If finance were high fashion, ‘smart beta ETFs’ would be the showcase of this year’s Spring collection. They are receiving a lot of press attention and surveys of institutional investors show that they plan to increase their adoption of smart beta ETFs. In this article, we answer the question: What specifically are smart beta ETFs and what assets have they gathered to date? Looking beyond the label is very important to both retail and institutional investors.

To do this, we first need to define ‘traditional’ beta ETFs. In its purest form, an ETF providing ‘traditional beta’ exposure is one that tracks a market capitalization weighted broad market index. So if this is traditional ‘beta’, then what is a ‘smart beta’ ETF?

A theoretician may define it as an ETF providing index-based exposure to any investment risk factor other than broad market risk. By this narrow yardstick, even an ETF that tracks the S&P Small Cap 600 could be considered ‘smart beta’ since it provides targeted exposure to the ‘size’ risk factor. Taking this definition very literally, even an ETF that tracks the S&P 500 wouldn’t be ‘pure’ beta exposure, since the S&P 500 screens stocks for profitability prior to inclusion.

We are more interested in the practitioner’s definition of ‘smart beta’. Here is a working definition of a smart beta ETF:

An ETF that tracks a rules based index providing exposure to a specific investment risk factor other than market cap weighted size, style (growth/value) or industry sectors.

We can break down this definition into its key components:

Index based: This eliminates ‘active’ ETFs i.e. those that don’t track an index. Essentially ‘smart beta’ ETFs are ‘index-izing’ what may earlier have been marketed as an active strategy. As I argued 2 years ago on Seeking Alpha, this represents a blurring of the distinction between traditional ‘passive’ and ‘active’ investing.

Specific risk factor: These ETFs should give you access to a targeted, definable risk factor or strategy such as low volatility, momentum etc. We exclude quantitative strategy ETFs even if they are index based, if the targeted risk factor or strategy is not tightly defined.

Excluding cap weighted size, style and sectors: This is clearly a judgment call, but a useful and important one. The practice of index based investing in market cap weighted size (e.g. small cap), style (e.g. value) and industry sectors has been well established for several years. Through the term ‘smart beta’ we are trying to identify those strategies that investors did not have access to via low cost, index-based products till recently. We also exclude inverse & leveraged ETFs.

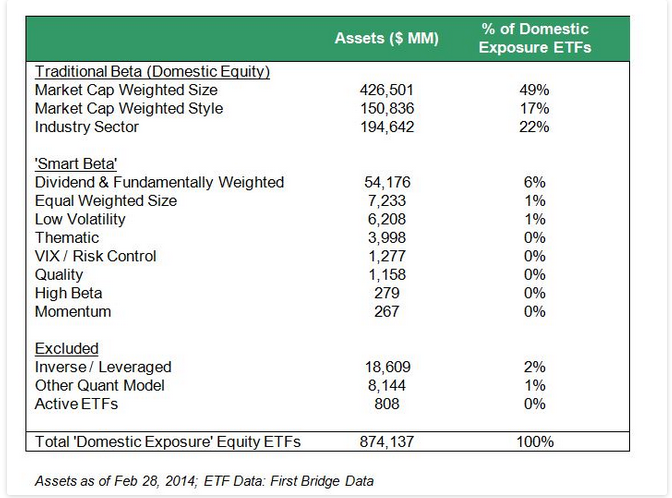

The table below shows the assets for US listed ETFs that provide domestic US equity exposure. It shows the breakdown of assets into ‘traditional beta’, ‘smart beta’ and ‘other’ categories based on our definition above. The ETF Data (ETF classifications and assets) is from the First Bridge ETF database.

{kind=link}