What has some concerned about further upside for health care stocks and ETFs is the aforementioned frothy valuations for the biotech sub-sector. Some may even be focusing on the fact that IBB has been one of the 10 best non-leveraged ETFs of any type for three consecutive years, reasoning that the largest biotech fund needs to run out of steam at some point. [One Biotech ETF Standout]

There is no denying that biotech stocks are expensive, but consider this: The combined P/E ratios of Biogen (NasdaqGM: BIIB), Amgen (NasdaqGM: AMGN), Gilead (NasdaqGM: GILD), Celgene (Nasdaq: CELG) and Regeneron (NasdaqGM: REGN) – roughly 37% of the Nasdaq Biotechnology Index’s weight – is nearly 239.

Said another way, the combined P/E of those stocks is barely above that of Netflix (NasdaqGM: NFLX) and not even half that of Amazon (NasdaqGM: AMZN). Amazon trades at over 84 times forward earnings, or nearly double Regeneron’s forward P/E.

No, the comparison of biotech to consumer discretionary stocks is not apples-to-apples. And yes, biotech is expensive, but maybe, just maybe the premium is justified. Perhaps it is trite to say, but Amazon and Netflix are developed world indulgences while the holdings in biotech ETFs are attempting to make products that improve and save lives.

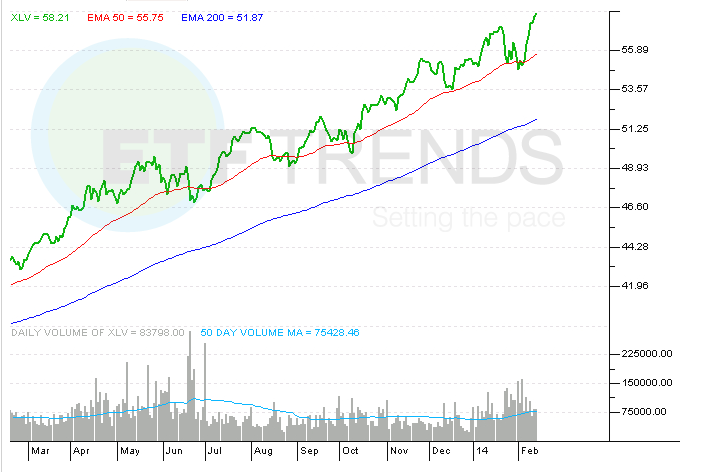

That might be an inconvenient truth to some, but it could also explain why Amazon’s 95.8% two-year gain looks paltry compared to the 116.3% gained by IBB over the same period. That is not some crazy, one-off example, either. Over the past three years, XLV is up almost 91% while the NASDAQ 100 is up about 59%. [Health Care Delivering as Other Sectors Lag]

Health Care Select Sector SPDR Fund

{kind=link}