Should I own the broad TIPS market or short-term TIPS?

“It depends on what risks you are hedging against,” Wright-Casparius said. The broad TIPS market has a duration of around 8 years compared with 2.5 years for the short-term market (duration measures the sensitivity of bond prices to movements in interest rates). As with nominal bonds, reaching for maturity can provide a higher return over time, but with much more volatility than short-term bonds.

For those with long-term investment horizons, stocks and nominal bonds on average may earn returns high enough to overcome erosion in purchasing power due to inflation. A long-duration TIPS portfolio may be more appropriate for investors willing to incur more duration risk in the attempt to increase their long-term returns but who still want inflation protection in the form of inflation-indexed income. However, a short-term TIPS portfolio may be more appropriate for investors who wish their total portfolio to more closely track actual realized inflation over short horizons.

“If inflation and yields rise, short-term TIPS offer high correlation to inflation with less interest rate risk than longer-maturity TIPS,” Wright-Casparius said. “If you are near or in retirement or saving for a near-term liability, short-term TIPS may be a better choice than longer-dated TIPS; however, as with nominal bonds, there is a give-up in return over time.”

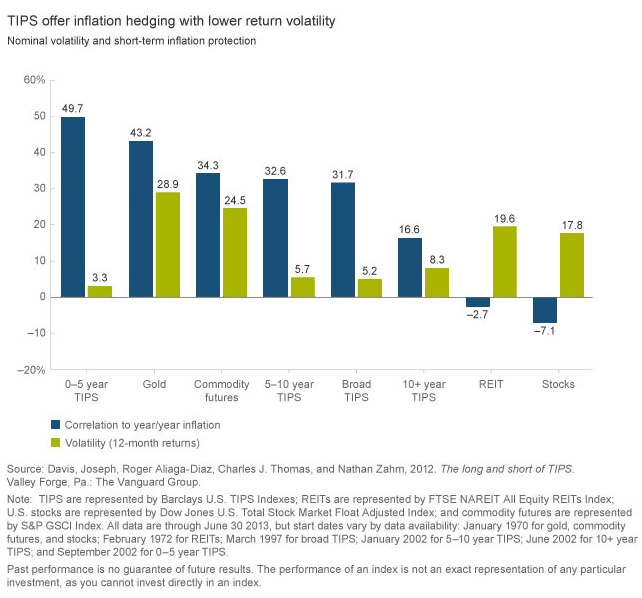

Short-term TIPS have historically had one of the highest correlations to inflation of any asset class (see chart below). At the same time, the volatility of their returns has been a fraction of the volatility shown by other potential inflation hedges, such as commodities, gold, and real estate. Low price volatility, resulting from short-term TIPS’ lower interest rate sensitivity, allows inflation-indexed income payments to drive a larger proportion of the investment’s total return. In addition, short-term TIPS prices respond more quickly to short-term fluctuations in the CPI—including changes in food and energy prices.

{kind=link}

Why is Vanguard’s short-term TIPS fund index and the broad TIPS fund active?

Vanguard introduced Vanguard Short-Term Inflation-Protected Securities Index Fund once the number of short-term issues reached a critical mass in depth and liquidity, making it suitable as an indexing segment. TIPS with maturities of 0–5 years now represent about 35% of the total TIPS market.

As noted above, the short-term fund is very sensitive to CPI changes and is less volatile than longer-maturity TIPS. “As a manager, this means the short-term fund presents fewer opportunities for active management, whereas the longer-maturity issues provide opportunities for significant added value over time by looking for price discrepancies tied to the BEI rate, to the slope of the yield curve, and to the relative value of different maturities,” Wright-Casparius said.

Will TIPS get hammered if rates continue rising? What if inflation rises at the same time?

“That can be a good time to own TIPS—it’s counterintuitive,” Wright-Casparius said. “TIPS’ prices will fall in the near term if rates rise, but think about what’s happening: You tend to have above-trend economic growth when rates rise, accompanied by a rise in inflationary pressures. If the level of inflation is unexpected, TIPS will compensate you well, helping to offset negative principal return.”

As with nominal bonds, low yields mean little cushion to offset dropping prices, increasing the size of a negative return. Over time, however, a TIPS fund or ETF will offset a price drop through the inflation adjustment to principal and the reinvestment of principal at higher rates.

The chart below shows how the TIPS market responded in five years that had rising rates. In 1999, 2005, and 2006, the Fed tightened monetary policy. Rising real rates resulted in negative inflation-adjusted returns for those years. “Keep in mind that the duration on the broad TIPS market is in the 8- to 9-year range, and so TIPS are not immune from the effect of rising rates,” Wright-Casparius said. That said, TIPS outperformed nominal Treasuries in each of those years.

“TIPS carried a much higher yield than nominals during those periods, so the return from income was larger, helping to offset the negative principal returns,” Wright-Casparius said. Jumping forward to the low-yield environment of 2013, TIPS did not have that income cushion to offset negative principal returns, resulting in a negative return year-to-date in absolute terms, while also underperforming nominal Treasuries.

In the other rising-rate environment, 2008, TIPS underperformed nominal Treasuries as investors sought the most liquid bonds in the market.

ow does a TIPS mutual fund or ETF work?

The U.S. Treasury adjusts TIPS’ principal periodically to reflect reported changes in the CPI. Fluctuations in prices of food and energy have historically accounted for 85%–90% of the volatility in the monthly CPI inflation rate.

Total return on a TIPS fund is a function of actual trailing inflation and the bond market’s expectation regarding future inflation. A TIPS portfolio adjusts an investor’s principal investment by the actual trailing inflation rate. Changes in inflation expectations can produce subpar or negative total returns even when actual inflation is positive.

The yield on a fund is affected by many risk factors. The most significant would be changes in the BEI rate associated with either a change in forward-inflation expectations or a change in the inflation-risk premium required by investors in nominal bonds. TIPS’ returns may also be affected by changes in the shape of the yield curve, liquidity risk, new-issue supply, or the rate of inflation built into a bond.

“There are many drivers of TIPS’ returns. There are a lot of moving parts,” said Wright-Casparius. “The main thing is to remember is that TIPS’ duration is calculated without the inflation compensation component because we don’t know what future realized inflation will be for TIPS. As a result, TIPS are more volatile than nominal Treasuries, which have an assumed inflation rate embedded in duration calculations.

“You also have to pay attention to the level of inflation compensation when rates are very, very low. You are already paying a premium for that inflation protection. If you buy when the break-even is at 2.6 percent, you may be buying at the rich end of the spectrum versus when the break-even is at 2 percent.”