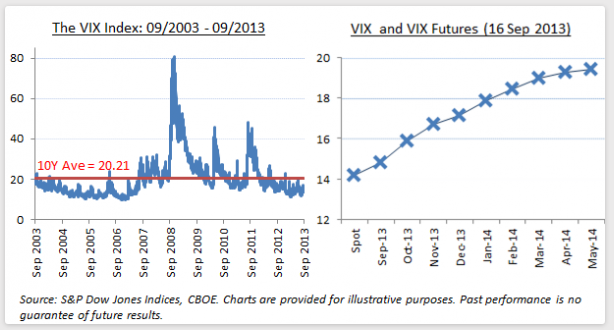

In the past few years – characterized by alternating risk-on, risk-off dynamics – the VIX has been a remarkably effective proxy for optimism or fear across multiple international markets. Five years on there is growing evidence that investors’ formerly incontinent risk appetite is becoming more discriminating. A case in point is provided by comparing U.S. and emerging market equities: the current correlation (0.56) is above levels prevalent prior to the crisis, but well below the majority of readings since.

But perhaps we are asking the wrong question. An errant correlation can always be found somewhere, then shoehorned into justifying a new era of market dynamics. Perhaps current low VIX levels are accurately reflecting a globalized and coordinated risk-on environment. After all, it is not difficult to find reasons to be cheerful. The extent of ‘tapering’ has arguably been largely discounted; a surprising Fed announcement would be highly uncharacteristic. The world’s advanced economies are recording concerted positive growth; the likelihood of a fully-fledged combat operation by NATO allies in Syria is receding at considerable pace. A Greek bailout, while politically awkward, is highly unlikely to shock a well-informed market. Even the much-battered rupee is showing signs of stabilization.

Such arguments provide little reason to demote the VIX Index from its privileged position as the primary indicator of global greed and fear. If the relative independence of EM and U.S. equities has indeed increased, it has done so because of a reduction in the perceived importance of systemic risk factors (in which case a “low” VIX is arguably justfied). And if systematic global risk should increase, the unparalleled systemic importance of the U.S. equity market will mean that the VIX is uniquely positioned to reflect the evolving impact of such risks.

{kind=link}