• “High Dividend Yield Years”: Years in which the starting trailing 12-month dividend yield was above the median trailing 12-month dividend yield for the MSCI EM. The median trailing 12-month dividend yield was 2.25%.

• “Low Dividend Yield Years”: Years in which the starting trailing 12-month dividend yield was below the median trailing 12-month dividend yield for the MSCI EM.

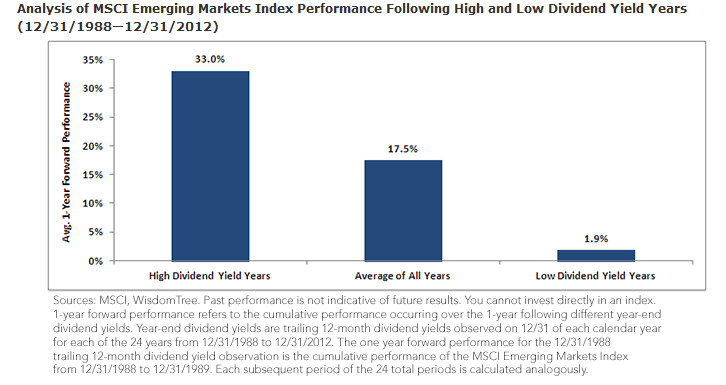

Performance: Where the Rubber Meets the Road

We think the figure below paints a clear picture of the differences in returns between periods classified as High Dividend Yield Years and those classified as Low Dividend Yield Years.

{kind=link}

• Squarely in the High Dividend Yield Year Range: As of July 31, 2013, the MSCI EM exhibited a trailing 12-month dividend yield of 2.93%. There were five calendar years that started with a higher value, and each was associated with a positive subsequent return. While this past performance cannot guarantee any particular future return, we do believe that 2.93% is a strong potential valuation indicator relative to the performance history of the MSCI EM.

• Big Dispersion from High to Low: We’ve certainly pointed to this analysis before, and we’ll bring it up again and again to emphasize its importance. The three bars in this figure make the statement that valuation is of paramount importance for the MSCI EM. On average, returns of the High Dividend Yield Years eclipsed those of the Low Dividend Yield Years by over 30%.

Conclusion

While the dividend yield analysis is a strong and important indicator for the broader market, we also want to look at other factors. We will look at price-to-earnings (P/E) ratios and how they differ across emerging market sectors as well as countries. Additionally, we will close this series with two blog posts aimed at showing that all emerging market equity indexes are not created equal. Each index approach trades off certain attributes to focus on others. A critical question must be asked: If one believes emerging markets are inexpensive and represent a good opportunity, are you best positioned to capture the market’s upside? Many investors may not be, and we will try to provide a framework to understand the trade-offs made in various approaches to indexing.

Read the full research paper here.

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.