Early signs markets starting to take default risk seriously. The gold price fell last week despite the US government shutdown, a weaker dollar, and generally weaker than expected US economic data, indicating that short term investors continue to engage in “buy the rumor, sell the fact” gold trading activity.

Silver was the precious metals stalwart, gaining 0.2% as investor flows favoured this beaten-down hybrid metal over gold. The Golden Week holiday in China likely kept the world’s largest consumer of gold away from the market, adding pressure on prices. The market calm is unlikely to last long in our view. Toward the end of last week there were tentative signs of increasing market impatience with the lack of progress, including continued selling of the US dollar and buying of perceived safe haven currencies such as the Japanese yen and Swiss franc. The cavalier attitude being taken by politicians about fiscal matters is leading to growing doubts about the ability of US politicians to come to a compromise that will avoid a sovereign default. With the debt limit likely to be breached around 17th October, markets are likely to remain volatile and short term news driven over the next few weeks. If progress on debt negotiations maintains the current stalemate much longer, gold is likely to move back into the spotlight.

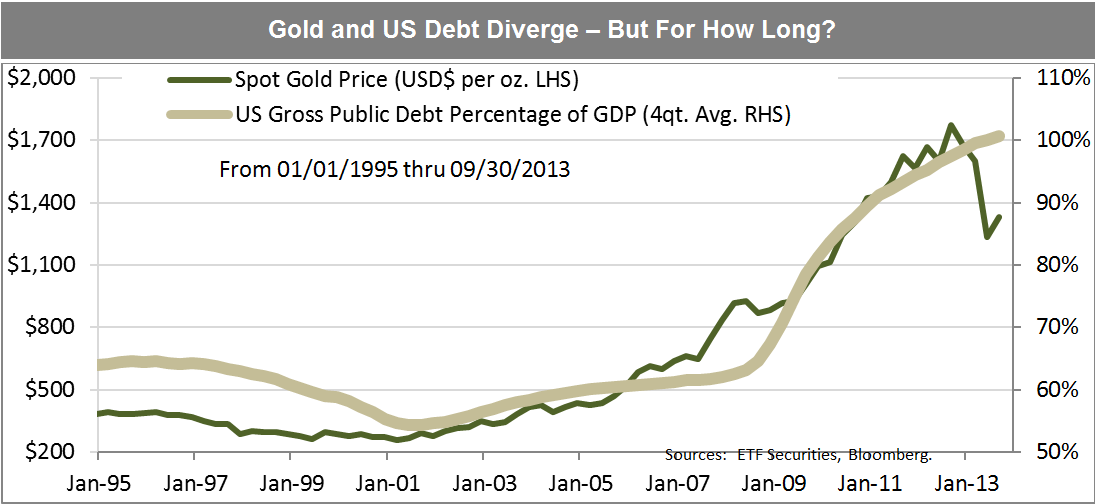

Gold likely to move back into the spotlight. Below the political maneuvering, it has to be remembered that the underlying cause of the current US government shutdown is that the US has too much debt and insufficient revenues to match spending. In our view, targeting moderate to high inflation is the likely long-term route the US and other major indebted developed economies will have to take in order to control rising real debt burdens. In the immediate term, the next hurdle is getting the debt ceiling raised in order to prevent a US debt default. Political misjudgement on this issue would likely not just severely damage the US economy and the longer term faith in the US government’s commitment to repaying its debt, but also would likely have large negative reverberations across global financial markets and economies. With the price of gold down about 22% this year and trading near its all-in cost of production, and the S&P 500 up nearly 19% and near its all-time high, some asset reallocation into gold as a hedge against worst case debt scenarios and inflation temptations may be prudent.

Platinum and palladium suffer as investors start to reduce risk positions. Despite strong auto sales figures in the US, Japan and the UK, and continued labor issues in South Africa, platinum and palladium prices declined last week. While underlying fundamentals remain highly price supportive in our view, with both metals in large supply deficit, both metals tend to be sensitive to overall market risk sentiment. With the US fiscal and debt negotiations becoming almost farcical, as highlighted above, there are early signs markets are starting to become concerned. Cyclical asset prices such as those of platinum and palladium will remain vulnerable if these fears escalate. However, assuming the US Congress eventually comes to its senses and backs off before a default occurs, any sell-off of platinum and palladium presents a good potential long-term buying opportunity in our view.

{kind=link}