Japanese stocks have soared since Shinzo Abe was elected prime minister based on the belief that his “Abenomics” policies will reinvigorate Japan. Abenomics focuses on a three-arrow policy of fiscal stimulus, monetary stimulus and structural reforms. All of Abenomics’ goals are aimed at one thing: promoting economic growth in Japan.

Weaker Yen Has Benefited Exporters’ Earnings

Thus far, the monetary stimulus has coincided with a weaker yen. A weaker yen ultimately helps large multinational companies that sell products overseas.

Products of these companies generally become more attractive to foreign buyers when the yen weakens.

Also, overseas sales converted back to a weak yen translate to more yen revenue, ultimately adding to the bottom line.

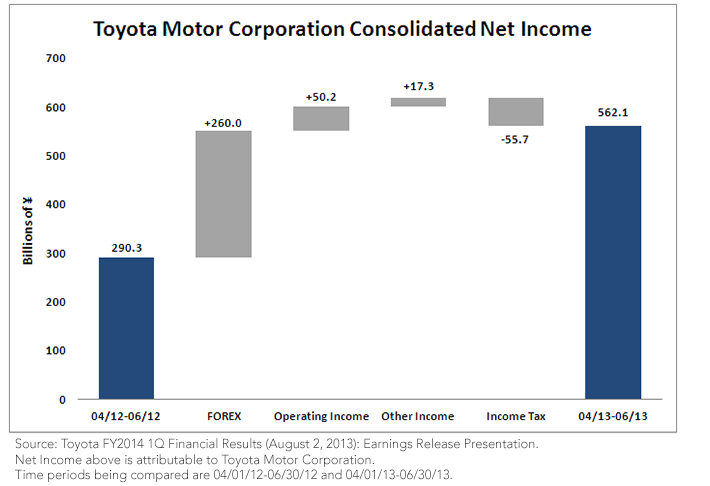

The chart below illustrates the positive effect a weaker yen has had on Toyota’s net income.

{kind=link}

• Yen Depreciation Dramatically Contributes to Earnings – The depreciation of the yen accounted for ¥260 billion of the ¥270.1 billion growth in net income over the same period last year. It is important to realize that Toyota’s gain from the yen depreciation is absolutely remarkable and represents over 95% of the total growth in net income for the period.

• Further Yen Depreciation Can Add to Future Profits – If the yen continues to depreciate, it could potentially continue to add to Toyota’s bottom line. Toyota is forecasting to sell 9.1 million vehicles over their 2014 fiscal year, and 6.8 million (approximately 75%) of those are expected to be sold outside Japan.1 These future overseas sales converted back to a potentially weaker yen translate to even more yen revenue.

• Toyota’s Stock Performance Also Strong – Market participants have recognized the benefit a weaker yen has had on Toyota’s bottom line. As of this writing (August 23), Toyota’s total return has been 94%, while the broader Tokyo Stock Price Index (TOPIX) for Japan is up 53%, over the past year. The yen is down 21% over this same period.2

Other Automakers Also Benefit from a Weaker Yen

Other large Japanese automakers have all benefited from a weakening yen due to their export-oriented business models. The list below shows the major automakers and the amount of reported income during their most recent earnings period compared to the same period of the preceding year.