As alternatively weighted, intelligently indexed or smart beta exchange traded funds have grown in prominence, so has the unfortunate notion that users of exchange traded funds must choose sides: Market capitalization weighting or smart beta.

“There seem to be two camps, one singing its praises and highlighting growing investor demand. The other side points out that not all of these strategies are the same and thus they should not be grouped together,” said S&P Capital IQ in a new research note.

Advisors and investors need not pick sides because it is possible and potentially rewarding to combine cap-weighted and smart beta strategies within the same portfolios. Some ETF strategists are already doing just that. [Cap Weighted, Smart Beta ETFs Can Work Together]

The growth alternatively weighted ETFs has been stunning. In the 12 months ending March 2014, smart ETFs hauled in a quarter of ETF inflows while representing just 10% of the available funds on the market, said S&P Capital, citing PowerShares.

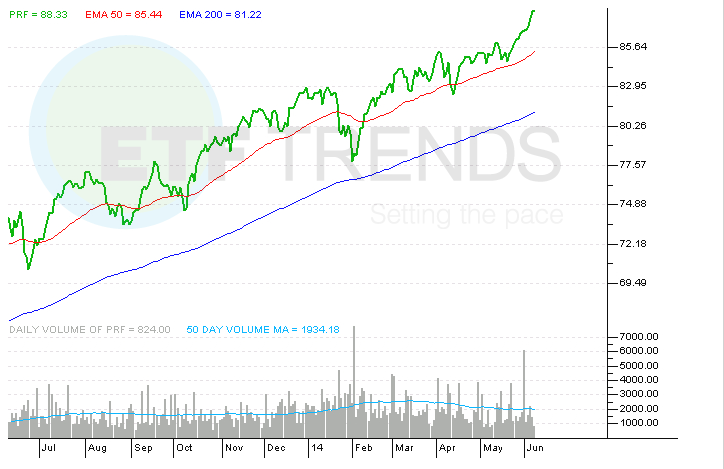

PowerShares is the fourth-largest U.S. ETF sponsor and one of the largest issuers of smart beta funds. One of the firm’s largest smart offerings is the PowerShares FTSE RAFI US 1000 Portfolio (NYSEArca: PRF).

PRF, which turns nine years old later this year, has $3.5 billion in assets under management. Rated overweight by S&P Capital IQ, PRF holds more than 1,000 stocks, leading to comparisons against traditional broad market ETFs and the assertion that small-caps drive PRF’s returns. In reality, less than 5% of PRF’s weight is allocated to small-caps, according to PowerShares data.

Since the March 2009 market bottom, PRF has returned almost 297% compared to an average gain of 227.5% for the S&P 500 and the Vanguard Total Stock Market ETF (NYSEArca: VTI). PRF has only been modestly more volatile than VTI and the S&P 500 over that time. [How Smart Beta ETFs Compare to Traditional Benchmarks]

“Alternatively weighted ETFs are constructed differently from market-cap weighted ones. Constituents are selected by the index provider based on certain rules, which can include a variety of fundamental or valuation factors, or they can hold the same stocks as market-cap weighted ones. These ETFs tend to be rebalanced on a periodic basis, often leading to a higher expense ratio than the larger market-cap weighted products. In our opinion, the higher costs are sometimes worth it and in other cases there are better ETF choices,” said S&P Capital IQ.

Among institutional decision makers, 53% expect to increase smart-beta ETF allocations over the next three years while 46% of non-users play to explore the idea of smart-beta ETFs in their portfolios. Financial advisors have a similar mindset with nearly two-thirds planning to increase their smart beta allocations this, according to a recent survey by ETF Trends and RIA Database. [Institutional Investors Warming to Smart Beta ETFs]

Other smart beta offerings from PowerShares include the PowerShares International Dividend Achievers Portfolio (NYSEArca: PID). The $1.2 billion ETF, which has a trailing 12-month yield of 3.3%, is rated marketweight by S&P Capital IQ.

Important to the investor that wants to maintain some U.S. exposure, U.S. stocks are PID’s largest country weight at nearly 30%. While the ETF surprisingly features no exposure to Australia, one of the highest-yielding developed markets, the fund’s other international weights indicate it has legitimate dividend growth potential.

For example, the U.K, is PID’s third-largest country weight. “British listed companies paid $102. 1 billion in dividends last year, and since 2009 have paid roughly $441 billion,” according to the Independent. [A High Achieving Global Dividend ETF]

PowerShares FTSE RAFI US 1000 Portfolio

{kind=link}