{kind=link}

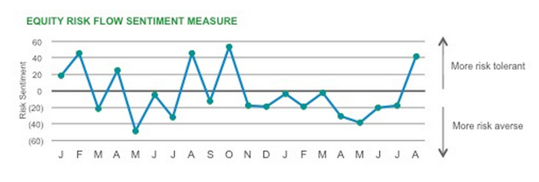

Because the Risk Sentiment Measure takes into account the risk profiles of securities within a category, it reflects shifts in risk appetite that are harder to discern from raw flow data. In other words, in August there were net outflows in less risky equity ETFs (e.g. broad-based, large cap funds like SPY) and net inflows in riskier equity ETFs (e.g. European equity funds).

The primary takeaway, as always, is that there’s usually more to the story than what high-level flows illustrate. It’s often necessary to look at both raw flow data and other information, like the BlackRock Risk Sentiment Measure, to get a more accurate picture of emerging investor trends.

In the case of August flows, investors appeared to be cautiously optimistic while also likely preparing for increased market volatility come September. With events like the highly-anticipated FOMC meeting, German elections, US debt ceiling negotiations and the escalating conflict in Syria, the only thing certain about September is all the uncertainty.

Dodd Kittsley, CFA, is the Head of Global ETP Market Trends Research for BlackRock.