Gold and silver prices rally on the weak US data and dollar. Gold and silver prices continued to recover last week on the back of the delayed release of the September US unemployment report and on-going USD weakness.

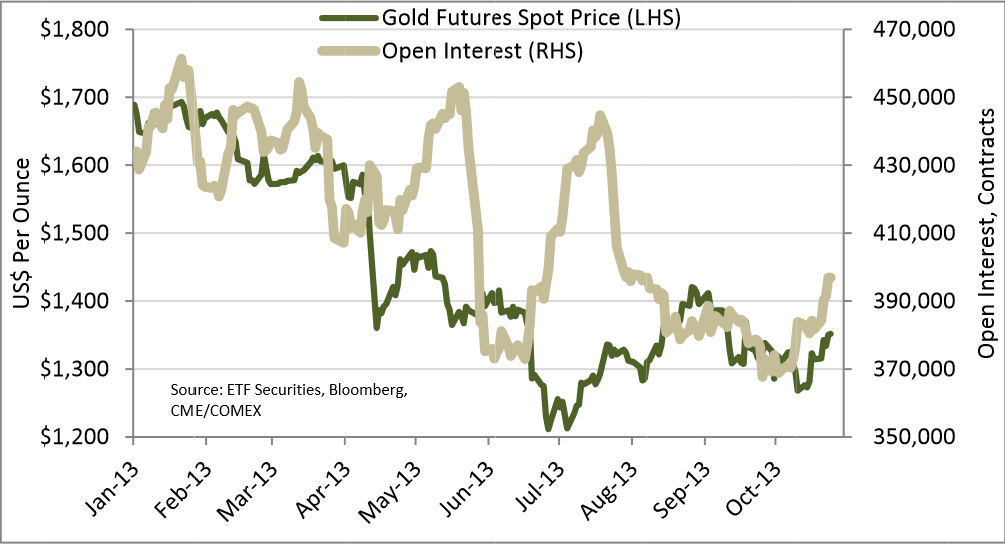

It is the third successive weaker-than-expected report, further deferring expectations of tapering of the US bond buying program. Alongside encouraging European economic data the EUR/USD rate reached $1.38, the highest level since November of 2011. Gold futures open interest was increased about 4% since mid-October (8% since Sept.), indicating investors have instigated new long positions (see chart below), adding bullish momentum. Last week LBMA gold forward rates remained negative and the front COMEX gold futures flirted with backwardation, highlighting the physical gold demand remain strong. We remain constructive gold, encouraged by the recovery above US$1,300 as the market appears to be on a solid footing, back stopped by signs of a re-emergence of physical demand. The risk for gold and silver is USD strength following the FOMC meeting this week.

Gold is shining in the US government shutdown post-mortem. Since US lawmakers announced the agreement to end the partial government shutdown and raise the debt ceiling on October 16th, the price of gold ahs increased 5.4%, outperforming most other asset classes. The Euro has increased 2.0% vs the US dollar, US 10yr yields have dropped 22bsp and the S&P 500 has gained 3.6% to reach new highs (from the Oct. 15 marks). Gold has performed strongly, as it seems clear the fact the US debt issue has only postponed, and central bank stimulus is likely to be required for a prolonged period. Such concerns appear to be accelerating central banks’ and private investors’ search for alternatives to the US dollar as a reserve asset, with gold one of the few viable alternatives.

Platinum and palladium remain attractive as global economic prospects improve. Platinum and palladium consolidated recent gains last week as much of the attention remained on recovering gold prices. Although the US may be entering a bit of a self-inflicted economic blip, global vehicle sales are likely to continue to improve with an added boost from the recovery in Europe. The chart on the following page shows the strong relationship between the EUR/USD rate and platinum since 2010. Due to a substantial increase in platinum jewelry demand from China during the European recession, a recovery in European auto catalyst platinum demand would likely further shift the supply demand imbalance in the platinum market toward a greater deficit.

Key events to watch this week. The US FOMC announcement is likely to be a highlight as analysts will be seeking to quantify how sever the US debt related standoff slowdown is perceived by the Fed. It is the beginning of a new month so the data docket will be full, notably with global PMI’s.

{kind=link}