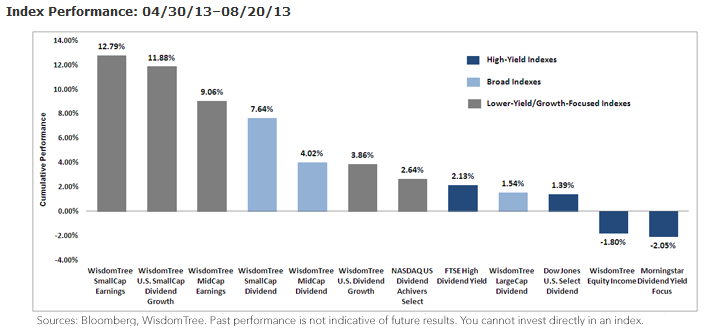

• High-Yield-Focused Indexes Outperformed through April – Over the first four months of 2013, as interest rates generally declined, the high-yield-focused indexes outperformed other broad and growth indexes shown above. The broad equity market, measured by the S&P 500 Index, was up 12.74%, which means that the yield-focused indexes also outperformed the broad market. Lower-yielding, growth-sensitive indexes lagged in the first four months of the year.

{kind=link}

• Since May 1, the performance situation reversed from the first four months of the year.

• High-Yield-Focused Indexes Have Underperformed since May 1 – Since interest rates began their climb, over the period displayed above, high-yield-focused indexes have underperformed other broad and growth indexes shown above. The broad equity market, measured by the S&P 500 Index, was up 4.19%, which means that the yield-focused indexes also underperformed the broad equity market. During this period, the 10-Year Treasury trended significantly higher.

• Morningstar Dividend Yield Focus Index – This index was the worst-performing of all indexes shown above, with a return of -2.05%, underperforming the S&P 500 by 6.23%, after being the best-performing index through April, a period during which it outperformed the S&P 500 by 5.15%.

A Look to Growth-Focused Indexes

The spike in interest rates in 2013 has caused a reevaluation of dividend-yield-focused indexes and the stocks with highest yields, but not all dividend-paying equities underperformed. Smaller-capitalization and dividend-growth indexes outperformed during the period associated with rising rates. Their outperformance might be a result of their higher growth expectations, which become more desirable with improving economic activity. The smaller-capitalization dividend stocks also have less exposure to some sectors of the market that many felt were becoming expensive. It is important to look to these diversified baskets of dividend-paying stocks for diversification and potential growth. In our market insight on this topic, we evaluate in more detail the underlying exposures that led to this performance divergence across the various equity indexes.

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.

1Source: Bloomberg (05/01/13–08/20/13).