the shuffle. One such issue that might have some significance in the coming weeks is the president of the St. Louis Federal Reserve, James Bullard saying that there is evidence of inflation “moving higher”. This statement shows a change in Bullard’s view point. In the past, he has shown concern over the low levels of inflation and recently has commented on the stability of the inflation rate. As of April 30, the level of annual inflation is 2%.

The Consumer Price Index (CPI) is a widely recognized price measure used in the U.S. to track the price of a market basket of goods and services purchased by individuals. The weights of the components are based on consumer spending patterns. The next release of the CPI will be June 17 and the market’s survey is calling for a month-over-month value of 0.2%. The CPI value has been trending higher since February’s 0.10% as March and April were 0.2% and 0.26%, respectively.

Rising inflation expectations resulting from comments in the news and recent CPI results can be attibuted to the performance of Treasury Inflation Protections Securities (TIPS). The S&P U.S. TIPS Index, a broad, comprehensive, market value-weighted index seeks to measure the performance of the U.S. TIPS market. Year-to-date, the index is returning 5.37%. Longer maturity indices such as the S&P 15+ Year U.S. Treasury TIPS Index returned 16.64% (see table).

The last TIPS auction was May 28 an $13 billion of a reopened 10-year TIPS was issued. The initial market reaction to the auction was positive. Since May 28, the return of the 10-year TIPS has been +0.62% as measured by the S&P 10 Year U.S. TIPS Index. The next auction for 30-year TIPS will be on June 19th, a reopening of the existing 29-year, 8-month 1.375% of Feb. 2044, and the amount offered will be $7 billion.

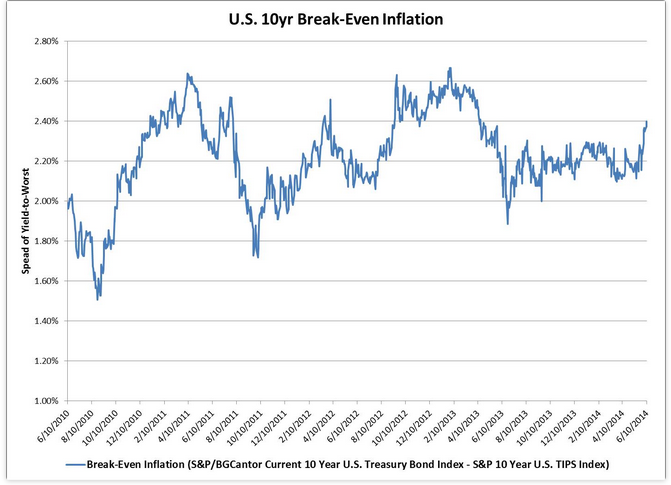

Break-even inflation is the difference between the nominal yield on a fixed-rate investment and the real yield on an inflation-linked investment of similar maturity and credit quality. If inflation averages more than the break-even, the inflation-linked investment will outperform the fixed-rate. Conversely, if inflation averages below the break-even, the fixed-rate will outperform the inflation-linked. Presently the break-even inflation of the 10-year TIPS is at 2.40%. This means that if inflation averages more than 2.40% over the next 10 years, TIPS will outperform a traditional Treasury. Time will tell if the rate at which inflation is rising in the U.S. could become a problem for the Federal Reserve or investors.

{kind=link}

This article was written by Kevin Horan, director fixed income indices, S&P Dow Jones Indices.