Sentiment regarding emerging markets, and resources-based assets, has been improving for several reasons. For one thing, both China and Europe may be turning a bit of a corner; economic data from both regions have improved; economic downturns are either stabilizing and/or demonstrating legitimate signs of expansion. This gives many of the exporters of basic materials and natural resources, companies as well as countries, a reason to be optimistic. Secondly, the Federal Reserve is likely to be more deliberate, and perhaps more slow, about tapering its bond purchases. This may give emergers a bit of wiggle room with respect to a global environment that is more stimulus-friendly. Finally, fund flows in September did not merely go into broad market U.S. assets; developed Europe-Asia, undeveloped emergers as well as resource-heavy investments began to see significant ETF inflows as well.

Not surprisingly, then, even the U.S. SPDR Select Sector Basic Materials Fund (XLB) demonstrated enormous Q3 resilience. It was the best performing sector ETF in the SPDR Select Sector series from 7/1-9/30 with a pick-up of 9.5%. Some have suggested that the results demonstrate a return to fundamental value as opposed to momentum alone.

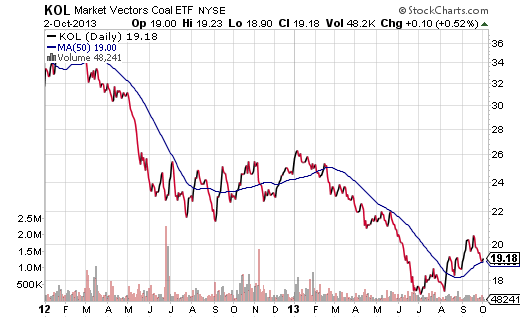

From a relative strength standpoint, I have more confidence in Natural Gas (FCG) to carry on its momentum. From a valuation standpoint, Coal (KOL) may prove to be an exceptional bargain. Coal has been so unloved for so long, the July lows may have ushered in a new season for producers of the globally used resource.

{kind=link}

Gary Gordon is president of Pacific Park Financial, Inc.